Paul Sweeney and Danny McCoy (IBEC) present different views on rebuilding the economy in today's Irish Times, which is also the theme of today's editorial.

Danny McCoy laments the lack of evidence-based policy-making. Whereas Paul Sweeney presents a critique of those, like Donal Donovan, who suggest the current economic strategy is in any sense working.

Friday, 31 December 2010

Saturday, 25 December 2010

The scenic route to public ownership

Slí Eile: 2010 - private banking emerges from the dark world. A slow crash. Now that €3bn+ has been raided from the National Pension Reserve Fund to invest in the 'people's bank' perhaps Government are about to take TASC advice and invest in jobs and people? Here is hoping that 2011 brings fundamental changes in social and economic policy. A peaceful and restful Christmas to all our readers and bloggers!

Thursday, 23 December 2010

How good is our export performance?

Rory O'Farrell: The government's policy (its probably overly generous to call it a policy, more the rationale give for their various mistakes) is to increase employment through exports. The government is going all out to promote the idea that exports are booming, (for example, look here).

Unfortunately, the truth is different.

The latest data from the CSO (available here) shows an improvement in our trade surplus. This is necessary to repay all the debt the country has borrowed (public and private). I previously explained the importance of the current account here. However the latest figures show the improvement is purely due to a drop in imports. This isn't necessarily a bad thing. For example substituting Belgian Leonidas chocolates with much tastier Gallweys' chocolates from Waterford will reduce imports and increase employment. What is a bad thing however is that (seasonally adjusted) exports have dropped 2% in October. Exports peaked in July, and have not recovered.

Exports in other countries decreased by more than ours during the recession, so the 'resilience' of our exports is an achievement. Also, there was a bounce as exports recovered from their decrease following the financial crisis. However, if we are really gaining competitiveness one would expect exports to grow along with the economies of our trading partners. Also (seasonally adjusted) exports were actually higher in March 2007, despite prices being far higher then.

The folly of cutting infrastructure spending is shown by the stagnation of our exports. Even if wages are cut, firms will not be attracted to one of the wettest countries in Europe where they turn off the water supply at 7pm. Why pay someone €7.65 to mop the floors when they can't get a bucket of water?

UPDATE: I've come across some new data from Eurostat (available here). It compares the growth in exports between the periods Jan-Sept 2009 and Jan-Sept 2010. Worryingly, with the exception of Luxembourg, Ireland is the worst performer.

Unfortunately, the truth is different.

The latest data from the CSO (available here) shows an improvement in our trade surplus. This is necessary to repay all the debt the country has borrowed (public and private). I previously explained the importance of the current account here. However the latest figures show the improvement is purely due to a drop in imports. This isn't necessarily a bad thing. For example substituting Belgian Leonidas chocolates with much tastier Gallweys' chocolates from Waterford will reduce imports and increase employment. What is a bad thing however is that (seasonally adjusted) exports have dropped 2% in October. Exports peaked in July, and have not recovered.

Exports in other countries decreased by more than ours during the recession, so the 'resilience' of our exports is an achievement. Also, there was a bounce as exports recovered from their decrease following the financial crisis. However, if we are really gaining competitiveness one would expect exports to grow along with the economies of our trading partners. Also (seasonally adjusted) exports were actually higher in March 2007, despite prices being far higher then.

The folly of cutting infrastructure spending is shown by the stagnation of our exports. Even if wages are cut, firms will not be attracted to one of the wettest countries in Europe where they turn off the water supply at 7pm. Why pay someone €7.65 to mop the floors when they can't get a bucket of water?

UPDATE: I've come across some new data from Eurostat (available here). It compares the growth in exports between the periods Jan-Sept 2009 and Jan-Sept 2010. Worryingly, with the exception of Luxembourg, Ireland is the worst performer.

Tuesday, 21 December 2010

Are Irish Managers up to the task?

The Irish Times carries an interesting report on the mediocre performance of Irish management. This is consistent with previous reports (available here). This also raises important questions about the increase in inequality during the boom and the increase in management pay over that of workers.

In general management in MNEs operating in Ireland is better than SMEs, and the countries with the best managers are the US, Germany, and Sweden. Given that our labour market has much more in common with Germany and Sweden than the US, Irish managers should look to these countries. Rather than seeking confrontation with unions, working with them is usually a more successful approach. The Luas is an excellent example of cooperation.

There are better ways to improve competitiveness than cutting wages. However, are Irish managers up to the task?

Monday, 20 December 2010

It's just not fair (a Ben Hur tale)

Homo economicus: It's just not fair. We have been at sea for two years and have faced almighty storms and attacks from raiding speculator vessels. We have spread the pain on board by flogging the slaves who do the rowing. Just as the other ships draw close we flog them harder and harder indicating that the beats of the hammer will be front loaded in velocity up to the limits of debt slave endurance (on board we like to say that things are manageable). All the time we enchant pari passu pari passu - we are all in this together depositors and bondholders. We would never harm a bondholder in a 1,000 years unless our overlords told us to. And what do our overlords in the markets say? We don't trust you and we don't think that you can bring the ship in.

It's just rotten - having rowed, flogged and done everything to appease the market overlords they treat us with contempt never dropping below 8 beats per minute as shown by these bond spreads. The curve rises every time we inflict more austerity flogging. Data here. What more do you want us to do? We can cut wages even more and stop buying your exports to us? We can export our most talented and best educated? We can offer you smart golf courses in place of ghost estates?

I'll tell you what we will do - we will send more ships and more debt slaves to shock the market further. Instead of a €15bn adjustment, lets go for €30bn. Shock them I say. And we can:

Fire 30,000 public servants

Cut public sector wages to align with those in Singapore

Simply abolish the minimum wage

Contract out hospitals and provide private health insurance to everyone

Raise class size to 40

Sell of the state silver - especially the profitable bits

Reduce welfare to the levels prevailing in the wastelands of inner city Britain - that will incentivise them.

Bet you that is what you are thinking right now o godly markets. And we will never default, never default, pari passu, we will do whatever you order.

(Slí Eile)

It's just rotten - having rowed, flogged and done everything to appease the market overlords they treat us with contempt never dropping below 8 beats per minute as shown by these bond spreads. The curve rises every time we inflict more austerity flogging. Data here. What more do you want us to do? We can cut wages even more and stop buying your exports to us? We can export our most talented and best educated? We can offer you smart golf courses in place of ghost estates?

I'll tell you what we will do - we will send more ships and more debt slaves to shock the market further. Instead of a €15bn adjustment, lets go for €30bn. Shock them I say. And we can:

Fire 30,000 public servants

Cut public sector wages to align with those in Singapore

Simply abolish the minimum wage

Contract out hospitals and provide private health insurance to everyone

Raise class size to 40

Sell of the state silver - especially the profitable bits

Reduce welfare to the levels prevailing in the wastelands of inner city Britain - that will incentivise them.

Bet you that is what you are thinking right now o godly markets. And we will never default, never default, pari passu, we will do whatever you order.

(Slí Eile)

Moneylending

Nat O'Connor: The Irish Times reports on the €113 million owed to legal moneylenders, who can charge over 180 per cent interest.

This is not a new issue. It was highlighted by Caroline Corr and Dr Pauline Conroy in TASC's publication, Life and Debt: Financial Exclusion in the Age of NAMA, which is an update of earlier work on this issue by the same authors.

For example, "In 2005, 23 per cent of households – or nearly a quarter – had no bank account. Many of these households – a large number of which are headed by women – are therefore forced to access financial products at prices they cannot afford. Such ‘services’ range from high-cost credit to expensive chequecashing facilities."

While a lot of attention has been focused on the ECB's concern about emergency banking legislation, the Government could do much worse that use draconian powers to require banks to provide, as a right, a basic bank account for everyone in this country. This would not necessarily include any overdraft facilities, but simply be an account free of stamp duty and transaction costs, incorporating a cash card (ATM card), with flexible account opening requirements, and no minimum opening or monthly balance.

However, instead of being helped to stablise their finances, it is highly likely that many of the people paying debts to moneylenders are badly affected by the cuts in social welfare and the minimum wage; which will drive ever more people into a cycle of poverty and further debt this Christmas.

This is not a new issue. It was highlighted by Caroline Corr and Dr Pauline Conroy in TASC's publication, Life and Debt: Financial Exclusion in the Age of NAMA, which is an update of earlier work on this issue by the same authors.

For example, "In 2005, 23 per cent of households – or nearly a quarter – had no bank account. Many of these households – a large number of which are headed by women – are therefore forced to access financial products at prices they cannot afford. Such ‘services’ range from high-cost credit to expensive chequecashing facilities."

While a lot of attention has been focused on the ECB's concern about emergency banking legislation, the Government could do much worse that use draconian powers to require banks to provide, as a right, a basic bank account for everyone in this country. This would not necessarily include any overdraft facilities, but simply be an account free of stamp duty and transaction costs, incorporating a cash card (ATM card), with flexible account opening requirements, and no minimum opening or monthly balance.

However, instead of being helped to stablise their finances, it is highly likely that many of the people paying debts to moneylenders are badly affected by the cuts in social welfare and the minimum wage; which will drive ever more people into a cycle of poverty and further debt this Christmas.

Sunday, 19 December 2010

Over the top lads: Why Intelligent People are Getting it Wrong

Rory O'Farrell: During a walk through Passchendaele in Flanders one is confronted by monuments to the stupidity of man.

During the First World War defence was the most successful strategy. However the commanders at the time were schooled in an earlier age, before defence had been mechanised. Their training and prior experience led them to believe that attack was the only way to win a war. By 1939 and 1940 much had changed. The French generals during the start of the Second World War had gained their experiences and training in the trenches. They did not realise that attack had been mechanised, and invested millions of Francs in the Maginot Line. Those in charge look to their past experiences for solutions to current problems, and can persist in viewing current problems through expired modes of thinking.

Fortunately we are not at war, and our troubles are minor in comparison. However the psychology of those commanding our economic policies is perhaps not so different to those of past generals.

During the Great Depression most economists had been schooled in the belief that economic problems are problems of supply. Politicians persisted with using flawed policies for several years. During this time Keynes showed that the problem of the Great Depression was one of demand. In the post-war years economists came to believe almost all economic problems were ones of demand, as these were all the problems that had experience of. However, when the oil crisis hit, and the supply of oil was reduced, demand side policies could not end stagflation. Economists and policymakers at the time lacked the mental tools to deal with stagflation. Now most economists active today have been trained during a period when supply side policies have held supremacy. However, the current economic problem, in Ireland and the rest of the world, is a demand problem caused by the financial crisis.

When all one’s experiences have been of a certain problem, it is hard to conceive of current problems as different to those in the past. During the First World War, when throwing 50,000 soldiers at the German machine guns did not work, the generals threw 100,000 soldiers at the problem. Alternative solutions could not be conceived. The strategy failed because the strategy was wrong, regardless of how obvious it may appear now.

The EU and Irish government use economic models to provide ‘insights’ into solving our problems. However the models being use ignore the core causes of the crisis, namely the lack of demand due to a poor distribution of income. Even where the IMF correctly identifies problems, such as substandard infrastructure, they can not bring themselves to offer demand side solutions (like stimulating demand by investing in infrastructure). When their policies fail (such as current Irish bond prices remaining prohibitively high) they offer nothing other than the same policies applied more intensely. They are using models for a different crisis to the one we face.

Despite 11 failed attacks on the Isonzo in northern Italy during the First World War, in which hundreds of thousands died, the Italian elite continued with their failed policies, ignoring alternative solutions. Mark Thompson, in his superb narrative of the Italian Front describes their mode of thinking as follows:

During the First World War defence was the most successful strategy. However the commanders at the time were schooled in an earlier age, before defence had been mechanised. Their training and prior experience led them to believe that attack was the only way to win a war. By 1939 and 1940 much had changed. The French generals during the start of the Second World War had gained their experiences and training in the trenches. They did not realise that attack had been mechanised, and invested millions of Francs in the Maginot Line. Those in charge look to their past experiences for solutions to current problems, and can persist in viewing current problems through expired modes of thinking.

Fortunately we are not at war, and our troubles are minor in comparison. However the psychology of those commanding our economic policies is perhaps not so different to those of past generals.

During the Great Depression most economists had been schooled in the belief that economic problems are problems of supply. Politicians persisted with using flawed policies for several years. During this time Keynes showed that the problem of the Great Depression was one of demand. In the post-war years economists came to believe almost all economic problems were ones of demand, as these were all the problems that had experience of. However, when the oil crisis hit, and the supply of oil was reduced, demand side policies could not end stagflation. Economists and policymakers at the time lacked the mental tools to deal with stagflation. Now most economists active today have been trained during a period when supply side policies have held supremacy. However, the current economic problem, in Ireland and the rest of the world, is a demand problem caused by the financial crisis.

When all one’s experiences have been of a certain problem, it is hard to conceive of current problems as different to those in the past. During the First World War, when throwing 50,000 soldiers at the German machine guns did not work, the generals threw 100,000 soldiers at the problem. Alternative solutions could not be conceived. The strategy failed because the strategy was wrong, regardless of how obvious it may appear now.

The EU and Irish government use economic models to provide ‘insights’ into solving our problems. However the models being use ignore the core causes of the crisis, namely the lack of demand due to a poor distribution of income. Even where the IMF correctly identifies problems, such as substandard infrastructure, they can not bring themselves to offer demand side solutions (like stimulating demand by investing in infrastructure). When their policies fail (such as current Irish bond prices remaining prohibitively high) they offer nothing other than the same policies applied more intensely. They are using models for a different crisis to the one we face.

Despite 11 failed attacks on the Isonzo in northern Italy during the First World War, in which hundreds of thousands died, the Italian elite continued with their failed policies, ignoring alternative solutions. Mark Thompson, in his superb narrative of the Italian Front describes their mode of thinking as follows:

The corollary of paternalism is infantilisation. What bound journalists, ministers and staff officers was a deep conservative assumption that ordinary people – unlike themselves – were incapable of grasping their true interests.Over the past months we have been told that a budget and four year plan must be passed prior to a general election. The thinking of the governing elites has not changed much in 100 years.

Saturday, 18 December 2010

Listening to common sense

Slí Eile: Sometimes we don't like listening to one of our own. Hence, expertise from outside is used to reassure us. Take David McWilliams. The mainstream dismisses him as not for real. He has been banging on about the impossibility of solving our debt crisis and kick-starting the economy. His recipe is straightforward - decouple soverign and bank debt default and start out again. See here. He argues that:

That figure explains why the IMF is here. It is not here to bail us out; it is here to bail them out. The bailout is a bailout for the banks of Germany and France and the Irish taxpayer foots the bill. It is that simple. And where will the EU and IMF money come from? It will be borrowed from the very investment banks that will be bailed out. So they will get interest payments from us, in order that we pay for their mistakes.But, David is not the only one saying this. Take the Economist here. It says:

Even so, that Iceland’s economy has done little worse than Ireland’s is still a triumph. It has been tough with its creditors and disregarded some international norms—and recovered. Ireland has stood by its banks to the benefit of the wider European banking system. Its reward has been “rescue” loans at an interest rate that makes it hard to fix its finances. The next Irish government may look at Iceland and decide to play hardball with Europe.And finally, don't miss a brilliant demolition of the Austerity nonsense here

Friday, 17 December 2010

Four Truths about the Irish situation (and one possible solution)

Nat O'Connor: The Government's four-year recovery plan doesn't address the issue of the banks. Without addressing this issue, the credibility of the whole plan is undermined. Richard Douthwaite presented Four Truths about the loan negotiations with the ECB, IMF, etc. These remain valid concerns.

In a context where orthodox monetary policy is no longer available to individual eurozone member states, Douthwaite presents 'deficit easing' as a novel suggestion.

In brief:

Truth 1. If Ireland has to pay interest on the loans being negotiated at a rate which exceeds the rate at which the economy grows over the next few years, it will make the country's situation worse, not better.

Truth 2. Any grant or loan to Ireland will only buy time for the eurozone to come up with a cure for the whole sick system. Ireland should not be asked to bear more than its proportionate share of the cost of gaining this time which is for the benefit of every euro user.

Truth 3. The ECB bears a large share of the responsibility for the regulatory failure which led to the property bubble.

Truth 4. There is a Plan B. Ireland doesn't have to take anything that is offered. It can leave the euro quickly and easily.

In a separate article, Douthwaite proposes a solution in the form of 'deficit easing' (full paper). His proposal is for money to be distributed directly to member states by the ECB (through a form of quantitative easing) and used to pay down national debts and to reduce borrowing requirements for expenditure.

It is increasingly clear that the Irish crisis is a eurozone crisis. And Ireland is caught in a damning position. Either we 'go it alone' and insist on major restructuring of the bank's debts we've taken on - and do huge damage to the (mostly European) banks that lent to our banks - or else we do huge damage to the people in Ireland by taking on huge private debts in order to save - for now - other banks in the eurozone. This is a lose:lose situation, and we need to find another way.

A road to a solution is equally clear. When we pooled our sovereignty into the euro currency and ECB, we took an 'we're all in this together' approach. We need to return to the basic principle of eurozone solidarity; and indeed wider European solidarity. Ireland should push for a eurozone-wide solution that would also aid Portugal, Greece, Spain - but equally Germany and all the rest. Some form of quantitative easing (or equally 'deficit easing') could be a major part of the solution.

The logic of the deficit easing proposal is interesting, although the politics would perhaps be more difficult to manage - what would stop politicians wanting to use this approach more and more? Nevertheless, orthodox monetary policy is not available, and innovative approaches should be given serious consideration.

In a context where orthodox monetary policy is no longer available to individual eurozone member states, Douthwaite presents 'deficit easing' as a novel suggestion.

In brief:

Truth 1. If Ireland has to pay interest on the loans being negotiated at a rate which exceeds the rate at which the economy grows over the next few years, it will make the country's situation worse, not better.

Truth 2. Any grant or loan to Ireland will only buy time for the eurozone to come up with a cure for the whole sick system. Ireland should not be asked to bear more than its proportionate share of the cost of gaining this time which is for the benefit of every euro user.

Truth 3. The ECB bears a large share of the responsibility for the regulatory failure which led to the property bubble.

Truth 4. There is a Plan B. Ireland doesn't have to take anything that is offered. It can leave the euro quickly and easily.

In a separate article, Douthwaite proposes a solution in the form of 'deficit easing' (full paper). His proposal is for money to be distributed directly to member states by the ECB (through a form of quantitative easing) and used to pay down national debts and to reduce borrowing requirements for expenditure.

It is increasingly clear that the Irish crisis is a eurozone crisis. And Ireland is caught in a damning position. Either we 'go it alone' and insist on major restructuring of the bank's debts we've taken on - and do huge damage to the (mostly European) banks that lent to our banks - or else we do huge damage to the people in Ireland by taking on huge private debts in order to save - for now - other banks in the eurozone. This is a lose:lose situation, and we need to find another way.

A road to a solution is equally clear. When we pooled our sovereignty into the euro currency and ECB, we took an 'we're all in this together' approach. We need to return to the basic principle of eurozone solidarity; and indeed wider European solidarity. Ireland should push for a eurozone-wide solution that would also aid Portugal, Greece, Spain - but equally Germany and all the rest. Some form of quantitative easing (or equally 'deficit easing') could be a major part of the solution.

The logic of the deficit easing proposal is interesting, although the politics would perhaps be more difficult to manage - what would stop politicians wanting to use this approach more and more? Nevertheless, orthodox monetary policy is not available, and innovative approaches should be given serious consideration.

Thursday, 16 December 2010

Guest post by Martin O'Dea: Concrete progress

Martin O'Dea lectures in Management and Human Resource Management at the Dublin Business School

There is an understanding of the errors in our current political and economic strategies among most people now, and also a realisation that things must change fundamentally in the window of opportunity that currently comes from this politicisation and appreciation among the general population; as well as the outrage at the continuous revelations of politico-economic faults. What is required to couple with this outrage and enthusiasm is a whole sea of ideas. All one can do is spend as much time as possible contemplating and presenting one's own contribution, and awaiting the response of others as to the degree to which they are helpful before recharging the batteries and going again. This is the central tenet of a ‘smart society’ and it is with this in mind that the suggestions below are offered.

1. Tell banks that they will reduce personal mortgages for all citizens to an upper value of €1 million and one property per adult mortgage owner; by 20%

• Reduce the amount the banks owe in terms of government investment repayment preferential shares etc.). Or (reduce from ownership by Irish state and have available to bondholders’ equity credit to the value of this reduction (approx 16 billion).

• This is money already borrowed from the ECB under the guise of NAMA and would then act as an ongoing stimulus to the most indebted sector of the population of on average €240 per month, which would not have the difficulty of instantaneous withdrawal and would stimulate mostly indigenous growth as it would progress as long as mortgages run (It is hard to see that the Irish people have not given enough to the banks at this point)

• The long-term and ‘re-found’ nature of this stimulus should guarantee its spending through the economy

• There should be a significant decrease in the future levels of mortgage defaults which looks set to become a major economic and social issue as things are currently

• Offer a direct government stimulus to those in the rental market while ensuring that the benefits be kept from landlords for adult citizens without mortgages

People really cannot be evicted from their homes because they have lost a job building houses that were erroneously built as a result of complete banking mismanagement created a housing market where these people had to become heavily indebted to have a family stead; while all the while having the unemployment benefit that they contributed to, and now need, reduced to pay for these same banks.

2. Recapitalise the country (give the bondholders who invested in the private banks in Ireland a debt-equity swap. This must be done with our European partners and in the understanding that the European Union cannot continue to follow markets sentiment only but must show strength and cohesion that will lead the markets to reinvest in a Europe they see will thrive. A new Irish government can pursue this course of action with a mandate from the Irish people.

3. Immediately create an incentive to the public sector workers which offers each individual who suggests and documents a money saving measure in their workplace 10% of that saving. From major schemes to purchasing canteen milk at a cheaper rate the employees who highlight these savings will receive their 10% savings from their senior managers who will need to achieve major reductions in costs or lose their positions, ala department heads in NYPD in the 90’s. We know beyond any doubt that there are massive wastages in this system which grew unchecked again with government mismanagement. However, incentivising staff’s ingenuity in this way will triumph where a continued governmental fight with a completely incoherent management structure has failed so often.

4. Form online and physical based 'Innovation Centres' around the country. Innovation centres should form a ‘public’ option for citizens seeking employment – in much the same way as one may attend a public or private school or college. These centres will concentrate on varying levels of information management and data mining. These projects may well be part funded by private enterprises and technology companies who may have first refusal to some of the data generated. A keen understanding of the potential information management here will allow one to see this as akin to a government finding minerals underground and employing members of the public to mine (the reduction of welfare and taking of income tax forming much of the funding and added by governmental stimulus and some private investment)

5. Remove unnecessary middle management and others from the health service and other areas and move them to running elements of these innovation centres.

6. Colleges and Universities and the department of education should work quickly towards providing online education courses made available on mobile phone apps as well as simple internet connections. These courses (with interactive and video based tutorials and assessments) should initially prepare people for re-entry into education (preparatory courses for a variety of professions and skill sets) but future development of this public education should be allowed to develop with the advancement of those receiving the education as the main drive.

7. Set about straight away creating an Irish educational institute that will focus on RESEARCH and will attract genuine international leaders in their fields. Locate this institute in a region of the country that can accommodate its needs but would benefit greatly from a decentralised spatially aware investment. Set up arrangements with leading firms to locate near this ‘green field’ institute site to create a fulcrum of learning and innovation and their implementation

8. Form an open government programme, under the website opengov.ie where all information with the exception of some sensitive defence material (perhaps) will be made accessible to the public. The providers of this service who will be a group of non-affiliated capable individuals will provide a web space that will allow citizens have debates, post queries with representatives at the various levels of governance, and pursue those issues through responses, associated laws or new bills etc. This would include budgetary information at a certain time each year, ideally before the final publishing.

9. Provide localopengov.ie and utilise it as one means of a number to encourage local level participation by citizens

10. Increase foreign aid significantly. Appreciate that principals of fairness will permit a growing economy and that a 1% GDP investment to areas of the world historically disadvantaged where absolute poverty and disease are still suffered

11. Utilise innovation centres who will have network coordinated infrastructural support to invest in health providing technologies, and reap a direct benefit in major reductions in health management costs (including smart house, and mobile, technologies that can monitor individuals health while they are in their homes on an ongoing basis and can feed the relevant information to the primary and secondary level of health care) as well as by exporting same technologies.

There is an understanding of the errors in our current political and economic strategies among most people now, and also a realisation that things must change fundamentally in the window of opportunity that currently comes from this politicisation and appreciation among the general population; as well as the outrage at the continuous revelations of politico-economic faults. What is required to couple with this outrage and enthusiasm is a whole sea of ideas. All one can do is spend as much time as possible contemplating and presenting one's own contribution, and awaiting the response of others as to the degree to which they are helpful before recharging the batteries and going again. This is the central tenet of a ‘smart society’ and it is with this in mind that the suggestions below are offered.

1. Tell banks that they will reduce personal mortgages for all citizens to an upper value of €1 million and one property per adult mortgage owner; by 20%

• Reduce the amount the banks owe in terms of government investment repayment preferential shares etc.). Or (reduce from ownership by Irish state and have available to bondholders’ equity credit to the value of this reduction (approx 16 billion).

• This is money already borrowed from the ECB under the guise of NAMA and would then act as an ongoing stimulus to the most indebted sector of the population of on average €240 per month, which would not have the difficulty of instantaneous withdrawal and would stimulate mostly indigenous growth as it would progress as long as mortgages run (It is hard to see that the Irish people have not given enough to the banks at this point)

• The long-term and ‘re-found’ nature of this stimulus should guarantee its spending through the economy

• There should be a significant decrease in the future levels of mortgage defaults which looks set to become a major economic and social issue as things are currently

• Offer a direct government stimulus to those in the rental market while ensuring that the benefits be kept from landlords for adult citizens without mortgages

People really cannot be evicted from their homes because they have lost a job building houses that were erroneously built as a result of complete banking mismanagement created a housing market where these people had to become heavily indebted to have a family stead; while all the while having the unemployment benefit that they contributed to, and now need, reduced to pay for these same banks.

2. Recapitalise the country (give the bondholders who invested in the private banks in Ireland a debt-equity swap. This must be done with our European partners and in the understanding that the European Union cannot continue to follow markets sentiment only but must show strength and cohesion that will lead the markets to reinvest in a Europe they see will thrive. A new Irish government can pursue this course of action with a mandate from the Irish people.

3. Immediately create an incentive to the public sector workers which offers each individual who suggests and documents a money saving measure in their workplace 10% of that saving. From major schemes to purchasing canteen milk at a cheaper rate the employees who highlight these savings will receive their 10% savings from their senior managers who will need to achieve major reductions in costs or lose their positions, ala department heads in NYPD in the 90’s. We know beyond any doubt that there are massive wastages in this system which grew unchecked again with government mismanagement. However, incentivising staff’s ingenuity in this way will triumph where a continued governmental fight with a completely incoherent management structure has failed so often.

4. Form online and physical based 'Innovation Centres' around the country. Innovation centres should form a ‘public’ option for citizens seeking employment – in much the same way as one may attend a public or private school or college. These centres will concentrate on varying levels of information management and data mining. These projects may well be part funded by private enterprises and technology companies who may have first refusal to some of the data generated. A keen understanding of the potential information management here will allow one to see this as akin to a government finding minerals underground and employing members of the public to mine (the reduction of welfare and taking of income tax forming much of the funding and added by governmental stimulus and some private investment)

5. Remove unnecessary middle management and others from the health service and other areas and move them to running elements of these innovation centres.

6. Colleges and Universities and the department of education should work quickly towards providing online education courses made available on mobile phone apps as well as simple internet connections. These courses (with interactive and video based tutorials and assessments) should initially prepare people for re-entry into education (preparatory courses for a variety of professions and skill sets) but future development of this public education should be allowed to develop with the advancement of those receiving the education as the main drive.

7. Set about straight away creating an Irish educational institute that will focus on RESEARCH and will attract genuine international leaders in their fields. Locate this institute in a region of the country that can accommodate its needs but would benefit greatly from a decentralised spatially aware investment. Set up arrangements with leading firms to locate near this ‘green field’ institute site to create a fulcrum of learning and innovation and their implementation

8. Form an open government programme, under the website opengov.ie where all information with the exception of some sensitive defence material (perhaps) will be made accessible to the public. The providers of this service who will be a group of non-affiliated capable individuals will provide a web space that will allow citizens have debates, post queries with representatives at the various levels of governance, and pursue those issues through responses, associated laws or new bills etc. This would include budgetary information at a certain time each year, ideally before the final publishing.

9. Provide localopengov.ie and utilise it as one means of a number to encourage local level participation by citizens

10. Increase foreign aid significantly. Appreciate that principals of fairness will permit a growing economy and that a 1% GDP investment to areas of the world historically disadvantaged where absolute poverty and disease are still suffered

11. Utilise innovation centres who will have network coordinated infrastructural support to invest in health providing technologies, and reap a direct benefit in major reductions in health management costs (including smart house, and mobile, technologies that can monitor individuals health while they are in their homes on an ongoing basis and can feed the relevant information to the primary and secondary level of health care) as well as by exporting same technologies.

Tuesday, 14 December 2010

Slashing the Minimum Wage: Olli made us do it (or: never let facts get in the way)

Tom McDonnell: Over the weekend, a Government TD insisted on RTE's Week in Politics programme that we should ask Olli Rehn why the minimum wage was cut. I leave it to the reader to decide what that implies for our national sovereignty.

Much of the justification given for the cut was that we had the second highest minimum wage in Europe and that it needed to be cut to provide more employment opportunities. More on this in a second.

The latest annual report of the United Kingdom’s highly respected Low Pay Commission (LPC) is here. The British government uses the recommendations of the Commission when passing legislation related to the minimum wage (including the setting of rates). You will find a wealth of information on issues such as gender composition, sectoral breakdown and other key issues.

Unfortunately, there is no equivalent Commission for Ireland and it is to our great detriment that we do not conduct the same level of research into these areas in Ireland. Irish policymakers seem to have only a passing acquaintance with the strange notions of theory and evidence.

Fortunately for us the LPC report has international data on the rates set for national minimum wages.

I refer you to Appendix 3 of the Low Pay Commission’s report and in particular column 3 (PPs) of Table 3A.1 on page 233. The table has data for eight different EU countries. Ireland has the fifth highest minimum wage rate of the eight EU countries shown. Most importantly, we find that the rate for our nearest neighbour - the UK - was 5.80 (sterling) and the equivalent rate for Ireland, before the 12 per cent cut imposed last week, was 5.43 (sterling) in terms of purchasing power parity. Note as well that only one country in the sample has reacted to the crisis by cutting the minimum wage.

So it seems that those spouting off that we have the second or third highest national minimum wage in Europe either haven’t bothered to check the facts or have decided to ignore the facts.

I’ll leave it to you to decide which is worse.

Much of the justification given for the cut was that we had the second highest minimum wage in Europe and that it needed to be cut to provide more employment opportunities. More on this in a second.

The latest annual report of the United Kingdom’s highly respected Low Pay Commission (LPC) is here. The British government uses the recommendations of the Commission when passing legislation related to the minimum wage (including the setting of rates). You will find a wealth of information on issues such as gender composition, sectoral breakdown and other key issues.

Unfortunately, there is no equivalent Commission for Ireland and it is to our great detriment that we do not conduct the same level of research into these areas in Ireland. Irish policymakers seem to have only a passing acquaintance with the strange notions of theory and evidence.

Fortunately for us the LPC report has international data on the rates set for national minimum wages.

I refer you to Appendix 3 of the Low Pay Commission’s report and in particular column 3 (PPs) of Table 3A.1 on page 233. The table has data for eight different EU countries. Ireland has the fifth highest minimum wage rate of the eight EU countries shown. Most importantly, we find that the rate for our nearest neighbour - the UK - was 5.80 (sterling) and the equivalent rate for Ireland, before the 12 per cent cut imposed last week, was 5.43 (sterling) in terms of purchasing power parity. Note as well that only one country in the sample has reacted to the crisis by cutting the minimum wage.

So it seems that those spouting off that we have the second or third highest national minimum wage in Europe either haven’t bothered to check the facts or have decided to ignore the facts.

I’ll leave it to you to decide which is worse.

Monday, 13 December 2010

Only growth can reduce the debt

Michael Burke: Over on Irish Ecoomy, Karl Whelan has initiated a useful discussion highlighting some of the differences between EU Commission and government forecasts. Very usefully, he has created an open spreadsheet which fleshes out the bones of the forecasts, which allows some of the underlying assumptions to be derived.

Only time will tell whether the EU Commission’s forecasts are more accurate. But they do at least have the merit of internal consistency, whereas DoF forecasts have none.

In relation to underlying (non-bank) deficit, the EU forecast a deficit of €16.4bn in 2011. Assuming an underlying deficit of €18.9bn in the current year, this implies that a €6bn ‘fiscal adjustment’ leads to actual deficit-reduction of €2.5bn. Likewise another package of cuts in 2012 amounting to €3.6bn leads to actual deficit-reduction of €1.5bn. In both cases the ratio is the same 1:2.4, €1bn in savings requires €2.4b in cuts/tax increases.

Contrast this with the DoF 1:1.6 in 2011, and an unfeasibly high 1:1.24 in 2012, that is cuts of €3.6bn could lead to a lower deficit of €2.9bn.

The facts are that cuts and tax increases in 2008/10 of €14.6bn led to a wider, not narrower deficit. So in both instances the Commission and the DoF are assuming a much less negative effect on government finances than has actually been the case.

But at least the Commission’s forecasts are at least within the spectrum of reasonable discussion and have the merit of consistency. Neither could be said for the DoF forecasts.

The (23yr old, single) laid off public sector worker previously on €35,000 pa was paying €6,500 a year in direct taxes and is now receiving €7,500 in JSA. At least another €2,000 is lost in VAT receipts on her lower consumption. So, without any account of the wider impact on the economy from this reduction in her output, or the incomes or consumption of others, or other welfare benefits to which she may be entitled, from just the direct effects alone, the gross saving for the government of €35,000 in spending cuts becomes a net saving of just €19,000. A ratio of 1:1.84.

Turning to the EU forecasts alone, it should be clear where the deficit-reduction is coming from. The forecasts are for nominal GDP to increase by €2bn in 2011 and by €4.3bn in 2012. At the same time, the deficit is expected to fall €2.5bn and €1.5bn in those years.

If the assumption is that the growth contribution to changes in government finances were simply the government’s share of total revenues (approx 35%), then growth would be responsible for €700mn of the deficit-reduction in 2011 and €1.5bn in 2012 (the entirety of the deficit-reduction in 2012).

However, this assumption reproduces a commonplace error. The sensitivity of the government finances to changes in GDP is a combination of the marginal tax take (not the average tax rate) plus the sensitivity of government outlays to changes in output (primarily changes in welfare payments). The DoF estimates these together total 0.6 (which seems to be an underestimate in current circumstances).

Using the DoF sensitivity estimate of 0.6, in 2011 growth would be responsible for €1.2bn or nearly half the total forecast deficit reduction, while in 2012 it would account for nearly €2.6bn in deficit-reduction, much greater than the anticipated level of €1.5bn. The measures themselves off-set this growth effect and are counter-productive.

If there is to be any deficit-reduction at all it can only come from growth. The EU forecasts demonstrate that deficit reduction over anything but the very short-term is entirely a function of growth. ‘Austerity’ measures run counter to promoting growth and are likely to lead to counter-productive increases in the deficit. Again.

Only time will tell whether the EU Commission’s forecasts are more accurate. But they do at least have the merit of internal consistency, whereas DoF forecasts have none.

In relation to underlying (non-bank) deficit, the EU forecast a deficit of €16.4bn in 2011. Assuming an underlying deficit of €18.9bn in the current year, this implies that a €6bn ‘fiscal adjustment’ leads to actual deficit-reduction of €2.5bn. Likewise another package of cuts in 2012 amounting to €3.6bn leads to actual deficit-reduction of €1.5bn. In both cases the ratio is the same 1:2.4, €1bn in savings requires €2.4b in cuts/tax increases.

Contrast this with the DoF 1:1.6 in 2011, and an unfeasibly high 1:1.24 in 2012, that is cuts of €3.6bn could lead to a lower deficit of €2.9bn.

The facts are that cuts and tax increases in 2008/10 of €14.6bn led to a wider, not narrower deficit. So in both instances the Commission and the DoF are assuming a much less negative effect on government finances than has actually been the case.

But at least the Commission’s forecasts are at least within the spectrum of reasonable discussion and have the merit of consistency. Neither could be said for the DoF forecasts.

The (23yr old, single) laid off public sector worker previously on €35,000 pa was paying €6,500 a year in direct taxes and is now receiving €7,500 in JSA. At least another €2,000 is lost in VAT receipts on her lower consumption. So, without any account of the wider impact on the economy from this reduction in her output, or the incomes or consumption of others, or other welfare benefits to which she may be entitled, from just the direct effects alone, the gross saving for the government of €35,000 in spending cuts becomes a net saving of just €19,000. A ratio of 1:1.84.

Turning to the EU forecasts alone, it should be clear where the deficit-reduction is coming from. The forecasts are for nominal GDP to increase by €2bn in 2011 and by €4.3bn in 2012. At the same time, the deficit is expected to fall €2.5bn and €1.5bn in those years.

If the assumption is that the growth contribution to changes in government finances were simply the government’s share of total revenues (approx 35%), then growth would be responsible for €700mn of the deficit-reduction in 2011 and €1.5bn in 2012 (the entirety of the deficit-reduction in 2012).

However, this assumption reproduces a commonplace error. The sensitivity of the government finances to changes in GDP is a combination of the marginal tax take (not the average tax rate) plus the sensitivity of government outlays to changes in output (primarily changes in welfare payments). The DoF estimates these together total 0.6 (which seems to be an underestimate in current circumstances).

Using the DoF sensitivity estimate of 0.6, in 2011 growth would be responsible for €1.2bn or nearly half the total forecast deficit reduction, while in 2012 it would account for nearly €2.6bn in deficit-reduction, much greater than the anticipated level of €1.5bn. The measures themselves off-set this growth effect and are counter-productive.

If there is to be any deficit-reduction at all it can only come from growth. The EU forecasts demonstrate that deficit reduction over anything but the very short-term is entirely a function of growth. ‘Austerity’ measures run counter to promoting growth and are likely to lead to counter-productive increases in the deficit. Again.

Beware economists bearing models

The following is abridged from a post that appears on Notes on the Front. See also Nat O'Connor's post here.

Michael Taft: So the 2011 budget is reasonably progressive. Indeed, budgets over the last two years have been reasonably progressive. And to prove all this, the ESRI researchers ran the numbers through their Switch tax/benefit model. It tells some useful things.

But does it tell us how the 2011 budget impacted on people’s living standards? No.

A major omission in the ESRI model is that it assumes disposable income is, by implication, equivalent to ‘living standards’. For instance, they claim that the top quintile experienced a -2.7 percent fall in their disposable income, while the bottom quintile experienced a -2.8 percent. Okay, not progressive; just neutral. But is it?

Out of our disposable incomes we must pay for necessities that we may have little cost-control over. For instance, we need housing, food, electricity, gas, telephone, etc. Therefore, our disposable (after-tax) income can be broken into two elements:

• Non-discretionary disposable income – which is spent on necessities which we have little cost-control over.

• Discretionary disposable income – the amount after both tax and necessities.

The CSO’s Household Budget Survey 2005 puts some numbers on this distinction (the following is indicative - a new Survey will be out soon). And I take only three necessities: housing, food and utilities (fuel, light and fixed-line telephone). We find:

• The bottom quintile spends approximately 58 percent on these necessities (or non-discretionary disposable income).

• The top quintile spends approximately 22.2 percent

So what happens when we apply the ESRI’s fall in disposable incomes to ‘discretionary disposable income’ (that is, after payments for necessities are made)?

The bottom quintile experiences a fall of approximately -6.5 percent while the top quintile is only hit for -3.5 percent.

Even this doesn’t fully measure living standards. A household with surplus income will more easily absorb a fall in disposable income than those who have a deficit (i.e. spends more than they take in).

Again, the Household Budget Survey shows that the poorest households experience the worst deficit at -37 percent; the highest income households had a surplus of 26 percent. High income households can easily absorb substantially higher falls in disposable income than the rest of the population without denting their life-styles.

These are other data must be integrated into any model if we are to get a more accurate measurement of budgetary impacts on living standards. In addition, we must take care to integrate ‘real-life’ wage and income increases. For instance, the CSO shows the decline in average weekly earnings over the last six quarters, 18 months:

• Management / Professionals: -1.1 percent

• Clerical / Secretarial: -6.2 percent

• Production workers: -6.6 percent

Add in the estimate increase in non-wage income next year (29 percent according to the ESRI) and we can see that those on high incomes have been able to protect their living standards (and in some cases, even enhance them) to a much greater extent than the vast majority of workers.

It is incumbent upon the ESRI to produce its full findings, rather than just a newspaper article. It cannot expect the public to accept its findings on faith. We have learned the harsh truth about models.

We know, for instance, that the Government’s model was flawed – fatally so. We also know the considerable limitations of the ESRI’s Hermes model, upon which researchers were actually suggesting only a few months ago, that the Irish economy could return to near full-employment by 2015. We know these were badly mistaken.

At the end of the day, the ESRI’s Switch model cannot tell us about impacts on living standards for it doesn’t seek to do so. It only gives us model-driven data to contribute one piece of a very large, more complex puzzle.

The ESRI started its article by asking the question: ‘Was Budget 2011 fair?’ After reading the article, we are no wiser.

Michael Taft: So the 2011 budget is reasonably progressive. Indeed, budgets over the last two years have been reasonably progressive. And to prove all this, the ESRI researchers ran the numbers through their Switch tax/benefit model. It tells some useful things.

But does it tell us how the 2011 budget impacted on people’s living standards? No.

A major omission in the ESRI model is that it assumes disposable income is, by implication, equivalent to ‘living standards’. For instance, they claim that the top quintile experienced a -2.7 percent fall in their disposable income, while the bottom quintile experienced a -2.8 percent. Okay, not progressive; just neutral. But is it?

Out of our disposable incomes we must pay for necessities that we may have little cost-control over. For instance, we need housing, food, electricity, gas, telephone, etc. Therefore, our disposable (after-tax) income can be broken into two elements:

• Non-discretionary disposable income – which is spent on necessities which we have little cost-control over.

• Discretionary disposable income – the amount after both tax and necessities.

The CSO’s Household Budget Survey 2005 puts some numbers on this distinction (the following is indicative - a new Survey will be out soon). And I take only three necessities: housing, food and utilities (fuel, light and fixed-line telephone). We find:

• The bottom quintile spends approximately 58 percent on these necessities (or non-discretionary disposable income).

• The top quintile spends approximately 22.2 percent

So what happens when we apply the ESRI’s fall in disposable incomes to ‘discretionary disposable income’ (that is, after payments for necessities are made)?

The bottom quintile experiences a fall of approximately -6.5 percent while the top quintile is only hit for -3.5 percent.

Even this doesn’t fully measure living standards. A household with surplus income will more easily absorb a fall in disposable income than those who have a deficit (i.e. spends more than they take in).

Again, the Household Budget Survey shows that the poorest households experience the worst deficit at -37 percent; the highest income households had a surplus of 26 percent. High income households can easily absorb substantially higher falls in disposable income than the rest of the population without denting their life-styles.

These are other data must be integrated into any model if we are to get a more accurate measurement of budgetary impacts on living standards. In addition, we must take care to integrate ‘real-life’ wage and income increases. For instance, the CSO shows the decline in average weekly earnings over the last six quarters, 18 months:

• Management / Professionals: -1.1 percent

• Clerical / Secretarial: -6.2 percent

• Production workers: -6.6 percent

Add in the estimate increase in non-wage income next year (29 percent according to the ESRI) and we can see that those on high incomes have been able to protect their living standards (and in some cases, even enhance them) to a much greater extent than the vast majority of workers.

It is incumbent upon the ESRI to produce its full findings, rather than just a newspaper article. It cannot expect the public to accept its findings on faith. We have learned the harsh truth about models.

We know, for instance, that the Government’s model was flawed – fatally so. We also know the considerable limitations of the ESRI’s Hermes model, upon which researchers were actually suggesting only a few months ago, that the Irish economy could return to near full-employment by 2015. We know these were badly mistaken.

At the end of the day, the ESRI’s Switch model cannot tell us about impacts on living standards for it doesn’t seek to do so. It only gives us model-driven data to contribute one piece of a very large, more complex puzzle.

The ESRI started its article by asking the question: ‘Was Budget 2011 fair?’ After reading the article, we are no wiser.

Guest post by Gerard Doyle and Tanya Lalor: Getting more bang for your buck

In this guest post, Gerard Doyle and Tanya Lalor of TSA Consultancy make the case for social enterprise to be part of any future stimulus programme.

For the past two years, economists and commentators have drawn attention to the urgency for a stimulus to re-invigorate the ailing Irish economy. With the exception of a small number of economists, this line of argument usually assumes that the private sector will be the only source of employment creation and should therefore be the focus of State resources.

Is this really the most effective use of limited resources?

We would argue that there are 65,000 reasons for including social enterprise in any future stimulus package - the Social Enterprise Task Force (The Social Enterprise Task Force (2010) ‘Adding Value Delivering Change – The Role of Social Enterprise in National Recovery’ Dublin) forecasts that 65,000 jobs could be created if the Government invested in a social enterprise strategy.

Social enterprises have a unique contribution to make because of a their differences to the private sector - the latter’s principle concern is with creating a return on investment for its shareholders, while social enterprise, in contrast, is motivated by a combination of social and economic objectives.

Social enterprises aim to enable communities to provide services that respond to community need; they are a mechanism for communities to have a greater level of control of their economic development; they provide employment and training opportunities for people out of work for a long time. These aims of social enterprises mean that they can serve as a catalyst for the economic regeneration of disadvantaged communities.

Because social enterprises are democratically controlled businesses, they do not wreak havoc on society - unlike the recent behaviour of our banks and many developers who have made woeful business decisions driven by greed. Indeed, social enterprises can play in important role in providing an example to private businesses that they have social as well as environmental responsibilities to society.

There are a number of sectors with particular employment potential for social enterprises.

For example, Ireland exports the bulk of its waste to Asia and mainland Europe for recycling and then purchases the recycled material back - this is crazy economics. If there was a change of mindset and waste was viewed as an asset, thousands of jobs could be generated. Waste could be handled by social enterprises already in existence, such as Sunflower recycling, which also provides training and a career path for long-term unemployed living in Dublin’s North Inner City.

Another sector is renewable energy. Ireland has some 6% of EU wind resources, and we are one of the richest countries in the world in terms of wind energy potential per capita. The renewable energy sector has the potential to generate thousands of jobs. One only has to look at Denmark to see the potential role social enterprise could play in providing employment an income for rural communities. Over 60% of Danish wind energy is generated by wind guilds - which are similar structures to cooperatives. There is no reason why this could not happen in Ireland - if social enterprises were to receive a contribution towards capital costs and increased prices for electricity supplied to the grid. Also, with a large dairy and beef industry, social enterprises could be formed in rural areas to generate energy from anaerobic digestion.

In urban communities, botched attempts at regeneration via public/private partnerships have left thousands of households living in substandard accommodation. Rather than repeating the same mistake by engaging in property developers, local authorities should support community organisations to become partners in the economic transformation of inner city areas. This is not a unique or alien concept - there are numerous examples of this approach being successful in the UK as well as North America - hardly bastions of alternative economics.

There has been a paralysis amongst policy makers when it comes to social enterprises - at a time when we appear to be bereft of ideas about where jobs may be created and sustained, surely the time has finally come for the potential of this sector to be acknowledged.

For the past two years, economists and commentators have drawn attention to the urgency for a stimulus to re-invigorate the ailing Irish economy. With the exception of a small number of economists, this line of argument usually assumes that the private sector will be the only source of employment creation and should therefore be the focus of State resources.

Is this really the most effective use of limited resources?

We would argue that there are 65,000 reasons for including social enterprise in any future stimulus package - the Social Enterprise Task Force (The Social Enterprise Task Force (2010) ‘Adding Value Delivering Change – The Role of Social Enterprise in National Recovery’ Dublin) forecasts that 65,000 jobs could be created if the Government invested in a social enterprise strategy.

Social enterprises have a unique contribution to make because of a their differences to the private sector - the latter’s principle concern is with creating a return on investment for its shareholders, while social enterprise, in contrast, is motivated by a combination of social and economic objectives.

Social enterprises aim to enable communities to provide services that respond to community need; they are a mechanism for communities to have a greater level of control of their economic development; they provide employment and training opportunities for people out of work for a long time. These aims of social enterprises mean that they can serve as a catalyst for the economic regeneration of disadvantaged communities.

Because social enterprises are democratically controlled businesses, they do not wreak havoc on society - unlike the recent behaviour of our banks and many developers who have made woeful business decisions driven by greed. Indeed, social enterprises can play in important role in providing an example to private businesses that they have social as well as environmental responsibilities to society.

There are a number of sectors with particular employment potential for social enterprises.

For example, Ireland exports the bulk of its waste to Asia and mainland Europe for recycling and then purchases the recycled material back - this is crazy economics. If there was a change of mindset and waste was viewed as an asset, thousands of jobs could be generated. Waste could be handled by social enterprises already in existence, such as Sunflower recycling, which also provides training and a career path for long-term unemployed living in Dublin’s North Inner City.

Another sector is renewable energy. Ireland has some 6% of EU wind resources, and we are one of the richest countries in the world in terms of wind energy potential per capita. The renewable energy sector has the potential to generate thousands of jobs. One only has to look at Denmark to see the potential role social enterprise could play in providing employment an income for rural communities. Over 60% of Danish wind energy is generated by wind guilds - which are similar structures to cooperatives. There is no reason why this could not happen in Ireland - if social enterprises were to receive a contribution towards capital costs and increased prices for electricity supplied to the grid. Also, with a large dairy and beef industry, social enterprises could be formed in rural areas to generate energy from anaerobic digestion.

In urban communities, botched attempts at regeneration via public/private partnerships have left thousands of households living in substandard accommodation. Rather than repeating the same mistake by engaging in property developers, local authorities should support community organisations to become partners in the economic transformation of inner city areas. This is not a unique or alien concept - there are numerous examples of this approach being successful in the UK as well as North America - hardly bastions of alternative economics.

There has been a paralysis amongst policy makers when it comes to social enterprises - at a time when we appear to be bereft of ideas about where jobs may be created and sustained, surely the time has finally come for the potential of this sector to be acknowledged.

Friday, 10 December 2010

Progressive Austerity?

Nat O'Connor: There has been a flurry of calculations about the effect of Budget 2011. One technical, but important, point is that our income tax system (inclusive of PRSI and USC) is now less progressive than it was last year.

Nearly everyone pays more tax due to Budget 2011 (except for the self-employed earning over €200,000) but the extent to which 'those who have more will pay more' is lessened.

Some ESRI economists argue that the cumulative effect of now four austerity budgets since the crisis began has hit higher earners more.

Their chart, invisible on the online version, looks like this:

Q1, Q2, etc stands for the income quintiles. The chart shows that those in the lowest quintile are hit most in 2011, but the authors' argument is that higher quintiles have been hit more when all four budgets' effects are combined.

There is an important caveat in the Irish Times article: "Our analysis does not include the wage or employment effects of the reduction in the minimum national minimum wage." This obviously matters a lot to people in the lowest quintile, and potentially to some in the second quintile, whose earnings are linked with the minimum wage.

This example highlights that any model or calculation of the budgetary effects rests on a number of assumptions. The Irish Times article only skims the surface of the technical details of their analysis, but one question which I raise below is the extent to which they assume tax reliefs that already erode the progressivity of the income tax system. They state that they include changes to pension tax relief, among other variables, which is open to challenge.

Similarly, the official Budget documentation provides 12 example household types and how they are affected by tax changes (in Annex A). However, these examples are neither complete nor balanced.

For example, there are no examples of married couples with two earners, and the tables stop at earnings over €175,000; thus failing to illustrate that self-employed people on over €200,000 are in fact better off after tax and social insurance changes in Budget 2011. Also, an unrealistic assumption is made that a six per cent pension contribution is made by workers, regardless of their income. Firstly, the evidence shows that less than half of Irish workers have a private pension. Secondly, it is unrealistic to assume that workers on low gross incomes can afford to save anything, in the context of the current cost of living. Therefore, the examples and the changes in net income they illustrate must be regarded as inaccurate and misleading, which is a serious concern when it occurs in the official Budget documentation.

One way to get to the bottom of this, is to identify the 'baseline' tax system; that is, the bare bones of the tax system.

In the case of income tax, I argue that the baseline system is composed of three elements: the rates (20% and 41%), the bands (e.g. single people pay 41% from €32,800 upwards) and the basic credits (e.g. single person 1,650). I also add in the basic PRSI, USC, etc rates.

Everything else is an addition or modification of the baseline tax system, including the PAYE tax credit, pension tax relief, etc. A problem with the ESRI-SWITCH and Budget calculations of income change from the budget is that a number of tax reliefs have been 'absorbed' into the baseline tax system. In fairness, the SILC data used in the SWITCH model may have an empirical basis for who uses what tax reliefs, but making these assumptions can easily include normative judgements about what's 'normal' tax relief versus what is in effect a 'bonus'.

I argue that tax reliefs (beyond the basic single person or married credits) are a bonus. Someone using reliefs is paying less than the full amount of tax they should otherwise be paying, based on their income level. This, in turn, lessens the progressivity of the tax system. As such, the loss of a tax relief bonus is not the same thing as an actual increase in someone’s tax liability, such as occurred with the rate and band changes in Budget 2011.

Progressivity in the baseline tax system can be simply measured as to whether someone on a higher income pays not just more tax, but a proportionately higher part of their income. And, as the figure below illustrates, this is indeed the case (blue triangles for 2011, red squares for 2010).

Of course, what the curves illustrate is only the baseline, theoretical progressivity of the tax system. When people use tax reliefs, additional credits, etc. the level of effective tax they pay is reduced and progressivity in the tax system is likewise reduced. And we use a great deal of tax relief in Ireland.

What the figure also illustrates is that, with Budget 2011, the curve is slightly flatter in 2011 than in the previous year. That is, the overall effect of income tax (including USC and PRSI) is less progressive. Everyone pays more tax, and a higher proportion of their incomes, but those on higher incomes see their proportion rise by less than those on lower incomes. For example, someone on €40,000 pays 3.6 per cent more in tax/charges, whereas someone on €200,000 only pays an extra 2.2 per cent.

And at a certain point in time, percentage increases and decreases are not useful comparators. For example, a ten per cent income cut for someone on €200,000 is €20,000; whereas ten per cent for someone on €20,000 is €2,000. Yet, the person on the lower income might suffer more hardship than the person who remains on a very high income of €180,000. Hence, we need to move beyond comparing the percentage changes for different income groups and start asking how much money do people need to live a decent life.

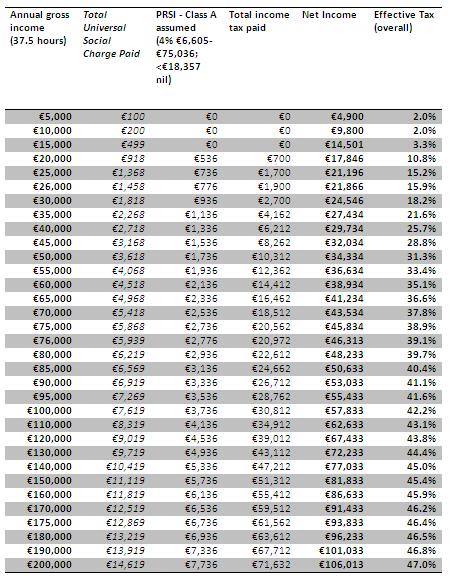

The data used in my line chart is as follows. The 2010 position (single PAYE workers, with no children, paying the income levy, health levy, PRSI and income tax):

The 2011 position (single PAYE workers, with no children, paying the Universal Social Charge, PRSI and income tax):

A further point is that many of the real, material effects of Budget 2011 do not manifest as changes to income. Economic equality can be measured as the combined effect of wealth, income, costs and public services on a person’s total net ‘benefit’ from the economy. Budget 2011 affects all four dimensions of economic equality, but some of the Budget’s implications are not immediately obvious. For example, while the Budget makes immediate changes to tax and social welfare, changing people’s incomes, it also sets the available resources for different Government Departments. It will only be as 2011 progresses that people will see the erosion of local services, such as libraries, roads, public transport, as well as a reduction in the resources available to community groups, etc. These cuts to public spending will impinge upon economic equality, with those on the lowest incomes again most badly affected, because they are more reliant on public services.

There is a lack of distributional analysis in the Budget documentation, which is a major flaw. More sophisticated analysis is required to guage the full extent to which budgetary changes affect different people in society.

Nearly everyone pays more tax due to Budget 2011 (except for the self-employed earning over €200,000) but the extent to which 'those who have more will pay more' is lessened.

Some ESRI economists argue that the cumulative effect of now four austerity budgets since the crisis began has hit higher earners more.

Their chart, invisible on the online version, looks like this:

Q1, Q2, etc stands for the income quintiles. The chart shows that those in the lowest quintile are hit most in 2011, but the authors' argument is that higher quintiles have been hit more when all four budgets' effects are combined.

There is an important caveat in the Irish Times article: "Our analysis does not include the wage or employment effects of the reduction in the minimum national minimum wage." This obviously matters a lot to people in the lowest quintile, and potentially to some in the second quintile, whose earnings are linked with the minimum wage.

This example highlights that any model or calculation of the budgetary effects rests on a number of assumptions. The Irish Times article only skims the surface of the technical details of their analysis, but one question which I raise below is the extent to which they assume tax reliefs that already erode the progressivity of the income tax system. They state that they include changes to pension tax relief, among other variables, which is open to challenge.

Similarly, the official Budget documentation provides 12 example household types and how they are affected by tax changes (in Annex A). However, these examples are neither complete nor balanced.

For example, there are no examples of married couples with two earners, and the tables stop at earnings over €175,000; thus failing to illustrate that self-employed people on over €200,000 are in fact better off after tax and social insurance changes in Budget 2011. Also, an unrealistic assumption is made that a six per cent pension contribution is made by workers, regardless of their income. Firstly, the evidence shows that less than half of Irish workers have a private pension. Secondly, it is unrealistic to assume that workers on low gross incomes can afford to save anything, in the context of the current cost of living. Therefore, the examples and the changes in net income they illustrate must be regarded as inaccurate and misleading, which is a serious concern when it occurs in the official Budget documentation.

One way to get to the bottom of this, is to identify the 'baseline' tax system; that is, the bare bones of the tax system.

In the case of income tax, I argue that the baseline system is composed of three elements: the rates (20% and 41%), the bands (e.g. single people pay 41% from €32,800 upwards) and the basic credits (e.g. single person 1,650). I also add in the basic PRSI, USC, etc rates.

Everything else is an addition or modification of the baseline tax system, including the PAYE tax credit, pension tax relief, etc. A problem with the ESRI-SWITCH and Budget calculations of income change from the budget is that a number of tax reliefs have been 'absorbed' into the baseline tax system. In fairness, the SILC data used in the SWITCH model may have an empirical basis for who uses what tax reliefs, but making these assumptions can easily include normative judgements about what's 'normal' tax relief versus what is in effect a 'bonus'.