Tom McDonnell: There has been much commentary in the last week about the Government’s decision to roll back on its commitment to end the Section 23 property tax breaks. The Government has instead committed to an economic analysis of the impact of ending the tax breaks. Although TASC called for the abolition of these reliefs in its pre- Budget submission, economic analysis of budgetary measures is in many ways a welcome development.

The larger issue here is the continuing failure to undertake economic analyses of all budgetary measures. For example, an announcement pointing to a forthcoming econometric analysis of the impact of €6 billion in austerity measures is glaringly conspicuous by its absence. The absence of serious analysis was a causal factor in the economic crash, and it would be criminally negligent not to learn from past mistakes.

At least six months before each annual budget, the Government of the day should produce a long list of the measures it is considering for the forthcoming budget. Each of these measures should then be subjected to a full cost-benefit analysis by independent economists. Opposition parties should have their own opportunity to submit proposals for analysis. The cost-benefit analysis should seek to quantify the impact of the proposal across a variety of indicators. Sample indicators include (but are not limited to) the impact on:

• Economic growth (short and long-term)

• Employment

• The exchequer borrowing requirement

• Economic equality, for example which groups will gain and which groups will lose

• The at risk of poverty rate and other poverty related indicators

• Quality of life indicators, for example health outcomes

• Aggregate stock and composition of productive physical capacity

• Aggregate stock and composition of human capital

• The national innovative capacity

• The environment

The results of each of the cost-benefit analyses should then be independently peer-reviewed and submitted to the Government two months in advance of the budget. Existing policies, for example tax expenditures, should be subjected to regular ex post analysis. All policy measures should be reviewed twelve months after implementation, and then again every two or three years.

In the run-up to the budget the Government’s chosen set of budget proposals should be submitted to an independent Fiscal Council, set up for the express purpose of ensuring the parameters of the budget are counter-cyclical and consistent with the principle of macroeconomic sustainability.

The Government of the day should also seek to ensure that the principle of multi-annual budgeting becomes standard practice. The publication of multi-annual budgetary frameworks, of the type outlined in the National Recovery Plan, need to become semi-annual events.

None of this in any way precludes or infringes on political or economic debate. Political parties will have different positions on the relative importance of the various indicators and these differences will lead to divergent policy choices.

Impact analysis will improve accountability and transparency in budgetary decisions and will make it more difficult for interest groups to lobby Governments to sneak through legislation that benefits their narrow sectional interest at the expense of the wider society.

An indicative timetable might look like this:

January to March: Passing of Finance Bill through the Dáil

April: Publication of ‘Four Year Budgetary Framework’

June: Publication of Long list of budget proposals

June-October: Cost benefit analyses of the long list

October: Publication of ‘Updated Four year Budgetary Framework’

November: Parameters of the current year’s proposed budget audited by independent fiscal council and findings published

December: Budget

The fiscal council should be a purely advisory body, entirely independent from political parties and from powerful vested interests. For example, this would automatically exclude all economists working in the financial sector (or, indeed, for other sectional interests). Lobbying a member of the fiscal council should be made illegal. Ideally, the head of the fiscal council should be an economist of international renown.

Showing posts with label Budget 2011. Show all posts

Showing posts with label Budget 2011. Show all posts

Wednesday, 26 January 2011

A new emergency Budget

Michael Taft: Whatever about the disputes over facilitating the passage of the Finance Bill, what people want to know is what parties are going to do about it when they get into office. And this is where progressives can stop feuding with each other and get the debate back to where it belongs – showing how Budget 2011 will do such harm to economic recovery and fiscal stability. And, more importantly, what can be done to remove that harm and show how a progressive platform will bring immediate benefit to the economy and living standards.

Here’s one way of doing that: a precondition for entering government should be the enactment of an emergency budget within 60 days based on three concrete pledges:

• Repeal the Universal Social Charge

• Immediately release funds for public investment

• Reverse the cuts in social welfare income and the minimum wage

Let’s go through these three pledges.

Pledge 1: Repeal the Universal Social Charge

The Universal Social Charge (USC) should be repealed and the previous tax regime – the Income Levy and Health Contribution Levy – should be reinstated. This has no budgetary implications as it would be, per Government estimates, fiscally neutral. But the benefit to households and the economy would be considerable:

As seen, low-income earners could benefit by up to €10 per week while higher income groups would lose out. This would help economic growth – low-income earners spend their additional income; high-income earners tend to save.

This platform could be developed. For instance, the Health Contribution Levy, while marinating its former thresholds, could be integrated into the Income Levy which has a more progressive base (e.g. rents and dividends are exempt from the Health Levy). Therefore, abolishing USC could actually be a revenue raising measure.

In addition, further progressive tax measures could be introduced alongside repealing the USC. The Community Platform, TASC, ICTU and other civil society organisations – all have put forward practical and easily implemented proposals in the areas of tax expenditures and extension of levies to capital income.

The total impact of this would be to increase tax revenue further while providing a small stimulus to low-average income households in the form of removing deflationary tax increases.

Pledge 2: Immediately Release Funds for Public Investment

The second pledge would be to immediately release €2 billion for investment – to come from a combination of the Pension Fund and Exchequer cash balances (we still have nearly €30 billion in liquid assets). This would be done in tandem with re-opening negotiations with the IMF/EU to ring-fence our cash and assets for investment/fiscal consolidation purposes.

To ensure it gets on-stream as quickly as possible, this investment would be largely pumped into ‘shovel-ready’ projects at central and local government (a good start would be refurbish every school to best standard in time for autumn classes).

However, we can go beyond ‘bricks and mortars’ – as UNITE has shown: modern information systems, preventative health initiatives, one-on-one tutoring to raise literacy and numeracy skills (both in schools and in the community), loan guarantee schemes for SMEs, etc.

The economy would not get a full year benefit from this increased investment. But let’s assume 50 percent of the total multiplier gets into the economy by year’s end (it will continue to benefit the economy for an additional 5 and a half years):

• 10,000 jobs created directly with an additional 3,000 to 4,000 spin-off jobs

• Reduction in unemployment and related costs

• An additional €350 million in tax revenue

• A GDP boost of 0.75 percent

A big impetus – which would take some time to get off the ground – would be an announcement that a public enterprise company will be established to build a Next Generation Broadband network to reach every household and business by 2015. While publicly-directed and owned, private investment can be leveraged in. This would be a clear signal of intent: that we are going to invest our way to economic recovery and fiscal stability.

Pledge 3: Reverse the cuts in social welfare income and the minimum wage

A pledge to reverse the cuts in social welfare income and the minimum wage should also be non-negotiable. This measure would boost demand and GDP, increase business turnover, protect retail employment and raise tax revenue (e.g. VAT, etc.). Therefore, it would end up costing the Exchequer far less than the headline cost of repealing the social welfare cuts (€397 million) while the reversing the minimum wage will actually boost Exchequer revenue.

There are other measures – minimal in cost but capable of lifting inequitable burdens on those on low incomes while increasing demand:

• Repealing the GMS co-payments – not likely to cost much after administrative savings are taken into account

• Protect all minimum wages – namely, no cut in pay rates and working conditions under Joint Labour Committees

• Increase Family Income Supplement by the amount as in Budget 2010 - €6 per child per week: this will enhance living standards of thousands of low and average income families with children.

Any increase on the public expenditure side would be more than compensated by tax measure introduced on high income groups (under Pledge 1), tax revenue from investment activity (under Pledge 2), and the benefit of higher demand that increasing people’s living standards would produce (under Pledge 3).

Its win-win-win.

* * *

This simple three-point programme does not address all the economic and social issues which progressive parties will have to address in their election manifestos, never mind when they are in government.

However, it would give a short, sharp signal to the electorate about progressive values and priorities. It will show people how people will be better off after 60 days of a progressive government. It will give everyone a clear picture of the medium-term direction of the new government.

And it will give something for progressive to agree over, instead of attacking each other. Such feuding only brings the prospect that more of the same failed economic thinking will dominate in the next government.

And who wants that?

Here’s one way of doing that: a precondition for entering government should be the enactment of an emergency budget within 60 days based on three concrete pledges:

• Repeal the Universal Social Charge

• Immediately release funds for public investment

• Reverse the cuts in social welfare income and the minimum wage

Let’s go through these three pledges.

Pledge 1: Repeal the Universal Social Charge

The Universal Social Charge (USC) should be repealed and the previous tax regime – the Income Levy and Health Contribution Levy – should be reinstated. This has no budgetary implications as it would be, per Government estimates, fiscally neutral. But the benefit to households and the economy would be considerable:

As seen, low-income earners could benefit by up to €10 per week while higher income groups would lose out. This would help economic growth – low-income earners spend their additional income; high-income earners tend to save.

This platform could be developed. For instance, the Health Contribution Levy, while marinating its former thresholds, could be integrated into the Income Levy which has a more progressive base (e.g. rents and dividends are exempt from the Health Levy). Therefore, abolishing USC could actually be a revenue raising measure.

In addition, further progressive tax measures could be introduced alongside repealing the USC. The Community Platform, TASC, ICTU and other civil society organisations – all have put forward practical and easily implemented proposals in the areas of tax expenditures and extension of levies to capital income.

The total impact of this would be to increase tax revenue further while providing a small stimulus to low-average income households in the form of removing deflationary tax increases.

Pledge 2: Immediately Release Funds for Public Investment

The second pledge would be to immediately release €2 billion for investment – to come from a combination of the Pension Fund and Exchequer cash balances (we still have nearly €30 billion in liquid assets). This would be done in tandem with re-opening negotiations with the IMF/EU to ring-fence our cash and assets for investment/fiscal consolidation purposes.

To ensure it gets on-stream as quickly as possible, this investment would be largely pumped into ‘shovel-ready’ projects at central and local government (a good start would be refurbish every school to best standard in time for autumn classes).

However, we can go beyond ‘bricks and mortars’ – as UNITE has shown: modern information systems, preventative health initiatives, one-on-one tutoring to raise literacy and numeracy skills (both in schools and in the community), loan guarantee schemes for SMEs, etc.

The economy would not get a full year benefit from this increased investment. But let’s assume 50 percent of the total multiplier gets into the economy by year’s end (it will continue to benefit the economy for an additional 5 and a half years):

• 10,000 jobs created directly with an additional 3,000 to 4,000 spin-off jobs

• Reduction in unemployment and related costs

• An additional €350 million in tax revenue

• A GDP boost of 0.75 percent

A big impetus – which would take some time to get off the ground – would be an announcement that a public enterprise company will be established to build a Next Generation Broadband network to reach every household and business by 2015. While publicly-directed and owned, private investment can be leveraged in. This would be a clear signal of intent: that we are going to invest our way to economic recovery and fiscal stability.

Pledge 3: Reverse the cuts in social welfare income and the minimum wage

A pledge to reverse the cuts in social welfare income and the minimum wage should also be non-negotiable. This measure would boost demand and GDP, increase business turnover, protect retail employment and raise tax revenue (e.g. VAT, etc.). Therefore, it would end up costing the Exchequer far less than the headline cost of repealing the social welfare cuts (€397 million) while the reversing the minimum wage will actually boost Exchequer revenue.

There are other measures – minimal in cost but capable of lifting inequitable burdens on those on low incomes while increasing demand:

• Repealing the GMS co-payments – not likely to cost much after administrative savings are taken into account

• Protect all minimum wages – namely, no cut in pay rates and working conditions under Joint Labour Committees

• Increase Family Income Supplement by the amount as in Budget 2010 - €6 per child per week: this will enhance living standards of thousands of low and average income families with children.

Any increase on the public expenditure side would be more than compensated by tax measure introduced on high income groups (under Pledge 1), tax revenue from investment activity (under Pledge 2), and the benefit of higher demand that increasing people’s living standards would produce (under Pledge 3).

Its win-win-win.

* * *

This simple three-point programme does not address all the economic and social issues which progressive parties will have to address in their election manifestos, never mind when they are in government.

However, it would give a short, sharp signal to the electorate about progressive values and priorities. It will show people how people will be better off after 60 days of a progressive government. It will give everyone a clear picture of the medium-term direction of the new government.

And it will give something for progressive to agree over, instead of attacking each other. Such feuding only brings the prospect that more of the same failed economic thinking will dominate in the next government.

And who wants that?

Monday, 13 December 2010

Only growth can reduce the debt

Michael Burke: Over on Irish Ecoomy, Karl Whelan has initiated a useful discussion highlighting some of the differences between EU Commission and government forecasts. Very usefully, he has created an open spreadsheet which fleshes out the bones of the forecasts, which allows some of the underlying assumptions to be derived.

Only time will tell whether the EU Commission’s forecasts are more accurate. But they do at least have the merit of internal consistency, whereas DoF forecasts have none.

In relation to underlying (non-bank) deficit, the EU forecast a deficit of €16.4bn in 2011. Assuming an underlying deficit of €18.9bn in the current year, this implies that a €6bn ‘fiscal adjustment’ leads to actual deficit-reduction of €2.5bn. Likewise another package of cuts in 2012 amounting to €3.6bn leads to actual deficit-reduction of €1.5bn. In both cases the ratio is the same 1:2.4, €1bn in savings requires €2.4b in cuts/tax increases.

Contrast this with the DoF 1:1.6 in 2011, and an unfeasibly high 1:1.24 in 2012, that is cuts of €3.6bn could lead to a lower deficit of €2.9bn.

The facts are that cuts and tax increases in 2008/10 of €14.6bn led to a wider, not narrower deficit. So in both instances the Commission and the DoF are assuming a much less negative effect on government finances than has actually been the case.

But at least the Commission’s forecasts are at least within the spectrum of reasonable discussion and have the merit of consistency. Neither could be said for the DoF forecasts.

The (23yr old, single) laid off public sector worker previously on €35,000 pa was paying €6,500 a year in direct taxes and is now receiving €7,500 in JSA. At least another €2,000 is lost in VAT receipts on her lower consumption. So, without any account of the wider impact on the economy from this reduction in her output, or the incomes or consumption of others, or other welfare benefits to which she may be entitled, from just the direct effects alone, the gross saving for the government of €35,000 in spending cuts becomes a net saving of just €19,000. A ratio of 1:1.84.

Turning to the EU forecasts alone, it should be clear where the deficit-reduction is coming from. The forecasts are for nominal GDP to increase by €2bn in 2011 and by €4.3bn in 2012. At the same time, the deficit is expected to fall €2.5bn and €1.5bn in those years.

If the assumption is that the growth contribution to changes in government finances were simply the government’s share of total revenues (approx 35%), then growth would be responsible for €700mn of the deficit-reduction in 2011 and €1.5bn in 2012 (the entirety of the deficit-reduction in 2012).

However, this assumption reproduces a commonplace error. The sensitivity of the government finances to changes in GDP is a combination of the marginal tax take (not the average tax rate) plus the sensitivity of government outlays to changes in output (primarily changes in welfare payments). The DoF estimates these together total 0.6 (which seems to be an underestimate in current circumstances).

Using the DoF sensitivity estimate of 0.6, in 2011 growth would be responsible for €1.2bn or nearly half the total forecast deficit reduction, while in 2012 it would account for nearly €2.6bn in deficit-reduction, much greater than the anticipated level of €1.5bn. The measures themselves off-set this growth effect and are counter-productive.

If there is to be any deficit-reduction at all it can only come from growth. The EU forecasts demonstrate that deficit reduction over anything but the very short-term is entirely a function of growth. ‘Austerity’ measures run counter to promoting growth and are likely to lead to counter-productive increases in the deficit. Again.

Only time will tell whether the EU Commission’s forecasts are more accurate. But they do at least have the merit of internal consistency, whereas DoF forecasts have none.

In relation to underlying (non-bank) deficit, the EU forecast a deficit of €16.4bn in 2011. Assuming an underlying deficit of €18.9bn in the current year, this implies that a €6bn ‘fiscal adjustment’ leads to actual deficit-reduction of €2.5bn. Likewise another package of cuts in 2012 amounting to €3.6bn leads to actual deficit-reduction of €1.5bn. In both cases the ratio is the same 1:2.4, €1bn in savings requires €2.4b in cuts/tax increases.

Contrast this with the DoF 1:1.6 in 2011, and an unfeasibly high 1:1.24 in 2012, that is cuts of €3.6bn could lead to a lower deficit of €2.9bn.

The facts are that cuts and tax increases in 2008/10 of €14.6bn led to a wider, not narrower deficit. So in both instances the Commission and the DoF are assuming a much less negative effect on government finances than has actually been the case.

But at least the Commission’s forecasts are at least within the spectrum of reasonable discussion and have the merit of consistency. Neither could be said for the DoF forecasts.

The (23yr old, single) laid off public sector worker previously on €35,000 pa was paying €6,500 a year in direct taxes and is now receiving €7,500 in JSA. At least another €2,000 is lost in VAT receipts on her lower consumption. So, without any account of the wider impact on the economy from this reduction in her output, or the incomes or consumption of others, or other welfare benefits to which she may be entitled, from just the direct effects alone, the gross saving for the government of €35,000 in spending cuts becomes a net saving of just €19,000. A ratio of 1:1.84.

Turning to the EU forecasts alone, it should be clear where the deficit-reduction is coming from. The forecasts are for nominal GDP to increase by €2bn in 2011 and by €4.3bn in 2012. At the same time, the deficit is expected to fall €2.5bn and €1.5bn in those years.

If the assumption is that the growth contribution to changes in government finances were simply the government’s share of total revenues (approx 35%), then growth would be responsible for €700mn of the deficit-reduction in 2011 and €1.5bn in 2012 (the entirety of the deficit-reduction in 2012).

However, this assumption reproduces a commonplace error. The sensitivity of the government finances to changes in GDP is a combination of the marginal tax take (not the average tax rate) plus the sensitivity of government outlays to changes in output (primarily changes in welfare payments). The DoF estimates these together total 0.6 (which seems to be an underestimate in current circumstances).

Using the DoF sensitivity estimate of 0.6, in 2011 growth would be responsible for €1.2bn or nearly half the total forecast deficit reduction, while in 2012 it would account for nearly €2.6bn in deficit-reduction, much greater than the anticipated level of €1.5bn. The measures themselves off-set this growth effect and are counter-productive.

If there is to be any deficit-reduction at all it can only come from growth. The EU forecasts demonstrate that deficit reduction over anything but the very short-term is entirely a function of growth. ‘Austerity’ measures run counter to promoting growth and are likely to lead to counter-productive increases in the deficit. Again.

Beware economists bearing models

The following is abridged from a post that appears on Notes on the Front. See also Nat O'Connor's post here.

Michael Taft: So the 2011 budget is reasonably progressive. Indeed, budgets over the last two years have been reasonably progressive. And to prove all this, the ESRI researchers ran the numbers through their Switch tax/benefit model. It tells some useful things.

But does it tell us how the 2011 budget impacted on people’s living standards? No.

A major omission in the ESRI model is that it assumes disposable income is, by implication, equivalent to ‘living standards’. For instance, they claim that the top quintile experienced a -2.7 percent fall in their disposable income, while the bottom quintile experienced a -2.8 percent. Okay, not progressive; just neutral. But is it?

Out of our disposable incomes we must pay for necessities that we may have little cost-control over. For instance, we need housing, food, electricity, gas, telephone, etc. Therefore, our disposable (after-tax) income can be broken into two elements:

• Non-discretionary disposable income – which is spent on necessities which we have little cost-control over.

• Discretionary disposable income – the amount after both tax and necessities.

The CSO’s Household Budget Survey 2005 puts some numbers on this distinction (the following is indicative - a new Survey will be out soon). And I take only three necessities: housing, food and utilities (fuel, light and fixed-line telephone). We find:

• The bottom quintile spends approximately 58 percent on these necessities (or non-discretionary disposable income).

• The top quintile spends approximately 22.2 percent

So what happens when we apply the ESRI’s fall in disposable incomes to ‘discretionary disposable income’ (that is, after payments for necessities are made)?

The bottom quintile experiences a fall of approximately -6.5 percent while the top quintile is only hit for -3.5 percent.

Even this doesn’t fully measure living standards. A household with surplus income will more easily absorb a fall in disposable income than those who have a deficit (i.e. spends more than they take in).

Again, the Household Budget Survey shows that the poorest households experience the worst deficit at -37 percent; the highest income households had a surplus of 26 percent. High income households can easily absorb substantially higher falls in disposable income than the rest of the population without denting their life-styles.

These are other data must be integrated into any model if we are to get a more accurate measurement of budgetary impacts on living standards. In addition, we must take care to integrate ‘real-life’ wage and income increases. For instance, the CSO shows the decline in average weekly earnings over the last six quarters, 18 months:

• Management / Professionals: -1.1 percent

• Clerical / Secretarial: -6.2 percent

• Production workers: -6.6 percent

Add in the estimate increase in non-wage income next year (29 percent according to the ESRI) and we can see that those on high incomes have been able to protect their living standards (and in some cases, even enhance them) to a much greater extent than the vast majority of workers.

It is incumbent upon the ESRI to produce its full findings, rather than just a newspaper article. It cannot expect the public to accept its findings on faith. We have learned the harsh truth about models.

We know, for instance, that the Government’s model was flawed – fatally so. We also know the considerable limitations of the ESRI’s Hermes model, upon which researchers were actually suggesting only a few months ago, that the Irish economy could return to near full-employment by 2015. We know these were badly mistaken.

At the end of the day, the ESRI’s Switch model cannot tell us about impacts on living standards for it doesn’t seek to do so. It only gives us model-driven data to contribute one piece of a very large, more complex puzzle.

The ESRI started its article by asking the question: ‘Was Budget 2011 fair?’ After reading the article, we are no wiser.

Michael Taft: So the 2011 budget is reasonably progressive. Indeed, budgets over the last two years have been reasonably progressive. And to prove all this, the ESRI researchers ran the numbers through their Switch tax/benefit model. It tells some useful things.

But does it tell us how the 2011 budget impacted on people’s living standards? No.

A major omission in the ESRI model is that it assumes disposable income is, by implication, equivalent to ‘living standards’. For instance, they claim that the top quintile experienced a -2.7 percent fall in their disposable income, while the bottom quintile experienced a -2.8 percent. Okay, not progressive; just neutral. But is it?

Out of our disposable incomes we must pay for necessities that we may have little cost-control over. For instance, we need housing, food, electricity, gas, telephone, etc. Therefore, our disposable (after-tax) income can be broken into two elements:

• Non-discretionary disposable income – which is spent on necessities which we have little cost-control over.

• Discretionary disposable income – the amount after both tax and necessities.

The CSO’s Household Budget Survey 2005 puts some numbers on this distinction (the following is indicative - a new Survey will be out soon). And I take only three necessities: housing, food and utilities (fuel, light and fixed-line telephone). We find:

• The bottom quintile spends approximately 58 percent on these necessities (or non-discretionary disposable income).

• The top quintile spends approximately 22.2 percent

So what happens when we apply the ESRI’s fall in disposable incomes to ‘discretionary disposable income’ (that is, after payments for necessities are made)?

The bottom quintile experiences a fall of approximately -6.5 percent while the top quintile is only hit for -3.5 percent.

Even this doesn’t fully measure living standards. A household with surplus income will more easily absorb a fall in disposable income than those who have a deficit (i.e. spends more than they take in).

Again, the Household Budget Survey shows that the poorest households experience the worst deficit at -37 percent; the highest income households had a surplus of 26 percent. High income households can easily absorb substantially higher falls in disposable income than the rest of the population without denting their life-styles.

These are other data must be integrated into any model if we are to get a more accurate measurement of budgetary impacts on living standards. In addition, we must take care to integrate ‘real-life’ wage and income increases. For instance, the CSO shows the decline in average weekly earnings over the last six quarters, 18 months:

• Management / Professionals: -1.1 percent

• Clerical / Secretarial: -6.2 percent

• Production workers: -6.6 percent

Add in the estimate increase in non-wage income next year (29 percent according to the ESRI) and we can see that those on high incomes have been able to protect their living standards (and in some cases, even enhance them) to a much greater extent than the vast majority of workers.

It is incumbent upon the ESRI to produce its full findings, rather than just a newspaper article. It cannot expect the public to accept its findings on faith. We have learned the harsh truth about models.

We know, for instance, that the Government’s model was flawed – fatally so. We also know the considerable limitations of the ESRI’s Hermes model, upon which researchers were actually suggesting only a few months ago, that the Irish economy could return to near full-employment by 2015. We know these were badly mistaken.

At the end of the day, the ESRI’s Switch model cannot tell us about impacts on living standards for it doesn’t seek to do so. It only gives us model-driven data to contribute one piece of a very large, more complex puzzle.

The ESRI started its article by asking the question: ‘Was Budget 2011 fair?’ After reading the article, we are no wiser.

Friday, 10 December 2010

Progressive Austerity?

Nat O'Connor: There has been a flurry of calculations about the effect of Budget 2011. One technical, but important, point is that our income tax system (inclusive of PRSI and USC) is now less progressive than it was last year.

Nearly everyone pays more tax due to Budget 2011 (except for the self-employed earning over €200,000) but the extent to which 'those who have more will pay more' is lessened.

Some ESRI economists argue that the cumulative effect of now four austerity budgets since the crisis began has hit higher earners more.

Their chart, invisible on the online version, looks like this:

Q1, Q2, etc stands for the income quintiles. The chart shows that those in the lowest quintile are hit most in 2011, but the authors' argument is that higher quintiles have been hit more when all four budgets' effects are combined.

There is an important caveat in the Irish Times article: "Our analysis does not include the wage or employment effects of the reduction in the minimum national minimum wage." This obviously matters a lot to people in the lowest quintile, and potentially to some in the second quintile, whose earnings are linked with the minimum wage.

This example highlights that any model or calculation of the budgetary effects rests on a number of assumptions. The Irish Times article only skims the surface of the technical details of their analysis, but one question which I raise below is the extent to which they assume tax reliefs that already erode the progressivity of the income tax system. They state that they include changes to pension tax relief, among other variables, which is open to challenge.

Similarly, the official Budget documentation provides 12 example household types and how they are affected by tax changes (in Annex A). However, these examples are neither complete nor balanced.

For example, there are no examples of married couples with two earners, and the tables stop at earnings over €175,000; thus failing to illustrate that self-employed people on over €200,000 are in fact better off after tax and social insurance changes in Budget 2011. Also, an unrealistic assumption is made that a six per cent pension contribution is made by workers, regardless of their income. Firstly, the evidence shows that less than half of Irish workers have a private pension. Secondly, it is unrealistic to assume that workers on low gross incomes can afford to save anything, in the context of the current cost of living. Therefore, the examples and the changes in net income they illustrate must be regarded as inaccurate and misleading, which is a serious concern when it occurs in the official Budget documentation.

One way to get to the bottom of this, is to identify the 'baseline' tax system; that is, the bare bones of the tax system.

In the case of income tax, I argue that the baseline system is composed of three elements: the rates (20% and 41%), the bands (e.g. single people pay 41% from €32,800 upwards) and the basic credits (e.g. single person 1,650). I also add in the basic PRSI, USC, etc rates.

Everything else is an addition or modification of the baseline tax system, including the PAYE tax credit, pension tax relief, etc. A problem with the ESRI-SWITCH and Budget calculations of income change from the budget is that a number of tax reliefs have been 'absorbed' into the baseline tax system. In fairness, the SILC data used in the SWITCH model may have an empirical basis for who uses what tax reliefs, but making these assumptions can easily include normative judgements about what's 'normal' tax relief versus what is in effect a 'bonus'.

I argue that tax reliefs (beyond the basic single person or married credits) are a bonus. Someone using reliefs is paying less than the full amount of tax they should otherwise be paying, based on their income level. This, in turn, lessens the progressivity of the tax system. As such, the loss of a tax relief bonus is not the same thing as an actual increase in someone’s tax liability, such as occurred with the rate and band changes in Budget 2011.

Progressivity in the baseline tax system can be simply measured as to whether someone on a higher income pays not just more tax, but a proportionately higher part of their income. And, as the figure below illustrates, this is indeed the case (blue triangles for 2011, red squares for 2010).

Of course, what the curves illustrate is only the baseline, theoretical progressivity of the tax system. When people use tax reliefs, additional credits, etc. the level of effective tax they pay is reduced and progressivity in the tax system is likewise reduced. And we use a great deal of tax relief in Ireland.

What the figure also illustrates is that, with Budget 2011, the curve is slightly flatter in 2011 than in the previous year. That is, the overall effect of income tax (including USC and PRSI) is less progressive. Everyone pays more tax, and a higher proportion of their incomes, but those on higher incomes see their proportion rise by less than those on lower incomes. For example, someone on €40,000 pays 3.6 per cent more in tax/charges, whereas someone on €200,000 only pays an extra 2.2 per cent.

And at a certain point in time, percentage increases and decreases are not useful comparators. For example, a ten per cent income cut for someone on €200,000 is €20,000; whereas ten per cent for someone on €20,000 is €2,000. Yet, the person on the lower income might suffer more hardship than the person who remains on a very high income of €180,000. Hence, we need to move beyond comparing the percentage changes for different income groups and start asking how much money do people need to live a decent life.

The data used in my line chart is as follows. The 2010 position (single PAYE workers, with no children, paying the income levy, health levy, PRSI and income tax):

The 2011 position (single PAYE workers, with no children, paying the Universal Social Charge, PRSI and income tax):

A further point is that many of the real, material effects of Budget 2011 do not manifest as changes to income. Economic equality can be measured as the combined effect of wealth, income, costs and public services on a person’s total net ‘benefit’ from the economy. Budget 2011 affects all four dimensions of economic equality, but some of the Budget’s implications are not immediately obvious. For example, while the Budget makes immediate changes to tax and social welfare, changing people’s incomes, it also sets the available resources for different Government Departments. It will only be as 2011 progresses that people will see the erosion of local services, such as libraries, roads, public transport, as well as a reduction in the resources available to community groups, etc. These cuts to public spending will impinge upon economic equality, with those on the lowest incomes again most badly affected, because they are more reliant on public services.

There is a lack of distributional analysis in the Budget documentation, which is a major flaw. More sophisticated analysis is required to guage the full extent to which budgetary changes affect different people in society.

Nearly everyone pays more tax due to Budget 2011 (except for the self-employed earning over €200,000) but the extent to which 'those who have more will pay more' is lessened.

Some ESRI economists argue that the cumulative effect of now four austerity budgets since the crisis began has hit higher earners more.

Their chart, invisible on the online version, looks like this:

Q1, Q2, etc stands for the income quintiles. The chart shows that those in the lowest quintile are hit most in 2011, but the authors' argument is that higher quintiles have been hit more when all four budgets' effects are combined.

There is an important caveat in the Irish Times article: "Our analysis does not include the wage or employment effects of the reduction in the minimum national minimum wage." This obviously matters a lot to people in the lowest quintile, and potentially to some in the second quintile, whose earnings are linked with the minimum wage.

This example highlights that any model or calculation of the budgetary effects rests on a number of assumptions. The Irish Times article only skims the surface of the technical details of their analysis, but one question which I raise below is the extent to which they assume tax reliefs that already erode the progressivity of the income tax system. They state that they include changes to pension tax relief, among other variables, which is open to challenge.

Similarly, the official Budget documentation provides 12 example household types and how they are affected by tax changes (in Annex A). However, these examples are neither complete nor balanced.

For example, there are no examples of married couples with two earners, and the tables stop at earnings over €175,000; thus failing to illustrate that self-employed people on over €200,000 are in fact better off after tax and social insurance changes in Budget 2011. Also, an unrealistic assumption is made that a six per cent pension contribution is made by workers, regardless of their income. Firstly, the evidence shows that less than half of Irish workers have a private pension. Secondly, it is unrealistic to assume that workers on low gross incomes can afford to save anything, in the context of the current cost of living. Therefore, the examples and the changes in net income they illustrate must be regarded as inaccurate and misleading, which is a serious concern when it occurs in the official Budget documentation.

One way to get to the bottom of this, is to identify the 'baseline' tax system; that is, the bare bones of the tax system.

In the case of income tax, I argue that the baseline system is composed of three elements: the rates (20% and 41%), the bands (e.g. single people pay 41% from €32,800 upwards) and the basic credits (e.g. single person 1,650). I also add in the basic PRSI, USC, etc rates.

Everything else is an addition or modification of the baseline tax system, including the PAYE tax credit, pension tax relief, etc. A problem with the ESRI-SWITCH and Budget calculations of income change from the budget is that a number of tax reliefs have been 'absorbed' into the baseline tax system. In fairness, the SILC data used in the SWITCH model may have an empirical basis for who uses what tax reliefs, but making these assumptions can easily include normative judgements about what's 'normal' tax relief versus what is in effect a 'bonus'.

I argue that tax reliefs (beyond the basic single person or married credits) are a bonus. Someone using reliefs is paying less than the full amount of tax they should otherwise be paying, based on their income level. This, in turn, lessens the progressivity of the tax system. As such, the loss of a tax relief bonus is not the same thing as an actual increase in someone’s tax liability, such as occurred with the rate and band changes in Budget 2011.

Progressivity in the baseline tax system can be simply measured as to whether someone on a higher income pays not just more tax, but a proportionately higher part of their income. And, as the figure below illustrates, this is indeed the case (blue triangles for 2011, red squares for 2010).

Of course, what the curves illustrate is only the baseline, theoretical progressivity of the tax system. When people use tax reliefs, additional credits, etc. the level of effective tax they pay is reduced and progressivity in the tax system is likewise reduced. And we use a great deal of tax relief in Ireland.

What the figure also illustrates is that, with Budget 2011, the curve is slightly flatter in 2011 than in the previous year. That is, the overall effect of income tax (including USC and PRSI) is less progressive. Everyone pays more tax, and a higher proportion of their incomes, but those on higher incomes see their proportion rise by less than those on lower incomes. For example, someone on €40,000 pays 3.6 per cent more in tax/charges, whereas someone on €200,000 only pays an extra 2.2 per cent.

And at a certain point in time, percentage increases and decreases are not useful comparators. For example, a ten per cent income cut for someone on €200,000 is €20,000; whereas ten per cent for someone on €20,000 is €2,000. Yet, the person on the lower income might suffer more hardship than the person who remains on a very high income of €180,000. Hence, we need to move beyond comparing the percentage changes for different income groups and start asking how much money do people need to live a decent life.

The data used in my line chart is as follows. The 2010 position (single PAYE workers, with no children, paying the income levy, health levy, PRSI and income tax):

The 2011 position (single PAYE workers, with no children, paying the Universal Social Charge, PRSI and income tax):

A further point is that many of the real, material effects of Budget 2011 do not manifest as changes to income. Economic equality can be measured as the combined effect of wealth, income, costs and public services on a person’s total net ‘benefit’ from the economy. Budget 2011 affects all four dimensions of economic equality, but some of the Budget’s implications are not immediately obvious. For example, while the Budget makes immediate changes to tax and social welfare, changing people’s incomes, it also sets the available resources for different Government Departments. It will only be as 2011 progresses that people will see the erosion of local services, such as libraries, roads, public transport, as well as a reduction in the resources available to community groups, etc. These cuts to public spending will impinge upon economic equality, with those on the lowest incomes again most badly affected, because they are more reliant on public services.

There is a lack of distributional analysis in the Budget documentation, which is a major flaw. More sophisticated analysis is required to guage the full extent to which budgetary changes affect different people in society.

Thursday, 9 December 2010

TASC analysis of Budget 2011

TASC has issued its analysis of Budget 2011; you can download a PDF of the document here. Comments?

Wednesday, 8 December 2010

A Merry Christmas for plutocrats

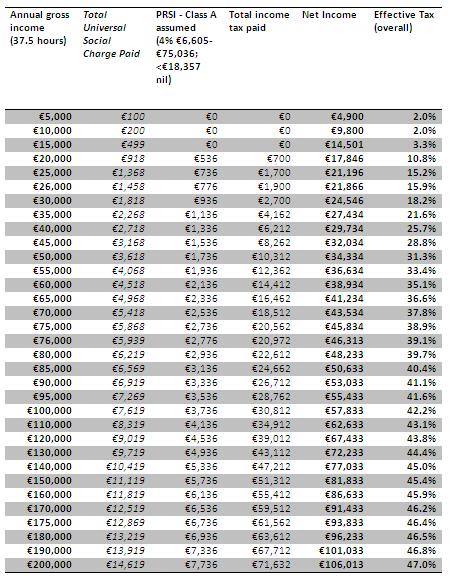

Tom McDonnell: TASC will be releasing a full budget response tomorrow. In the meantime feast your eyes on some good news for all of you single, non-PAYE workers on €200,000 or more. I have followed the Government’s practice of assuming a 6% pension contribution. You can do the calculations yourself using the deloitte tax calculator. See table below the fold, and click to enlarge.

Budget 2011: biggest fiscal consolidation ever

Paul Sweeney: The 2011 Budget is the biggest fiscal consolidation imposed by any government in the developed world since the Second World War. It dwarfs the consolidation under McSharry back in the late Eighties and far exceeds the biggest adjustment in another country - that of Denmark in the mid Eighties. We have heard of the Finnish adjustment after its exports collapsed with the fall of the Soviet Union in the early 1990s, but that was a fraction of this adjustment.

Based on a recent paper by Alesina, Carloni and Lecce, the following emerges. In terms of Ireland’s fiscal adjustment under McSharry, undoing the tax cuts and heavy public spending policies after the 1977 Election, the 4-year adjustment 1986-89 cumulatively was -4.82% of GDP and averaged -1.21%. Finland’s was a four year period of pain and was 6.23%. This averaged just over -1% a year over the six years, 1993-98.

The largest fiscal consolidation was in Denmark and it lasted 4 years between 1983 and 1986, averaging a savage -2.43% consolidation of cuts and tax rises a year.

So with the savage adjustment of €6bn in cuts with some tax rises, which is 4.7% of GNP (4% of GDP) Ireland’s Fianna Fail/Green Government wins the shocking economic prize as the world’s leading (lagging?) deflating government. The total adjustment is to be €29.6bn over the 6.5 years from mid 2008 to 2014 inclusive, (p 6 of Lenihan’s speech) or 23.3% of GNP in 2010 or 2011. The average will be somewhat less at a still massive 4.55% year from mid 2008 to end 2014. This is some pain to be inflicted upon the Irish people.

From a quick read of the EU’s 1st Review of the Greek Economic Adjustment Programme, it appears that the total consolidation will be 8% of GDP over 4 years and the IMF/EU MOU states that the will be 3.2% in 2011 (4.3% if carryovers from 2010 are added in).

As this is a blog post and written quickly, I suggest further study is undertaken by academic economists to see if this is correct and to develop it. It does seem that this Government is making economic history – for all the very wrong reasons!

“We all partied” say some in the commentariat and so we all must pay. Of course, that is untrue and many did not rise in the rising tide of the Domestically-Induced Boom of 2002-08.

But why should the poorest pay most, as per this incredibly regressive Budget? Of course, we may later have the ESRI or some body cited on this Budget to “prove” how progressive it is. But such a study will only examine some aspects of the total package, like income tax and welfare, and it will omit (by necessity of complexity), for example, various charges, indirect taxes, or the failure of Government to insist that the corporate sector step up to the plate in this deep crisis and contribute even 2% of profits (only profits made) which would contribute €630m a year to running this debt-ridden country, the one in which they are happy to operate in.

It was corporate Ireland – specifically the banks, which all but destroyed this economy. And these banks were “governed” by the heads of Ireland leading corporations, heads of public bodies, top advisors and lawyers from the big firms etc., as TASC’s “Mapping the Golden Circle” demonstrates. Thus when you hear calls for public sector reform, modify them to institutional or corporate reform for both public and private sectors.

Alesina et al’s paper is ironically called “The Electoral Consequences of Large Fiscal Adjustments. It is available on Alesina’s website at Harvard.

In this paper they also suggest that “tax-based adjustments” (over cuts) make it more difficult for incumbent governments to be reappointed when they implement large fiscal adjustments. Alesina is criticised on this important point of the supposed superiority of cuts over tax rises by others, including even the IMF in its recent Outlook paper.

Aleseni is often cited by proponents of cuts vs taxes. Lenihan’s Budget statement cites “economic theory” as supporting cuts over taxes. It is of course the liberal economic view, that is the view from a certain side of the house!

In my opinion, this Budget is perhaps the first Irish Budget to be so overtly informed, if that is not too flattering a word, in the language of liberal economic theory. Of course, all Irish Budgets since 1998 have been strong models of this perspective, moderated with some social democratic values. But it was largely the pro-cyclical, direct tax-cutting and de-regulation which led to Ireland’s economic Crash of 2008 and our downfall continues with this Budget.

Last year in his Budget, Mr Lenihan promised “we are on the road to recovery.” Yeah? He concluded by asserting that “our plan is working.” He then asserted that “We have turned the corner”. Green shoots? Where?

With the biggest deflationary Budget in the western world, with this saturation bombing, it will be many years before there are any “green shoots”.

Based on a recent paper by Alesina, Carloni and Lecce, the following emerges. In terms of Ireland’s fiscal adjustment under McSharry, undoing the tax cuts and heavy public spending policies after the 1977 Election, the 4-year adjustment 1986-89 cumulatively was -4.82% of GDP and averaged -1.21%. Finland’s was a four year period of pain and was 6.23%. This averaged just over -1% a year over the six years, 1993-98.

The largest fiscal consolidation was in Denmark and it lasted 4 years between 1983 and 1986, averaging a savage -2.43% consolidation of cuts and tax rises a year.

So with the savage adjustment of €6bn in cuts with some tax rises, which is 4.7% of GNP (4% of GDP) Ireland’s Fianna Fail/Green Government wins the shocking economic prize as the world’s leading (lagging?) deflating government. The total adjustment is to be €29.6bn over the 6.5 years from mid 2008 to 2014 inclusive, (p 6 of Lenihan’s speech) or 23.3% of GNP in 2010 or 2011. The average will be somewhat less at a still massive 4.55% year from mid 2008 to end 2014. This is some pain to be inflicted upon the Irish people.

From a quick read of the EU’s 1st Review of the Greek Economic Adjustment Programme, it appears that the total consolidation will be 8% of GDP over 4 years and the IMF/EU MOU states that the will be 3.2% in 2011 (4.3% if carryovers from 2010 are added in).

As this is a blog post and written quickly, I suggest further study is undertaken by academic economists to see if this is correct and to develop it. It does seem that this Government is making economic history – for all the very wrong reasons!

“We all partied” say some in the commentariat and so we all must pay. Of course, that is untrue and many did not rise in the rising tide of the Domestically-Induced Boom of 2002-08.

But why should the poorest pay most, as per this incredibly regressive Budget? Of course, we may later have the ESRI or some body cited on this Budget to “prove” how progressive it is. But such a study will only examine some aspects of the total package, like income tax and welfare, and it will omit (by necessity of complexity), for example, various charges, indirect taxes, or the failure of Government to insist that the corporate sector step up to the plate in this deep crisis and contribute even 2% of profits (only profits made) which would contribute €630m a year to running this debt-ridden country, the one in which they are happy to operate in.

It was corporate Ireland – specifically the banks, which all but destroyed this economy. And these banks were “governed” by the heads of Ireland leading corporations, heads of public bodies, top advisors and lawyers from the big firms etc., as TASC’s “Mapping the Golden Circle” demonstrates. Thus when you hear calls for public sector reform, modify them to institutional or corporate reform for both public and private sectors.

Alesina et al’s paper is ironically called “The Electoral Consequences of Large Fiscal Adjustments. It is available on Alesina’s website at Harvard.

In this paper they also suggest that “tax-based adjustments” (over cuts) make it more difficult for incumbent governments to be reappointed when they implement large fiscal adjustments. Alesina is criticised on this important point of the supposed superiority of cuts over tax rises by others, including even the IMF in its recent Outlook paper.

Aleseni is often cited by proponents of cuts vs taxes. Lenihan’s Budget statement cites “economic theory” as supporting cuts over taxes. It is of course the liberal economic view, that is the view from a certain side of the house!

In my opinion, this Budget is perhaps the first Irish Budget to be so overtly informed, if that is not too flattering a word, in the language of liberal economic theory. Of course, all Irish Budgets since 1998 have been strong models of this perspective, moderated with some social democratic values. But it was largely the pro-cyclical, direct tax-cutting and de-regulation which led to Ireland’s economic Crash of 2008 and our downfall continues with this Budget.

Last year in his Budget, Mr Lenihan promised “we are on the road to recovery.” Yeah? He concluded by asserting that “our plan is working.” He then asserted that “We have turned the corner”. Green shoots? Where?

With the biggest deflationary Budget in the western world, with this saturation bombing, it will be many years before there are any “green shoots”.

Michael Burke on the British economy may escape an Irish fate

Writing on the Guardian website, PE blogger Michael Burke points out that "British political leaders, like their co-thinkers in Dublin, have no explanation as to how cuts led to a wider deficit. Yet there is one important difference between the two economies that may yet shelter the British economy from an Irish fate, or at least the dominant section of it. The Irish bailout, like Greece before it, is a form of international loan-sharking, where Europe's banks demand repayment in full of existing debt by means of loading Irish taxpayers with ever-greater debts. These banks are headed by British ones, which hold £140bn in bonds issued by Irish borrowers, the biggest national exposure to Irish debt. Almost unremarked here, but not in Ireland, is that the interest rate on these new EU loans will be approximately 7%, compared with just 3% on IMF loans". You can read the rest of his article here.

Tuesday, 7 December 2010

A budget that does not add up

Slí eile: The annual pantomime known as the Budget is an annual fixture. Since the onset of recession in 2008 it has assumed the proportion of an annual (and sometimes twice a year) catharsis. It is carefully planned and delivered through a series of planted leaks, suggestions, threats, ameliorations, political trading and spin. This year, the atmosphere has been characterised by:

1 recession weariness (in some peoples people have been used to a certain level of shock, awe and fear)

2 the publication of a 'four year plan' to resolve the fiscal impasse

3 a sense that control has passed more than before, to some extent, to forces outside Ireland.

On a first reading and hearing of this year's budget the following is apparent:

the poor, the unemployed, families with children, the sick, the young will take the brunt of the adjustment

public services will be further undermined in a country where the public domain was inadequate

taxes will serve to lower living standards across the board but in a way that will impact in absolute terms very severely on those already struggling on low income

key changes in regard to capital, corporate and consumption taxes were either avoided, postponed or introduced in a very limited way.

as in previous years, the amount and quality of information provided leaves much to be desired -

simple to use and transparent data sheets are not available

the full policy and programme implications of reductions Department by Department and vote sub-head by sub-head remain to be spelt out

the macro-economic impact of these adjustments are not presented (e.g. the deflationary impact on tax flows is not shown or explicitly factored in)

the combined impact on household income for different groups (e.g. by decile) has not been shown

the extent of reparations in the form of capital transactions is difficult to isolate out in the data shown in the background material - this needs to be more clearly shown and set against the cut backs to public services and living standards - the price of reparations for the benefit of unknown investors, bondholders and other creditors.

There is a sense from the opposition benches that in the coming months some aspects of the bigger 'plan' can be revisited and even re-negotiated (with respect to composition, timing and interest payments). The speeches from that side of the house were populist but not indicative of how exactly an alternative economic strategy would work and deliver. The most credible, worked-out and progressive alternative package I have seen to date is that provided by UNITE.

1 recession weariness (in some peoples people have been used to a certain level of shock, awe and fear)

2 the publication of a 'four year plan' to resolve the fiscal impasse

3 a sense that control has passed more than before, to some extent, to forces outside Ireland.

On a first reading and hearing of this year's budget the following is apparent:

the poor, the unemployed, families with children, the sick, the young will take the brunt of the adjustment

public services will be further undermined in a country where the public domain was inadequate

taxes will serve to lower living standards across the board but in a way that will impact in absolute terms very severely on those already struggling on low income

key changes in regard to capital, corporate and consumption taxes were either avoided, postponed or introduced in a very limited way.

as in previous years, the amount and quality of information provided leaves much to be desired -

simple to use and transparent data sheets are not available

the full policy and programme implications of reductions Department by Department and vote sub-head by sub-head remain to be spelt out

the macro-economic impact of these adjustments are not presented (e.g. the deflationary impact on tax flows is not shown or explicitly factored in)

the combined impact on household income for different groups (e.g. by decile) has not been shown

the extent of reparations in the form of capital transactions is difficult to isolate out in the data shown in the background material - this needs to be more clearly shown and set against the cut backs to public services and living standards - the price of reparations for the benefit of unknown investors, bondholders and other creditors.

There is a sense from the opposition benches that in the coming months some aspects of the bigger 'plan' can be revisited and even re-negotiated (with respect to composition, timing and interest payments). The speeches from that side of the house were populist but not indicative of how exactly an alternative economic strategy would work and deliver. The most credible, worked-out and progressive alternative package I have seen to date is that provided by UNITE.

A New Deal moment

Michael Taft: The budget will be nasty, brutal but unfortunately not short. Its effects will last – unless people through their popular organisations put enough pressure on the opposition parties to commit to its repeal. But repeal to what end?

We must demand a New Deal moment – a fundamental break from the existing parameters. You can read about this here.

We must demand a New Deal moment – a fundamental break from the existing parameters. You can read about this here.

Monday, 6 December 2010

Was it for this? II

Michael Burke: Ahead of tomorrow's Budget, it may be worth taking stock and posing the question, How did it come to this?

The Irish Times leader column titled Was It for This? caused something of a stir by contrasting the national humiliation of the EU/ECB/IMF landing party to the expression of national independence in 1916. The editorial paints a confused historical picture of how this debacle came about, but the context, and contrast, is not misplaced.

It is clear from the 4-year and wholly misnamed 'Recovery Plan' that the intention is to bind the citizens of this state and their elected representatives to a set of economic, fiscal and social policies that are designed to be wholly immutable. Tomorrow's Budget will fill in the awful details, but the main elements are already in place.

The documents agreed between the government and the international bodies who are actually in charge also make it abundantly clear whose interests are being represented. It is stated that the IMF portion of the package will command an interest rate of just over 3%. If, as stated, the average interest rate is 5.8%, then the EU, non-IMF portion (two-thirds of the total) must be at a rate close to 7%.

It is further stated that, of the €35bn in further funds for the banks, only €10bn is for their immediate recapitalisation- the remainder is for 'contingencies' in the banking sector (which is almost exactly the same as the NPRF's former level of assets, just to underline who it is here that is being protected. It turns out the NPRF was 'rainy day' money for the banking sector, not its contributors.).

This further lifeblood for what are already zombie banks will cost over €1.7bn annually at a 7% interest rate. This annual cost is a large proportion of the planned cuts to current expenditure in December's Budget (€2.09bn), including social welfare, public sector job losses, public sector pensions and 'other expenditure' on goods and services.

Or, it is amost exactly the same as the planned reduction of €1.8bn in govt. capital expenditure.

Irish taxpayers are being foisted with a near-doubling of the national debt- in the name of debt-reduction. The government aim is to keep alive a failed banking system so that it will not pull the plug on property speculators. But the ultimate beneficiaries are British, German and French banks who will be paid out in full despite the stupidity of their lending and in violation of the free-market principles which they extol. These are the real 'vested interests' which determine policy.

Prophetically, Liam Mellowes once said, "Ireland, if her industries and banks were controlled by foreign capital, would be at the mercy of every breeze that ruffled the surface of the world’s money-markets." His response was, "The Irish Republic stands, therefore, for the ownership of Ireland by the people of Ireland."

The current arrangements are the negation of a Republic.

The Irish Times leader column titled Was It for This? caused something of a stir by contrasting the national humiliation of the EU/ECB/IMF landing party to the expression of national independence in 1916. The editorial paints a confused historical picture of how this debacle came about, but the context, and contrast, is not misplaced.

It is clear from the 4-year and wholly misnamed 'Recovery Plan' that the intention is to bind the citizens of this state and their elected representatives to a set of economic, fiscal and social policies that are designed to be wholly immutable. Tomorrow's Budget will fill in the awful details, but the main elements are already in place.

The documents agreed between the government and the international bodies who are actually in charge also make it abundantly clear whose interests are being represented. It is stated that the IMF portion of the package will command an interest rate of just over 3%. If, as stated, the average interest rate is 5.8%, then the EU, non-IMF portion (two-thirds of the total) must be at a rate close to 7%.

It is further stated that, of the €35bn in further funds for the banks, only €10bn is for their immediate recapitalisation- the remainder is for 'contingencies' in the banking sector (which is almost exactly the same as the NPRF's former level of assets, just to underline who it is here that is being protected. It turns out the NPRF was 'rainy day' money for the banking sector, not its contributors.).

This further lifeblood for what are already zombie banks will cost over €1.7bn annually at a 7% interest rate. This annual cost is a large proportion of the planned cuts to current expenditure in December's Budget (€2.09bn), including social welfare, public sector job losses, public sector pensions and 'other expenditure' on goods and services.

Or, it is amost exactly the same as the planned reduction of €1.8bn in govt. capital expenditure.

Irish taxpayers are being foisted with a near-doubling of the national debt- in the name of debt-reduction. The government aim is to keep alive a failed banking system so that it will not pull the plug on property speculators. But the ultimate beneficiaries are British, German and French banks who will be paid out in full despite the stupidity of their lending and in violation of the free-market principles which they extol. These are the real 'vested interests' which determine policy.

Prophetically, Liam Mellowes once said, "Ireland, if her industries and banks were controlled by foreign capital, would be at the mercy of every breeze that ruffled the surface of the world’s money-markets." His response was, "The Irish Republic stands, therefore, for the ownership of Ireland by the people of Ireland."

The current arrangements are the negation of a Republic.

Wednesday, 10 November 2010

Ireland will not run out of money if the December Budget fails

Nat O'Connor: The front page of The Irish Times runs with the Taoiseach claiming that if the Budget is not passed, the country will run out of money. That is technically untrue.

The Taoiseach is absolutely correct that major fiscal adjustments have to be made this year and in subsequent years, but the evidence does not necessarily weigh behind the current plan of frontloading €6 billion.

The Taoiseach is also correct that if Ireland reached the middle of next year, with no coherent economic strategy and a weak Budget that fudged the issues, we could find ourselves running out of money. He is correct that you can't spend €50 billion a year, if you only bring in €31 billion in tax.

But none of the areas where the Taoiseach is factually correct supports his contention that if the Government's Budget is not passed on December 7, that Ireland will then run out of money.

Under the Constitution, only the Dáil deals with 'money' bills, like the Budget, the Finance Act, etc. The Seanad can only make commentary. So, passing the Budget is down to the Dáil vote.

The Budget could at this point easily fail to be passed, if the Green Party defects, if a very small number of backbench Fianna Fáil TDs vote against it, or if a slightly larger number of pro-Government TDs abstain or don't turn up. This assumes that all the Opposition TDs do turn up, and vote against it.

If the Budget is defeated in the Dáil, what will happen next is very predictable based on Ireland's prior parliamentary history. The Opposition will put down a Motion of No Confidence in the Government, which the Government will counter with a Motion of Confidence in themselves. Under the parliamentary rules, the Government's motion gets to be debated first, so there will be some heated speeches in the Dáil. Then the TDs will vote on the motion. It seems to me highly unlikely that the Government would win such a vote. If they lose the Budget vote, they'll almost certainly lose the confidence vote, and a General Election will be called.

Once the election is called, arrangements will be made for what the now 'caretaker' Government will do in its final weeks. The Opposition may be asked to agree a compromise and pass parts of the Budget. That could go in various ways. Fianna Fáil and Fine Gael might agree an alternative €6 billion adjustment at that point. Alternatively, a wider range of TDs might agree a skeleton Budget that simply ensures money is there so that hospitals, schools, etc will all remain open in January.

Once the election is over, the new Government will then propose, and pass, their own Budget (probably in January). Any new Government must have a working majority in the Dáil, so this New Year Budget would almost certainly pass. Depending on its content - and the economic logic of its approach - the bond markets will react accordingly. If the markets react favourably, the new Government could borrow a relatively small amount in the first quarter to 'test the water' and then go back to the markets again in late summer. As ever, what will matter to the markets is a coherent, sustainable growth strategy to demonstrate that Ireland is serious about generating the funds to pay them back.

The Taoiseach is right that Ireland does need to pass a strong Budget and four-year plan before very early next year. But it does not have to be his Budget.

I would go further and suggest that Ireland could be more likely to 'run out of money' if the Government's planned €6 billion budget is passed. If the austerity measures kill growth and stagnate the economy, and if there is no robust plan on jobs, then the bond markets will demand far too high interest rates, making it effectively impossible for Ireland to borrow. And then we really will run out of money.

The Taoiseach is absolutely correct that major fiscal adjustments have to be made this year and in subsequent years, but the evidence does not necessarily weigh behind the current plan of frontloading €6 billion.

The Taoiseach is also correct that if Ireland reached the middle of next year, with no coherent economic strategy and a weak Budget that fudged the issues, we could find ourselves running out of money. He is correct that you can't spend €50 billion a year, if you only bring in €31 billion in tax.

But none of the areas where the Taoiseach is factually correct supports his contention that if the Government's Budget is not passed on December 7, that Ireland will then run out of money.

Under the Constitution, only the Dáil deals with 'money' bills, like the Budget, the Finance Act, etc. The Seanad can only make commentary. So, passing the Budget is down to the Dáil vote.

The Budget could at this point easily fail to be passed, if the Green Party defects, if a very small number of backbench Fianna Fáil TDs vote against it, or if a slightly larger number of pro-Government TDs abstain or don't turn up. This assumes that all the Opposition TDs do turn up, and vote against it.

If the Budget is defeated in the Dáil, what will happen next is very predictable based on Ireland's prior parliamentary history. The Opposition will put down a Motion of No Confidence in the Government, which the Government will counter with a Motion of Confidence in themselves. Under the parliamentary rules, the Government's motion gets to be debated first, so there will be some heated speeches in the Dáil. Then the TDs will vote on the motion. It seems to me highly unlikely that the Government would win such a vote. If they lose the Budget vote, they'll almost certainly lose the confidence vote, and a General Election will be called.

Once the election is called, arrangements will be made for what the now 'caretaker' Government will do in its final weeks. The Opposition may be asked to agree a compromise and pass parts of the Budget. That could go in various ways. Fianna Fáil and Fine Gael might agree an alternative €6 billion adjustment at that point. Alternatively, a wider range of TDs might agree a skeleton Budget that simply ensures money is there so that hospitals, schools, etc will all remain open in January.

Once the election is over, the new Government will then propose, and pass, their own Budget (probably in January). Any new Government must have a working majority in the Dáil, so this New Year Budget would almost certainly pass. Depending on its content - and the economic logic of its approach - the bond markets will react accordingly. If the markets react favourably, the new Government could borrow a relatively small amount in the first quarter to 'test the water' and then go back to the markets again in late summer. As ever, what will matter to the markets is a coherent, sustainable growth strategy to demonstrate that Ireland is serious about generating the funds to pay them back.

The Taoiseach is right that Ireland does need to pass a strong Budget and four-year plan before very early next year. But it does not have to be his Budget.

I would go further and suggest that Ireland could be more likely to 'run out of money' if the Government's planned €6 billion budget is passed. If the austerity measures kill growth and stagnate the economy, and if there is no robust plan on jobs, then the bond markets will demand far too high interest rates, making it effectively impossible for Ireland to borrow. And then we really will run out of money.

Friday, 5 November 2010

2011, 2014, the Bond Markets and Growth

Nat O'Connor: It seems to me that there is some confusion in the way in which international factors on Ireland's deficit are presented to the general public in the media. In particular, the 'requirement' that Ireland's deficit is reduced to three per cent of GDP by 2014 seems to be confused with the issue of whether it may be too expensive for us to borrow from the bond markets early next year. The financial institutions that lend money to countries (i.e. the 'bond markets') do not care whether Ireland reaches three per cent of GDP by 2014, provided we can show evidence of an ability to repay our borrowings. But in terms of providing this evidence, the deadline for satisfying these lenders may well be early 2011, not end-2014.

Those who are offering to lend money to Ireland at the moment (at high rates of nearly eight per cent) are taking a chance on making big money on these loans; balanced against a heightened risk that this or the next Irish Government will decide not to pay back the loan - or only pay back a portion of it. However, they are not crazy. They would not lend to Ireland (except at extortionate, short-term rates) if they thought that it was highly likely that we would default on the loans. So, we are still in a position where some of these large - and coldly calculating - financial institutions think that they can make money. (That is, they are confident that we will pay back the loans, or at least enough years of interest, to make it worth their while taking the risk). Unfortunately, not enough of them are interested in lending to Ireland, hence we would have to borrow at nearly eight per cent from the small pool of risk-takers who are willing to lend.

However, the institutions that might consider lending to Ireland at lower rates are not necessarily the same financial institutions that would lend at higher rates. Some institutions make more conservative lending decisions, while others go for more risky investments. This is an oversimplification, perhaps, as most will have balanced portfolios, but it hopefully illustrates the point that not all participants in the international bond markets are clones.

The more conservative institutions operating in the bond markets want to see more evidence of ability to pay. That is, they want evidence that Ireland has moved into a period of economic growth that can be sustained. And they want evidence that tax revenue is stable. And they certainly want to see public expenditure reduced over time to what the state can afford, based on its revenue. However, as long as there is evidence that the state is on a sustainable path, it doesn't matter whether it is 2014, 2016 or 2020. All that matters is that Ireland is on a stable growth trajectory and can show that it will be able to pay back the money.