Friday, 30 March 2012

Michael O'Sullivan on the European project

Michael O'Sullivan, author of 'Ireland and the Global question', has an interesting opinion piece in today's Financial Times.

Wednesday, 28 March 2012

Welcome to the inequality cycle

Michael Taft: We are now starting to get data to assess just who in society is getting hit and who is getting by. Of course, we know about unemployment rates, deprivation rates, and income inequality rates. But the CSO’s 2010 Survey of Income and Living Conditions gives us an insight as to who has lost how much in the first two years of the crisis, namely 2009 and 2010. Let’s take a particular look at three deciles – the lowest, the highest and the middle 6th decile.

First, what levels of income are we discussing within these groups?

• The lowest decile includes households with gross incomes of less than €13,249 or less; or approximately €10,000 per adult in the household.

• The middle decile includes households with gross incomes between €37, 467 and €46,561; or approximately between €18,000 and €21,000 per adult in the household. (Question: is this the squeezed middle that the Irish Times series was recently chronicling?).

• The average for the highest household is a gross income of over €171,000; or approximately €62,000 per adult in the household.

For the lowest decile, income levels are extremely low while in the middle decile, incomes are extremely modest. Incomes at the higher level are in another place altogether.

Now, let’s look at disposable income – that is, income after tax.

Nationally, weekly income fell by nearly 12 percent on average. However, as seen the worst hit were those who could least afford it , with the lowest 10 percent income earners experiencing a fall of over 20 percent. The next biggest decline is found in the middle 6th decile. All deciles experienced a fall in double digits with one exception: the highest earners pretty much escaped the impact of the recession.

However, the story is a little more complicated.

In 2009, the lowest decile experienced a minimal impact. It was the middle decile that took the biggest hit with the highest income earners also experiencing a significant decline. However, the picture changed in 2010. The lowest income groups experienced substantial income decline – in this year social transfers were cut. The middle income group suffered further decline. However, the highest income groups returned to growth.

The SILC data shows that income inequality experienced a large rise in 2010, rising from a ratio of 4.3 to 5.5 (the ratio of the income of the top 20 percent to the bottom 20 percent). This was the biggest single year jump in income inequality experienced in any country since the EU started recording this data. In 2010, Ireland ranked 9th in the EU-27 for income inequality.

These trends are likely to continue and may even accelerate. The 2011 budget saw further cuts in social transfers combined with highly regressive tax measures (the USC and the reduction in personal tax credits). The 2012 budget – which the ESRI described as the most regressive of all budgets introduced since the crisis began – will further exacerbate this.

So we have a new cycle to discuss – alongside the deflationary cycle, the debt cycle and the long-term unemployment cycle: the inequality cycle. And this is likely to be as vicious and socially degrading as the others.

First, what levels of income are we discussing within these groups?

• The lowest decile includes households with gross incomes of less than €13,249 or less; or approximately €10,000 per adult in the household.

• The middle decile includes households with gross incomes between €37, 467 and €46,561; or approximately between €18,000 and €21,000 per adult in the household. (Question: is this the squeezed middle that the Irish Times series was recently chronicling?).

• The average for the highest household is a gross income of over €171,000; or approximately €62,000 per adult in the household.

For the lowest decile, income levels are extremely low while in the middle decile, incomes are extremely modest. Incomes at the higher level are in another place altogether.

Now, let’s look at disposable income – that is, income after tax.

Nationally, weekly income fell by nearly 12 percent on average. However, as seen the worst hit were those who could least afford it , with the lowest 10 percent income earners experiencing a fall of over 20 percent. The next biggest decline is found in the middle 6th decile. All deciles experienced a fall in double digits with one exception: the highest earners pretty much escaped the impact of the recession.

However, the story is a little more complicated.

In 2009, the lowest decile experienced a minimal impact. It was the middle decile that took the biggest hit with the highest income earners also experiencing a significant decline. However, the picture changed in 2010. The lowest income groups experienced substantial income decline – in this year social transfers were cut. The middle income group suffered further decline. However, the highest income groups returned to growth.

The SILC data shows that income inequality experienced a large rise in 2010, rising from a ratio of 4.3 to 5.5 (the ratio of the income of the top 20 percent to the bottom 20 percent). This was the biggest single year jump in income inequality experienced in any country since the EU started recording this data. In 2010, Ireland ranked 9th in the EU-27 for income inequality.

These trends are likely to continue and may even accelerate. The 2011 budget saw further cuts in social transfers combined with highly regressive tax measures (the USC and the reduction in personal tax credits). The 2012 budget – which the ESRI described as the most regressive of all budgets introduced since the crisis began – will further exacerbate this.

So we have a new cycle to discuss – alongside the deflationary cycle, the debt cycle and the long-term unemployment cycle: the inequality cycle. And this is likely to be as vicious and socially degrading as the others.

Tuesday, 27 March 2012

There is an alternative and we have choices

Tom Healy: Today the Nevin Economic Research Institute is being launched. The website www.NERInstitute.net contains information about the new Institute as well as download copies of the Quarterly Economic Observer and the Quarterly Economic Facts. Our key message and conclusion based on research to date is that:

* fiscal austerity is killing the domestic economy

* unemployment - especially youth - is the main social problem confronting the EU

* Ireland is still deficient in key areas of infrastructure - energy, water, retrofitting, broadband and provision of early childhood care and education.

* An investment stimulus of €15bn over 5 years would begin to reverse some of the negative impacts of fiscal austerity to date.

* Such a stimulus could be sourced from public, private and EU (EIB) sources in such a way as to avoid adding to General Government Debt. It could also lower the public sector deficit as a result of tax buoyancy and lower unemployment costs.

* fiscal austerity is killing the domestic economy

* unemployment - especially youth - is the main social problem confronting the EU

* Ireland is still deficient in key areas of infrastructure - energy, water, retrofitting, broadband and provision of early childhood care and education.

* An investment stimulus of €15bn over 5 years would begin to reverse some of the negative impacts of fiscal austerity to date.

* Such a stimulus could be sourced from public, private and EU (EIB) sources in such a way as to avoid adding to General Government Debt. It could also lower the public sector deficit as a result of tax buoyancy and lower unemployment costs.

Monday, 26 March 2012

Dishonesty and the 'structural deficit'

Michael Burke: An article in the Irish Times by Stephen Collins which asserts that the new Treaty “seeks to do is to put an end to the kind of populist and inept fiscal policies that brought Ireland to the brink of ruin” has already drawn strong rebuttals here and here.

It is an entirely valid argument that fiscal policies brought Ireland ‘to the brink of ruin’- but only because the actual sequence of events was that it was the political decision to bail out the failed private sector banks that fatally undermined the state’s finances.

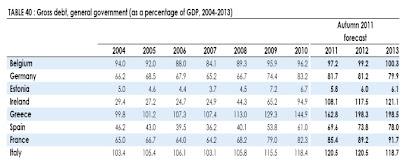

But there is no legitimacy to any suggestion that the new rules would have required successive Irish governments to act in a significantly different manner, until after the crisis hit. The table below shows that the EU commission assessed there was no structural deficit at all until 2007.

It is worth simply pointing out what the EU Commission has recorded on the Irish ‘structural deficit’.

In fact, even this low ‘structural deficit’ is dishonest. It is an example of what statisticians call ‘data-fitting’; that is, adjusting the data to get the desired outcome. Here’s what the Commission was saying in late 2008, after the crisis and the Irish slump had begun. Somehow a 2008 deficit of 4.9% has become a deficit of 7.2%.

The point of the ‘structural deficit’ is that is exceptionally malleable- it can be made to fit almost any desired level at all. In this article, the impeccably mainstream ‘Investor’s Chronicle’ magazine argues that the ‘structural deficit’ is a myth.

Nor was there a debt problem in Ireland which raised any issue regarding the 60% of GDP limit, not until 2009 for Ireland. As can be seen, it was the so-called ‘core’ countries which were the serial offenders on debt levels before the crisis.

The assertion that the new Treaty would have prevented the crisis in Ireland is groundless.

It is an entirely valid argument that fiscal policies brought Ireland ‘to the brink of ruin’- but only because the actual sequence of events was that it was the political decision to bail out the failed private sector banks that fatally undermined the state’s finances.

But there is no legitimacy to any suggestion that the new rules would have required successive Irish governments to act in a significantly different manner, until after the crisis hit. The table below shows that the EU commission assessed there was no structural deficit at all until 2007.

It is worth simply pointing out what the EU Commission has recorded on the Irish ‘structural deficit’.

In fact, even this low ‘structural deficit’ is dishonest. It is an example of what statisticians call ‘data-fitting’; that is, adjusting the data to get the desired outcome. Here’s what the Commission was saying in late 2008, after the crisis and the Irish slump had begun. Somehow a 2008 deficit of 4.9% has become a deficit of 7.2%.

The point of the ‘structural deficit’ is that is exceptionally malleable- it can be made to fit almost any desired level at all. In this article, the impeccably mainstream ‘Investor’s Chronicle’ magazine argues that the ‘structural deficit’ is a myth.

Nor was there a debt problem in Ireland which raised any issue regarding the 60% of GDP limit, not until 2009 for Ireland. As can be seen, it was the so-called ‘core’ countries which were the serial offenders on debt levels before the crisis.

The assertion that the new Treaty would have prevented the crisis in Ireland is groundless.

Friday, 23 March 2012

Government spending policy is deepening the crisis

Michael Burke: The latest national accounts data are worse than they look. The headlines have been about a ‘technical return’ to recession with two quarters of negative growth at the end of 2011. But on two measures, the situation is much worse than the short-term occurrence of a double-dip recession.

• Measured by GDP the economy has been in recession since the end of 2007 and remains €21bn below its peak. This is a decline of 11.6%

• GNP, which excludes the profit flows of overseas multinational corporations, has fallen by €26.3bn, down 17.3%. This takes GNP back to the last century

It remains the case that investment (Gross Fixed Capital Formation, GFCF) is overwhelmingly the source of the slump, having fallen by €23.4bn. This is greater than the decline in GDP and accounts for over 90% of the decline in GNP. Clearly, there can be no recovery without a recovery in investment.

But, acknowledging that all these data are subject to revision, investment is not currently the motor force of the decline. Investment rose in Q4, as did household consumption, according to these initial data. Combined, they added an annualised €2.5bn to growth in the 4th quarter.

The motor force of the slump has become reduced government spending. In the 4th quarter of 2011 government spending fell by €1.9bn in the quarter which is a majority of the total decline of €2.8bn in the period.

The data show the dynamic of the economy. The investment collapse accounts for the slump as a whole. Yet even the tentative increase in investment currently recorded at the end of 2011 is unlikely to persist while there is a contraction in government spending.

The private sector investment strike is the cause of the slump. But government policy is deepening the slump, not alleviating it.

• Measured by GDP the economy has been in recession since the end of 2007 and remains €21bn below its peak. This is a decline of 11.6%

• GNP, which excludes the profit flows of overseas multinational corporations, has fallen by €26.3bn, down 17.3%. This takes GNP back to the last century

It remains the case that investment (Gross Fixed Capital Formation, GFCF) is overwhelmingly the source of the slump, having fallen by €23.4bn. This is greater than the decline in GDP and accounts for over 90% of the decline in GNP. Clearly, there can be no recovery without a recovery in investment.

But, acknowledging that all these data are subject to revision, investment is not currently the motor force of the decline. Investment rose in Q4, as did household consumption, according to these initial data. Combined, they added an annualised €2.5bn to growth in the 4th quarter.

The motor force of the slump has become reduced government spending. In the 4th quarter of 2011 government spending fell by €1.9bn in the quarter which is a majority of the total decline of €2.8bn in the period.

The data show the dynamic of the economy. The investment collapse accounts for the slump as a whole. Yet even the tentative increase in investment currently recorded at the end of 2011 is unlikely to persist while there is a contraction in government spending.

The private sector investment strike is the cause of the slump. But government policy is deepening the slump, not alleviating it.

Thursday, 22 March 2012

Back in recession

Tom Healy: While quarterly national accounts data are always to be taken with caution the latest CSO data clearly indicate a return to recession - technically two quarters in a row. And total domestic demand has fallen by 26% from the peak in late 2007 to the end of 2011. We are now entering the fifth year of domestic recession. This significant 'inflection' point has been dwarfed by Mahon, Promissory Notes and other matters. Paul Krugman has a very telling chart issued a few hours after the CSO release here. A picture tells a lot.

Wednesday, 21 March 2012

Europe from the periphery

Paul Sweeney: These days, Europe appears to be a cold place viewed from the periphery in Ireland. We are being bailed out and supported in many ways by the Troika of the EU, ECB and IMF, but the terms imposed upon citizens largely reflect the liberal economic perspective. We are four long years into austerity. Indicators are no longer falling, but little is rising, particularly green shoots.

At this inauspicious time, a progressive vision for Europe demands a strong focus by progressive parties and organisations on the European Social Model and a clear understanding what is meant by the abused word “competitiveness.” This small western island hjas been laid low by liberal economics but,with European solidarity and support, rather than punishment and austerity, can rebound as a model member state. As progressives, we also need to consciously set out to restore the wage share in national income to improve equity, social cohesions, personal income distribution, longer term wealth distribution, macroeconomic stability and the composition of aggregate demand.

Persuading Voters that the Post-War European Social Compact is Alive and Well

Economic and social progress in Europe since the war has been remarkable. Living standards and improvements in housing, health and peoples’ security have been excellent. There had been a consensus with conservatives that national income and wealth would be shared, but with the prolonged crisis, growing numbers of conservatives no longer want to share. The cake is no longer growing – thanks to their policies - and they want to keep more of it for themselves.

But the best way to grow national income is though social solidarity, education, investment, efficient public services and equitable incomes.

Re-building the European Social Model must be the priority of all progressive forces in Europe. Many Europeans fear that governments are neglecting citizens and are obsessed by appeasing the financial markets; have a very narrow view of “competitiveness”; and with fiscal rectitude. This means that the Post-War European Social Compact appears to be dying or dead for increasing numbers of European citizens.

Apparent confirmation of its death was given by the key unelected European leader, Mario Draghi, who was quoted in the Wall Street Journal earlier this year as saying that “Europe's vaunted social model is "already gone”." Thus a clarion call for all progressive parties must be that the European Social Model is very much alive. Not alone will it continue to be a core objective in progressives’ policy implementation in government, but we should guarantee that the Social Model will be enhanced in line with economic and social progress.

The prolonged ineptitude of European leaders, predominantly conservatives, in dealing with the crisis effectively has undermined public confidence in the European project. The failure of austerity measures has led the same leaders to pursue them with more vigour, instead of learning from their mistakes. The Fiscal Compact will exacerbate the problem.

Mr. Draghi also argued that “austerity, coupled with structural change, is the only option for economic renewal”. Like ancient Greek priests, appeasing the gods with sacrifices, he wants to feed even more of our living standards to the markets, saying "Backtracking on fiscal targets would elicit an immediate reaction by the market."

On top of this deep crisis, there are great challenges with ageing populations straining pensions, rising health costs, environmental issues and much more. There is a hollowing-out of the middle with the growth in “Cool Jobs and Crap Jobs” worldwide. Solid pensionable jobs like banking, computing, parts of accounting, engineering etc. are being de-skilled and outsourced from Europe. The polarisation of jobs is a vital area which has to be addressed.

Some of these challenges may mean doing things very differently, but all can be overcome. Revitalising the Social Model is the key to rebuilding confidence in Europe. One step in this direction is to have a clear understanding of one of the most abused concepts in modern economics- “competitiveness".

Competitiveness is Poorly Understood

The most abused word in modern political economy is “competitiveness.” It is not just that each economist has a different definition, but even the same economist may define it in several ways. For most of them and for many institutions it is simply a description of short-term movements in wages. A more sophisticated definition is of short run movements in unit labour costs, but both are too often ideological, using easily available data to beat up workers and trade unions. This is now a tired abuse of what can be a helpful concept in modern economics in measuring national economic progress. Unless we all subscribe to the same understanding, we must avoid this abused word/concept.

A good definition (as given in the 2003 European Comission Report on Competitiveness) is: “Competitiveness is understood to mean high and rising standards of living of a nation with the lowest possible level of involuntary unemployment on a sustainable basis.” But this does not inform on how to measure it.

I suggest the complexity of the issue is best understood by examining the work of Ireland’s tripartite National Competitiveness Council, which represents unions, employers and Government (albeit with only one-eighth union representation). It produces an annual Benchmarking or Scorecard report covering Ireland’s competitiveness performance in a comprehensive and coherent way. It has a collection of statistical indicators against a whole-of-economy comparison to 17 other economies and the OECD or EU average. Costs and labour costs are included but they are only a small part of the overall measurement of a country’s competitiveness. It is deeply disappointing that sophisticated analysts such as the OECD, IMF etc. still define competitiveness only in terms of unit labour costs. But perhaps it is deliberately ideological?

It is worth remembering that only 9% of EU GDP is exported (measuring the exports in value added, not gross, terms), which means EU countries are very largely competing with themselves. We do buy European, already! However, competitiveness is worth benchmarking, if done properly.

A View from a Troubled Western Island

It is essential to avoid the core/periphery break up in Europe. Ireland grew from one of the poorest of the poor in Europe to one of the richest in twenty years, thanks in no small part to its membership of the Union. It is facing enormous economic problems at present, but provided we get support in facing our staggering and perhaps insurmountable private banking debts, Ireland will recover and revert to become a net contributor to the Union’s funds.

Ireland‘s economic collapse in 2008 was not due to poor competitiveness, nor to public sector profligacy, but to gross irresponsibility by a small elite in the private sector, operating within what had become an ultra-liberal economic system. It was the private banking collapse, which the government foolishly under-wrote which brought Ireland down. Commissioner Rehn demanded, in Latin, “pacta sunt servanda” and in English that the Irish taxpayers “respect your commitments and obligations”. However, these debts are not ours, but those of the private defunct banks, which our sacked government guaranteed, in our name, without our consent.

Prior to this, European banks queued up to lend to our reckless banks, while the ECB looked on benignly. Tax policy – cutting direct taxes on incomes and profits, tax breaks especially for property investment and tax-shifting – also contributed substantially to Ireland’s current economic crisis. The third factor was de-regulation.

Today Irish taxpayers are repaying the bank creditors (EU banks and hedge funds) of the six Irish banks which were socialised. This is an impossible task for 1.8 million people at work, where GDP has collapsed by over 13 per cent between 2008 and 2011, GNP by over 16 per cent and domestic demand by a staggering 24.9 per cent and is still in decline. Unemployment is at 14.6 per cent. When discouraged workers, those who would like to work full time, are included the official figure rises to 25 per cent. Youth unemployment is soaring and long term unemployment is 60.3 of the total.

When the trade unions first met the ECB, EU, IMF Troika in late 2010 when Ireland was placed in Examinership, we pointed out that Ireland has many core strengths, but that the bailout package agreed by the Government with them made the economic recovery very difficult. We said that the deflationary impacts of the measures in the package are such that growth has little chance of reviving. This has been proven to be correct - unless one gives credence to the technical definition of “the end of recession” with a few recent quarters of very weak growth in GDP. It will take many years to makes up for the fall of 13 per cent at current rates, especially with citizens’ taxes diverted to fund the apparently endless private bank bailout.

The previous government tried an experiment in Internal Devaluation because there could be no devaluation in a single currency area. Fortunately, this strategy failed.

Had it worked, the recession would be even worse. It would have sucked more demand out of the economy. Overall, the average employee who remained in work saw no decline in real hourly earnings from the beginning of 2008 when the Crash began. For some workers, in the export and other dynamic sectors, there have been small wage rises. The real losses were the considerable numbers (a huge 14 per cent fall) who lost their jobs. A recent study of how employers dealt with the total wage bill found that there had been cuts, but “however, these cuts were primarily achieved though employment reductions with relatively low contributions at the aggregate level from changes in average hourly earnings and average weekly paid hours” (see Walsh, Kieran “Wage bill change during the recession: how have employers reacted to the downturn?” Statistical and Social Enquiry Society of Ireland, February, 2012)

This relative stability in real incomes of those who kept their jobs since the Crash of 2008 has also been extremely important in ensuing that the terrible collapse in domestic demand – of one quarter in less than four years – was not worse. This is because averagely paid workers generally spend most of their incomes. The last government also cut the minimum wage by 12 per cent but the new government reversed this immediately. It also did not cut welfare rates and there is a deal with the public service whereby there will be no further pay cuts (two of which averaged 14 per cent) provided there is support for substantial change, which is occurring.

The relative stability in real incomes, in welfare rates and in public employment is the key to the explanation of why there has been no rioting in Ireland, despite our travails. It is crucial that the core economies which are performing well, act in solidarity and not in punishment to the underperforming peripherals.

Nor should we entertain the idea of a ‘two speed’ Europe, which could allow an inner core to move towards closer economic and political union supposedly “to protect the Union as a whole.” To move in that direction is to abandon solidarity and to miss this opportunity to build a cohesive Europe.

Restoring the Wage Share of National Income

The share of national income going to wages has fallen considerably in most developed countries since the early 1970s. There has been a slight reversal in recent years, but it is forecast to fall back again. One explanation for the falling labour share and rising share to capital might be that there has been an intensification of capital investment. However, against that, there has been a huge improvement in human capital with all countries seeing major increases in educational and skills attainment. It seems that the investment in human capital is not being rewarded by increases in labour’s share of national income. As less national income is going to workers, this has a secular impact on aggregate demand and thus on growth.

The issue of the decline in labour income share involves equity, social cohesion and personal income distribution, longer-term wealth distribution, macroeconomic stability and the composition of aggregate demand.

The “American Dream” of the next generation enjoying a higher standard of living than their parents has been dead since the early 1970s. Since 1975 US workers’ median incomes have not risen. There are hard lessons to be learned from America. The stagnation in incomes was masked for some time because the working and middle classes borrowed against their homes. Now the home ownership dream has turned into a nightmare for many with negative equity and big debts. It was also masked by a dramatic fall in the prices of many goods now imported from Asia which reduced the cost of living. It was further masked by the growth in dual-income families, where there had only been one earner in the past. Male, unionised and in well paid manufacturing, these American workers had previously seen themselves as firmly in the “middle class”.

The fall in labour’s share of national income was also driven by globalisation, accelerated by technology, falling prices in transport and instant communications. In turn, these trends were accentuated by liberalisation of borders and markets, especially labour markets.

The value of the fall between 1973 and 2011 is substantial in monetary terms. Even with the smallest decline which as in France of 3.5%, it is still a transfer of €71bn from labour’s share of GDP to capital. For Germany it is €137bn.[Click to enlarge table below].

The decline of trade unions and the paucity of vision and lack of ambition in progressive parties, which should be counterforces to such trends, also facilitated the stagnation of incomes of the majority, in spite of economic growth and growth in labour productivity.

There is also a view that corporations and the rich should not have to pay “too much tax” as it is a disincentive to investment. Simultaneously, people are demanding more and better public services, but have been increasingly unwilling to pay for them through taxation. The aversion of many governments and major institutions like the IMF and OECD to progressive income taxes which they now pejoratively term “taxes on labour” means that if acted upon, taxation will fail to be a redistributive mechanism. It also means that the great polarisation of incomes will continue unchecked and citizens will grow even more angry and frustrated.

A Common Fiscal Policy is key to addressing inequality, sorting out the banks and boosting demand by underwriting an EU wide stimulus programme. It may begin with a small budget overall, but a small budget in EU terms is still a lot of cash. I would go for tax coordination rather than harmonisation where member states can set rates, within bands, though a common tax base for companies makes sense in a single market.

Conclusion

The real irony in Europe is that this deep crisis was caused by neo-liberal economic policies. Yet it is conservatives who are in power in most member states. They are prolonging the crisis with the same old failed policies and general incompetence. Some are even reverting to narrow nationalism. Instead, bold action with an EU-wide stimulus and policies informed by a longer term vision of European solidarity is required.

There is a lesson in this for us all. That is to replenish our vision by going back to core ideas, sticking to them in a principled way and being innovative in our policy responses.

Part of this post is based on a a presentation given to a meeting of progressive groups, parties and individuals in the French Parliament on Friday March 16th entitled "The Renaissance of Europe". It was sponsored by four EU think-tanks: FEPF, Jean Jaures, Friedrich Ebert Stiftung and Italianieuropei. This event will be followed by seminars in Rome and Berlin in advance of the Italian and German elections.

At this inauspicious time, a progressive vision for Europe demands a strong focus by progressive parties and organisations on the European Social Model and a clear understanding what is meant by the abused word “competitiveness.” This small western island hjas been laid low by liberal economics but,with European solidarity and support, rather than punishment and austerity, can rebound as a model member state. As progressives, we also need to consciously set out to restore the wage share in national income to improve equity, social cohesions, personal income distribution, longer term wealth distribution, macroeconomic stability and the composition of aggregate demand.

Persuading Voters that the Post-War European Social Compact is Alive and Well

Economic and social progress in Europe since the war has been remarkable. Living standards and improvements in housing, health and peoples’ security have been excellent. There had been a consensus with conservatives that national income and wealth would be shared, but with the prolonged crisis, growing numbers of conservatives no longer want to share. The cake is no longer growing – thanks to their policies - and they want to keep more of it for themselves.

But the best way to grow national income is though social solidarity, education, investment, efficient public services and equitable incomes.

Re-building the European Social Model must be the priority of all progressive forces in Europe. Many Europeans fear that governments are neglecting citizens and are obsessed by appeasing the financial markets; have a very narrow view of “competitiveness”; and with fiscal rectitude. This means that the Post-War European Social Compact appears to be dying or dead for increasing numbers of European citizens.

Apparent confirmation of its death was given by the key unelected European leader, Mario Draghi, who was quoted in the Wall Street Journal earlier this year as saying that “Europe's vaunted social model is "already gone”." Thus a clarion call for all progressive parties must be that the European Social Model is very much alive. Not alone will it continue to be a core objective in progressives’ policy implementation in government, but we should guarantee that the Social Model will be enhanced in line with economic and social progress.

The prolonged ineptitude of European leaders, predominantly conservatives, in dealing with the crisis effectively has undermined public confidence in the European project. The failure of austerity measures has led the same leaders to pursue them with more vigour, instead of learning from their mistakes. The Fiscal Compact will exacerbate the problem.

Mr. Draghi also argued that “austerity, coupled with structural change, is the only option for economic renewal”. Like ancient Greek priests, appeasing the gods with sacrifices, he wants to feed even more of our living standards to the markets, saying "Backtracking on fiscal targets would elicit an immediate reaction by the market."

On top of this deep crisis, there are great challenges with ageing populations straining pensions, rising health costs, environmental issues and much more. There is a hollowing-out of the middle with the growth in “Cool Jobs and Crap Jobs” worldwide. Solid pensionable jobs like banking, computing, parts of accounting, engineering etc. are being de-skilled and outsourced from Europe. The polarisation of jobs is a vital area which has to be addressed.

Some of these challenges may mean doing things very differently, but all can be overcome. Revitalising the Social Model is the key to rebuilding confidence in Europe. One step in this direction is to have a clear understanding of one of the most abused concepts in modern economics- “competitiveness".

Competitiveness is Poorly Understood

The most abused word in modern political economy is “competitiveness.” It is not just that each economist has a different definition, but even the same economist may define it in several ways. For most of them and for many institutions it is simply a description of short-term movements in wages. A more sophisticated definition is of short run movements in unit labour costs, but both are too often ideological, using easily available data to beat up workers and trade unions. This is now a tired abuse of what can be a helpful concept in modern economics in measuring national economic progress. Unless we all subscribe to the same understanding, we must avoid this abused word/concept.

A good definition (as given in the 2003 European Comission Report on Competitiveness) is: “Competitiveness is understood to mean high and rising standards of living of a nation with the lowest possible level of involuntary unemployment on a sustainable basis.” But this does not inform on how to measure it.

I suggest the complexity of the issue is best understood by examining the work of Ireland’s tripartite National Competitiveness Council, which represents unions, employers and Government (albeit with only one-eighth union representation). It produces an annual Benchmarking or Scorecard report covering Ireland’s competitiveness performance in a comprehensive and coherent way. It has a collection of statistical indicators against a whole-of-economy comparison to 17 other economies and the OECD or EU average. Costs and labour costs are included but they are only a small part of the overall measurement of a country’s competitiveness. It is deeply disappointing that sophisticated analysts such as the OECD, IMF etc. still define competitiveness only in terms of unit labour costs. But perhaps it is deliberately ideological?

It is worth remembering that only 9% of EU GDP is exported (measuring the exports in value added, not gross, terms), which means EU countries are very largely competing with themselves. We do buy European, already! However, competitiveness is worth benchmarking, if done properly.

A View from a Troubled Western Island

It is essential to avoid the core/periphery break up in Europe. Ireland grew from one of the poorest of the poor in Europe to one of the richest in twenty years, thanks in no small part to its membership of the Union. It is facing enormous economic problems at present, but provided we get support in facing our staggering and perhaps insurmountable private banking debts, Ireland will recover and revert to become a net contributor to the Union’s funds.

Ireland‘s economic collapse in 2008 was not due to poor competitiveness, nor to public sector profligacy, but to gross irresponsibility by a small elite in the private sector, operating within what had become an ultra-liberal economic system. It was the private banking collapse, which the government foolishly under-wrote which brought Ireland down. Commissioner Rehn demanded, in Latin, “pacta sunt servanda” and in English that the Irish taxpayers “respect your commitments and obligations”. However, these debts are not ours, but those of the private defunct banks, which our sacked government guaranteed, in our name, without our consent.

Prior to this, European banks queued up to lend to our reckless banks, while the ECB looked on benignly. Tax policy – cutting direct taxes on incomes and profits, tax breaks especially for property investment and tax-shifting – also contributed substantially to Ireland’s current economic crisis. The third factor was de-regulation.

Today Irish taxpayers are repaying the bank creditors (EU banks and hedge funds) of the six Irish banks which were socialised. This is an impossible task for 1.8 million people at work, where GDP has collapsed by over 13 per cent between 2008 and 2011, GNP by over 16 per cent and domestic demand by a staggering 24.9 per cent and is still in decline. Unemployment is at 14.6 per cent. When discouraged workers, those who would like to work full time, are included the official figure rises to 25 per cent. Youth unemployment is soaring and long term unemployment is 60.3 of the total.

When the trade unions first met the ECB, EU, IMF Troika in late 2010 when Ireland was placed in Examinership, we pointed out that Ireland has many core strengths, but that the bailout package agreed by the Government with them made the economic recovery very difficult. We said that the deflationary impacts of the measures in the package are such that growth has little chance of reviving. This has been proven to be correct - unless one gives credence to the technical definition of “the end of recession” with a few recent quarters of very weak growth in GDP. It will take many years to makes up for the fall of 13 per cent at current rates, especially with citizens’ taxes diverted to fund the apparently endless private bank bailout.

The previous government tried an experiment in Internal Devaluation because there could be no devaluation in a single currency area. Fortunately, this strategy failed.

Had it worked, the recession would be even worse. It would have sucked more demand out of the economy. Overall, the average employee who remained in work saw no decline in real hourly earnings from the beginning of 2008 when the Crash began. For some workers, in the export and other dynamic sectors, there have been small wage rises. The real losses were the considerable numbers (a huge 14 per cent fall) who lost their jobs. A recent study of how employers dealt with the total wage bill found that there had been cuts, but “however, these cuts were primarily achieved though employment reductions with relatively low contributions at the aggregate level from changes in average hourly earnings and average weekly paid hours” (see Walsh, Kieran “Wage bill change during the recession: how have employers reacted to the downturn?” Statistical and Social Enquiry Society of Ireland, February, 2012)

This relative stability in real incomes of those who kept their jobs since the Crash of 2008 has also been extremely important in ensuing that the terrible collapse in domestic demand – of one quarter in less than four years – was not worse. This is because averagely paid workers generally spend most of their incomes. The last government also cut the minimum wage by 12 per cent but the new government reversed this immediately. It also did not cut welfare rates and there is a deal with the public service whereby there will be no further pay cuts (two of which averaged 14 per cent) provided there is support for substantial change, which is occurring.

The relative stability in real incomes, in welfare rates and in public employment is the key to the explanation of why there has been no rioting in Ireland, despite our travails. It is crucial that the core economies which are performing well, act in solidarity and not in punishment to the underperforming peripherals.

Nor should we entertain the idea of a ‘two speed’ Europe, which could allow an inner core to move towards closer economic and political union supposedly “to protect the Union as a whole.” To move in that direction is to abandon solidarity and to miss this opportunity to build a cohesive Europe.

Restoring the Wage Share of National Income

The share of national income going to wages has fallen considerably in most developed countries since the early 1970s. There has been a slight reversal in recent years, but it is forecast to fall back again. One explanation for the falling labour share and rising share to capital might be that there has been an intensification of capital investment. However, against that, there has been a huge improvement in human capital with all countries seeing major increases in educational and skills attainment. It seems that the investment in human capital is not being rewarded by increases in labour’s share of national income. As less national income is going to workers, this has a secular impact on aggregate demand and thus on growth.

The issue of the decline in labour income share involves equity, social cohesion and personal income distribution, longer-term wealth distribution, macroeconomic stability and the composition of aggregate demand.

The “American Dream” of the next generation enjoying a higher standard of living than their parents has been dead since the early 1970s. Since 1975 US workers’ median incomes have not risen. There are hard lessons to be learned from America. The stagnation in incomes was masked for some time because the working and middle classes borrowed against their homes. Now the home ownership dream has turned into a nightmare for many with negative equity and big debts. It was also masked by a dramatic fall in the prices of many goods now imported from Asia which reduced the cost of living. It was further masked by the growth in dual-income families, where there had only been one earner in the past. Male, unionised and in well paid manufacturing, these American workers had previously seen themselves as firmly in the “middle class”.

The fall in labour’s share of national income was also driven by globalisation, accelerated by technology, falling prices in transport and instant communications. In turn, these trends were accentuated by liberalisation of borders and markets, especially labour markets.

The value of the fall between 1973 and 2011 is substantial in monetary terms. Even with the smallest decline which as in France of 3.5%, it is still a transfer of €71bn from labour’s share of GDP to capital. For Germany it is €137bn.[Click to enlarge table below].

The decline of trade unions and the paucity of vision and lack of ambition in progressive parties, which should be counterforces to such trends, also facilitated the stagnation of incomes of the majority, in spite of economic growth and growth in labour productivity.

There is also a view that corporations and the rich should not have to pay “too much tax” as it is a disincentive to investment. Simultaneously, people are demanding more and better public services, but have been increasingly unwilling to pay for them through taxation. The aversion of many governments and major institutions like the IMF and OECD to progressive income taxes which they now pejoratively term “taxes on labour” means that if acted upon, taxation will fail to be a redistributive mechanism. It also means that the great polarisation of incomes will continue unchecked and citizens will grow even more angry and frustrated.

A Common Fiscal Policy is key to addressing inequality, sorting out the banks and boosting demand by underwriting an EU wide stimulus programme. It may begin with a small budget overall, but a small budget in EU terms is still a lot of cash. I would go for tax coordination rather than harmonisation where member states can set rates, within bands, though a common tax base for companies makes sense in a single market.

Conclusion

The real irony in Europe is that this deep crisis was caused by neo-liberal economic policies. Yet it is conservatives who are in power in most member states. They are prolonging the crisis with the same old failed policies and general incompetence. Some are even reverting to narrow nationalism. Instead, bold action with an EU-wide stimulus and policies informed by a longer term vision of European solidarity is required.

There is a lesson in this for us all. That is to replenish our vision by going back to core ideas, sticking to them in a principled way and being innovative in our policy responses.

Part of this post is based on a a presentation given to a meeting of progressive groups, parties and individuals in the French Parliament on Friday March 16th entitled "The Renaissance of Europe". It was sponsored by four EU think-tanks: FEPF, Jean Jaures, Friedrich Ebert Stiftung and Italianieuropei. This event will be followed by seminars in Rome and Berlin in advance of the Italian and German elections.

Tuesday, 20 March 2012

Ireland's funding options: Time to end the 'race-to-disaster' debate

Tom McDonnell & Michael Taft: Even before the wording has been published and a referendum date named there is one issue that looks set to dominate the debate over the Fiscal Treaty; namely, what future financing options does Ireland have in the eventuality of a ‘No’ vote. While we are not taking a position on the substantive issue in this post, the following is intended to aid the debate by helping to answer that question.

The ‘Indispensable’ Condition

First, regardless of the Treaty vote, Ireland is guaranteed funding under the current programme – as long as it meets its targets. A Yes or No vote will not change this.

In the event of a No vote with Ireland unable to fully return to the markets, what would the situation be?

‘ . . . the granting of assistance in the framework of new programmes under the European Stability Mechanism will be conditional, as of 1 March 2013, on the ratification of this Treaty by the Contracting Party.’

This clearly states that new financing under the European Stability Mechanism is contingent upon ratification of the Treaty. However, we would put the following points that suggest that the issue contains potentially significant ambiguity.

First, the text of the European Stability Mechanism Treaty states that there are two conditions for providing support for ESM members:

‘The purpose of the ESM shall be to mobilise funding and provide stability support under strict conditionality, appropriate to the financial assistance instrument chosen, to the benefit of ESM Members which are experiencing, or are threatened by, severe financing problems, if indispensable to safeguard the financial stability of the euro area as a whole and of its Member States.’

The two conditions for support under the ESM appear to be (a) a member-state requires assistance, and (b) such assistance is ‘indispensable’ to the stability of Euro area. The indispensable clause, not surprisingly, is stated four times in the ESM treaty; unsurprising as this is the purpose of the ESM – to safeguard the Eurozone’s stability.

For argument’s sake, let’s assume Ireland – a member of the ESM but having voted No in the referendum – is in demonstrable need of financial assistance; and further, it can be objectively established that, without such assistance, there is a threat to Eurozone stability (issues of both state and bank default which may arise if assistance isn’t forthcoming). A literalist reading of the Fiscal Treaty would seem to settle the issue – Ireland, if voting No, would be excluded from the fund. But how final is this literalism?

‘Indispensable’ to the financial stability of the Euro area does not become less indispensable merely because Ireland, an ESM member, has not incorporated rules (rules that it has already agreed to) into its constitution through a process unique in the Eurozone – that is, a popular referendum. It is difficult to imagine a situation where the financial stability of the Eurozone (and Eurozone countries from Spain to Germany) is at risk and the resolution of that risk is barred because of a referendum result in a member-state. This would effectively undermine the intent of the ESM and its ability to respond to financial risks in the Eurozone.

What this crisis has shown is the flexibility of the Eurozone and EU institutions to respond to the crisis, whether we agree with the policies or not. For instance, the European Central Bank is legally barred from acting as a lender of last resort to sovereign states. But that did not stop it from, first, participating in the secondary bond markets and, second, from providing over €1 trillion in liquidity to European banks through their Long-Term Refinancing Operations (LTROs). The LTRO was intended to indirectly ease pressure on Spanish and Italian bond yields and was effectively a roundabout method of overcoming the bar to lend to sovereign states. Both of these were innovative and flexible responses. This resort to flexibility has implications for Ireland in the event of a No vote.

The Fiscal Compact refers to ‘new programmes under the European Stability Mechanism’. The ‘new’ may provide some flexibility, especially if Ireland is unable to re-enter the market and seeks a continuation of the current programme. This could be buttressed by the statement by the EU Heads of State or Government in July of last year. This, too, is definitive:

‘We are determined to continue to provide support to countries under programmes until they have regained market access, provided they successfully implement those programmes.’

Minister Michael Noonan confirmed this after the summit:

'There is a commitment that if countries continue to fulfil the conditions of their programme the European authorities will continue to supply them with money even when the programme is concluded . . . The commitment is now written in that if we are not back in the markets the European authorities will give us money until we get back in the markets.’

That both the EU leaders commitment and the Minister’s statement followed on from agreement to establish the ESM – with the same clause that disbursement of funds is based on the same ‘indispensability’ condition referred to above – suggests that there is considerable room for all sides to manoeuvre, even in the eventuality of a No vote. We are not suggesting that this is a definitive outcome. However, resort to a literal reading could lead us to the conclusion that Ireland, even if voted Yes, could be denied funding under the ESM if it was concluded at EU level that assistance was not indispensable to Eurozone stability. We seriously doubt this scenario which is why literal readings of one section of one treaty can lead us to unjustified conclusions. This holds when discussing the outcomes of either a Yes or No vote.

Alternative Sources of Funding

Regardless of the above, there is a credible argument that Ireland, in the eventuality that it needs a second bailout, has access to funding sources apart from the ESM; namely the IMF. This is the same ‘insurance’ or ‘back-stop’ that all EU countries are entitled to as members of the IMF. More EU countries have accessed IMF support than EU support in the last decade: Latvia, Lithuania, Poland, Bulgaria, Romania, Hungary, and Estonia.

The IMF programmes have recently undergone considerable reform in order to tailor support for the specific need of a country. Further support from the IMF does not necessarily have to come via the Extended Facility that Ireland currently participates in. Some of these programmes may even be more suitable to the Irish economy than an ESM programme modelled on the current one. This is because IMF programmes can provide credit lines on a precautionary basis. In these circumstances, Ireland may be able to enter the market even on a partial basis but have recourse to the IMF if and when further support is needed. A particular strength of some of these programmes is that Ireland may not have to draw down any funds (though it would make a ‘down-payment’ to participate in the particular programme).

There is a range of programmes that Ireland may be able to avail of:

Stand-by Arrangements with high-access precautionary provisions. The IMF describes this as its ‘workhorse lending instrument’.

The Flexible Credit Scheme which does not carry with it any conditions (and which the IMF claims ‘reduces the perceived stigma of borrowing from the IMF’.

The Precautionary and Liquidity Line is another line of support which provides finance and, according to the IMF, ‘is intended to serve as insurance and help resolve crises’.

Rapid Financing Instrument provides a quick response to an outside shock – including economic shocks.

These programmes are separate from the current Extended Facility programme we are in. Some have conditions attached to them; one does not (the Flexible Credit Scheme). They have a range of participating and payback periods, with provision for roll-over. We are not suggesting that Ireland would comply with all of the above; however, it shows the considerable potential sources of funding. There are two issues that might arise in considering these alternatives.

First, will Ireland be eligible for future financing? IMF financing is based on quotas assigned to each country with programmes laying down specific amounts that can be lent. However, all the programmes have exceptional access policy whereby limits are waived – with the exception of the Flexible Credit Line which, in any event, has no cap on funding.

In fact, for many countries there is a natural progression from the type of IMF funding Ireland is currently in (an Extended programme) to the programmes listed above. Poland is an example which started out in an Extended Programme, progressed to a Standby Arrangement and is now in a Flexible Credit Line which has no conditions attached. Ireland could make a similar progression.

Second, it has been suggested that the IMF actually regards Ireland as a high-risk country and may, therefore, refuse to lend further. In the first instance this would certainly be curious. To date, Ireland has abided by the programme that the IMF itself helped design (it’s fairly typical of IMF extended facilities). If the IMF suddenly claimed Ireland was too risky, this would be tantamount to an admission of their own failure. Would Ireland be penalised by the IMF for adhering to a programme that the IMF helped designed?

There is a strong argument that Ireland fulfils all four criteria for an ‘exceptional access’:

(a) The member is experiencing or has the potential to experience pressures resulting in a need for Fund financing that cannot be met within the normal limits.

(b) There is a high probability that the member’s public debt is sustainable in the medium term. However, in instances where there are significant uncertainties that make it difficult to state categorically that there is a high probability that the debt is sustainable over this period, exceptional access would be justified if there is a high risk of international systemic spillovers.

(c) The member has prospects of gaining or regaining access to private capital markets within the timeframe when Fund resources are outstanding.

(d) The policy program of the member provides a reasonably strong prospect of success, including not only the member’s adjustment plans but also its institutional and political capacity to deliver that adjustment.

We would draw attention to the condition in (b); in particular where exceptional access is justified if there is a high risk of international ‘spillovers’. There is a strong argument that Ireland is in such a situation. That the IMF participated in the current bail-out, despite the staff country report in December 2010 stating that Ireland would entail ‘substantial risks’, only confirms their determination to participate in programmes where the risks of spillovers are significant.

Another issue is the scale to which Ireland has already borrowed from the IMF. Currently, Ireland is the third largest debtor to the IMF – behind Greece and Portugal. Poland has a similar level of contingent debt, while Mexico is much higher – though these countries are in the Flexible Credit Line have not drawn down funds. There is a limit to which a country can borrow – even if complying with the provisions of the exceptional access. The IMF has lent a considerable amount to EU countries already and while it still retains considerable reserves, and while further precautionary lending to EU countries would not impact unduly, the possibility of larger countries needing assistance (Spain, Italy) could squeeze available funds to Ireland.

Taking all of the above on board, that the IMF has decided to extend its assistance to Greece in the form of a second bail-out suggests that Ireland would be a credible candidate for further support if it cannot access the international markets. If so, this could be a viable alternative to ESM funding.

Appalling Scenarios and a Legitimate Debate

None of the above can be certain. But that is no reason to resort to counter-posing ‘appalling scenarios’. Some argue that Ireland will be frozen out of both market and institutional funding if we vote No. Clearly, this would be an appalling scenario. Others argue that it would never come to this because of the impact on the Eurozone (defaults, contagion) – another appalling scenario.

This is not a satisfactory way to debate this issue. This will trap us in a ‘race-to-disaster’ debate which will be particularly uninformative. We have attempted to outline concrete scenarios for Ireland apart from the ESM. Whether these would become available is a subject for legitimate debate. The fact that Ireland may have a secure safety net with IMF funding is likely to induce cooperative, if ad hoc, relationships with the EU. Competing disaster scenarios will only undermine our understanding of these difficult issues.

In one respect, debating non-market funding has an air of unreality about it – if we are to heed the Government’s dismissal of a second bail-out as ‘ludicrous’. The fact that this issue is being taken seriously is a testament to the common sense of the debate. While we respect the fact that no Government will intentionally play down the prospect of being able to borrow on the international markets, in our own opinion a second bail-out is a real and probable outcome of current policies.

And this is not in the best interests of the Irish economy, whether that support comes from the IMF, the EU’s ESM , some other ad hoc EU support or any combination of these.

The ‘Indispensable’ Condition

First, regardless of the Treaty vote, Ireland is guaranteed funding under the current programme – as long as it meets its targets. A Yes or No vote will not change this.

In the event of a No vote with Ireland unable to fully return to the markets, what would the situation be?

‘ . . . the granting of assistance in the framework of new programmes under the European Stability Mechanism will be conditional, as of 1 March 2013, on the ratification of this Treaty by the Contracting Party.’

This clearly states that new financing under the European Stability Mechanism is contingent upon ratification of the Treaty. However, we would put the following points that suggest that the issue contains potentially significant ambiguity.

First, the text of the European Stability Mechanism Treaty states that there are two conditions for providing support for ESM members:

‘The purpose of the ESM shall be to mobilise funding and provide stability support under strict conditionality, appropriate to the financial assistance instrument chosen, to the benefit of ESM Members which are experiencing, or are threatened by, severe financing problems, if indispensable to safeguard the financial stability of the euro area as a whole and of its Member States.’

The two conditions for support under the ESM appear to be (a) a member-state requires assistance, and (b) such assistance is ‘indispensable’ to the stability of Euro area. The indispensable clause, not surprisingly, is stated four times in the ESM treaty; unsurprising as this is the purpose of the ESM – to safeguard the Eurozone’s stability.

For argument’s sake, let’s assume Ireland – a member of the ESM but having voted No in the referendum – is in demonstrable need of financial assistance; and further, it can be objectively established that, without such assistance, there is a threat to Eurozone stability (issues of both state and bank default which may arise if assistance isn’t forthcoming). A literalist reading of the Fiscal Treaty would seem to settle the issue – Ireland, if voting No, would be excluded from the fund. But how final is this literalism?

‘Indispensable’ to the financial stability of the Euro area does not become less indispensable merely because Ireland, an ESM member, has not incorporated rules (rules that it has already agreed to) into its constitution through a process unique in the Eurozone – that is, a popular referendum. It is difficult to imagine a situation where the financial stability of the Eurozone (and Eurozone countries from Spain to Germany) is at risk and the resolution of that risk is barred because of a referendum result in a member-state. This would effectively undermine the intent of the ESM and its ability to respond to financial risks in the Eurozone.

What this crisis has shown is the flexibility of the Eurozone and EU institutions to respond to the crisis, whether we agree with the policies or not. For instance, the European Central Bank is legally barred from acting as a lender of last resort to sovereign states. But that did not stop it from, first, participating in the secondary bond markets and, second, from providing over €1 trillion in liquidity to European banks through their Long-Term Refinancing Operations (LTROs). The LTRO was intended to indirectly ease pressure on Spanish and Italian bond yields and was effectively a roundabout method of overcoming the bar to lend to sovereign states. Both of these were innovative and flexible responses. This resort to flexibility has implications for Ireland in the event of a No vote.

The Fiscal Compact refers to ‘new programmes under the European Stability Mechanism’. The ‘new’ may provide some flexibility, especially if Ireland is unable to re-enter the market and seeks a continuation of the current programme. This could be buttressed by the statement by the EU Heads of State or Government in July of last year. This, too, is definitive:

‘We are determined to continue to provide support to countries under programmes until they have regained market access, provided they successfully implement those programmes.’

Minister Michael Noonan confirmed this after the summit:

'There is a commitment that if countries continue to fulfil the conditions of their programme the European authorities will continue to supply them with money even when the programme is concluded . . . The commitment is now written in that if we are not back in the markets the European authorities will give us money until we get back in the markets.’

That both the EU leaders commitment and the Minister’s statement followed on from agreement to establish the ESM – with the same clause that disbursement of funds is based on the same ‘indispensability’ condition referred to above – suggests that there is considerable room for all sides to manoeuvre, even in the eventuality of a No vote. We are not suggesting that this is a definitive outcome. However, resort to a literal reading could lead us to the conclusion that Ireland, even if voted Yes, could be denied funding under the ESM if it was concluded at EU level that assistance was not indispensable to Eurozone stability. We seriously doubt this scenario which is why literal readings of one section of one treaty can lead us to unjustified conclusions. This holds when discussing the outcomes of either a Yes or No vote.

Alternative Sources of Funding

Regardless of the above, there is a credible argument that Ireland, in the eventuality that it needs a second bailout, has access to funding sources apart from the ESM; namely the IMF. This is the same ‘insurance’ or ‘back-stop’ that all EU countries are entitled to as members of the IMF. More EU countries have accessed IMF support than EU support in the last decade: Latvia, Lithuania, Poland, Bulgaria, Romania, Hungary, and Estonia.

The IMF programmes have recently undergone considerable reform in order to tailor support for the specific need of a country. Further support from the IMF does not necessarily have to come via the Extended Facility that Ireland currently participates in. Some of these programmes may even be more suitable to the Irish economy than an ESM programme modelled on the current one. This is because IMF programmes can provide credit lines on a precautionary basis. In these circumstances, Ireland may be able to enter the market even on a partial basis but have recourse to the IMF if and when further support is needed. A particular strength of some of these programmes is that Ireland may not have to draw down any funds (though it would make a ‘down-payment’ to participate in the particular programme).

There is a range of programmes that Ireland may be able to avail of:

Stand-by Arrangements with high-access precautionary provisions. The IMF describes this as its ‘workhorse lending instrument’.

The Flexible Credit Scheme which does not carry with it any conditions (and which the IMF claims ‘reduces the perceived stigma of borrowing from the IMF’.

The Precautionary and Liquidity Line is another line of support which provides finance and, according to the IMF, ‘is intended to serve as insurance and help resolve crises’.

Rapid Financing Instrument provides a quick response to an outside shock – including economic shocks.

These programmes are separate from the current Extended Facility programme we are in. Some have conditions attached to them; one does not (the Flexible Credit Scheme). They have a range of participating and payback periods, with provision for roll-over. We are not suggesting that Ireland would comply with all of the above; however, it shows the considerable potential sources of funding. There are two issues that might arise in considering these alternatives.

First, will Ireland be eligible for future financing? IMF financing is based on quotas assigned to each country with programmes laying down specific amounts that can be lent. However, all the programmes have exceptional access policy whereby limits are waived – with the exception of the Flexible Credit Line which, in any event, has no cap on funding.

In fact, for many countries there is a natural progression from the type of IMF funding Ireland is currently in (an Extended programme) to the programmes listed above. Poland is an example which started out in an Extended Programme, progressed to a Standby Arrangement and is now in a Flexible Credit Line which has no conditions attached. Ireland could make a similar progression.

Second, it has been suggested that the IMF actually regards Ireland as a high-risk country and may, therefore, refuse to lend further. In the first instance this would certainly be curious. To date, Ireland has abided by the programme that the IMF itself helped design (it’s fairly typical of IMF extended facilities). If the IMF suddenly claimed Ireland was too risky, this would be tantamount to an admission of their own failure. Would Ireland be penalised by the IMF for adhering to a programme that the IMF helped designed?

There is a strong argument that Ireland fulfils all four criteria for an ‘exceptional access’:

(a) The member is experiencing or has the potential to experience pressures resulting in a need for Fund financing that cannot be met within the normal limits.

(b) There is a high probability that the member’s public debt is sustainable in the medium term. However, in instances where there are significant uncertainties that make it difficult to state categorically that there is a high probability that the debt is sustainable over this period, exceptional access would be justified if there is a high risk of international systemic spillovers.

(c) The member has prospects of gaining or regaining access to private capital markets within the timeframe when Fund resources are outstanding.

(d) The policy program of the member provides a reasonably strong prospect of success, including not only the member’s adjustment plans but also its institutional and political capacity to deliver that adjustment.

We would draw attention to the condition in (b); in particular where exceptional access is justified if there is a high risk of international ‘spillovers’. There is a strong argument that Ireland is in such a situation. That the IMF participated in the current bail-out, despite the staff country report in December 2010 stating that Ireland would entail ‘substantial risks’, only confirms their determination to participate in programmes where the risks of spillovers are significant.

Another issue is the scale to which Ireland has already borrowed from the IMF. Currently, Ireland is the third largest debtor to the IMF – behind Greece and Portugal. Poland has a similar level of contingent debt, while Mexico is much higher – though these countries are in the Flexible Credit Line have not drawn down funds. There is a limit to which a country can borrow – even if complying with the provisions of the exceptional access. The IMF has lent a considerable amount to EU countries already and while it still retains considerable reserves, and while further precautionary lending to EU countries would not impact unduly, the possibility of larger countries needing assistance (Spain, Italy) could squeeze available funds to Ireland.

Taking all of the above on board, that the IMF has decided to extend its assistance to Greece in the form of a second bail-out suggests that Ireland would be a credible candidate for further support if it cannot access the international markets. If so, this could be a viable alternative to ESM funding.

Appalling Scenarios and a Legitimate Debate

None of the above can be certain. But that is no reason to resort to counter-posing ‘appalling scenarios’. Some argue that Ireland will be frozen out of both market and institutional funding if we vote No. Clearly, this would be an appalling scenario. Others argue that it would never come to this because of the impact on the Eurozone (defaults, contagion) – another appalling scenario.

This is not a satisfactory way to debate this issue. This will trap us in a ‘race-to-disaster’ debate which will be particularly uninformative. We have attempted to outline concrete scenarios for Ireland apart from the ESM. Whether these would become available is a subject for legitimate debate. The fact that Ireland may have a secure safety net with IMF funding is likely to induce cooperative, if ad hoc, relationships with the EU. Competing disaster scenarios will only undermine our understanding of these difficult issues.

In one respect, debating non-market funding has an air of unreality about it – if we are to heed the Government’s dismissal of a second bail-out as ‘ludicrous’. The fact that this issue is being taken seriously is a testament to the common sense of the debate. While we respect the fact that no Government will intentionally play down the prospect of being able to borrow on the international markets, in our own opinion a second bail-out is a real and probable outcome of current policies.

And this is not in the best interests of the Irish economy, whether that support comes from the IMF, the EU’s ESM , some other ad hoc EU support or any combination of these.

Nama Wine Lake on the Promissory Notes

Tom McDonnell: Here is a timely recap by Nama Wine Lake of the grotesque farce that is the Anglo promissory note debacle.

Saturday, 17 March 2012

Emigration a 'lifestyle choice'?

Tom Healy: Today's 'feel good' story in the Irish Times ran as 'Emigrants leaving by choice'. Nice to know that some people still have choices. Politicians seem to believe there is much less choice than before. How much migration is really taking place and who is emigrating - and even still immigrating to the State? There is much less hard data on this than many assume. The CSO estimate an annual gross outward migration of 76,000 in the year ending 2011 - many are young and single. 50% of respondents to the Ipsos MRBI poll reported in today's IT felt it was their 'choice' to emigrate when asked 'Did you feel forced to emigrate or was it your choice'. 42% said the left Ireland for 'a change of experience'. Writer Stephen Collins says: 'The findings appear to back the contention of Minister for Finance Michael Noonan that emigration is a lifestyle choice for many who have left the country in recent times'. While one does not wish to take from yet another feel good story building on all the other good news recently a few questions are in order -

all of this not to question necessarily the reliability of the results. Just caution is needed. Have a great St Patricks weekend commemorating an immigrant who was forced here in the first place - well he chose to come back a second time.

how is it that gross outward migration - most of which is 'by choice' was estimated to be running at 76K per annum in 2011 and 36K per annum in 2006?

If 59% of migrants left by 'choice' what about the other 59%? (a serious statistical question in any opinion survey?)

would it be possible to actually report the questionnaire and precise questions?

it should not be thought that because most emigrants were in employment prior to emigrating that the nature, hours and reliability of employment was anything but inadequate.

how was the sample of 300 persons chosen - the detail given is scanty and one wonders about possible bias.

all of this not to question necessarily the reliability of the results. Just caution is needed. Have a great St Patricks weekend commemorating an immigrant who was forced here in the first place - well he chose to come back a second time.

Friday, 16 March 2012

The Alcohol Industry - A case study of health versus wealth

Nat O'Connor: The recently completed (Feb 2012) Steering Group Report On a National Substance Misuse Strategy has taken a public health approach to the issue of alcohol, and it estimates the costs to Irish society of dealing with alcohol abuse to be €3.7 billion. At the same time, the alcohol manufacturing and retail industry provided €2 billion in VAT and excise to the State, as well as 50,000-60,000 direct and indirect jobs.

There’s just no way to reduce the €3.7 billion of social harm and retain the same levels of tax and jobs. One of the recommended societal goals is to reduce alcohol consumption by nearly a quarter (page 7), which would have to significantly affect the alcohol industry.

It's a good case study of a genuine dilemma facing the Government about how to curb the societal harm and economic costs from alcohol abuse while minimising the loss of jobs or tax revenue from the alcohol industry.

Minority reports from both the ABFI and MEAS disagree with the steering groups findings. This suggests that the alcohol industry sees the report's recommendations overall as a financial threat, although it would be unfair to infer from this that the industry is unwilling to deal with the issue of abuse.

Table 7 (page 78) gives the breakdown of the €3.7 billion cost to society:

• €1.2 billion (32%) Costs to healthcare system of alcohol-related illnesses

• €1.2 billion (32%) Alcohol-related crime

• €526 million (14%) Alcohol-related road accidents

• €330 million (9%) Output lost to alcohol-related absence from work

• €197 million (5%) Alcohol-related accidents at work

• €167 million (5%) Alcohol-related suicides

• €110 million (3%) Alcohol-related premature mortality

The economic role of alcohol production and consumption is addressed too (page 71):

• €7.2 billion personal expenditure on beverages

• €2.9 billion turnover in drinks manufacturing, including €1 billion in drinks exports

• The on-trade provides 43,629 full-time job equivalents, and off-licences another 2,850.