‘Growth affects both the denominator and the numerator of the structural deficit as a share of GDP. (For simplicity I assume that actual and potential GDP grow at equal rates post 2015.) The denominator effect is straightforward. For the numerator, we could use the standard coefficient used by the European Commission for Ireland that assumes that the reduction in the deficit is 0.4 times the change in nominal GDP. (This coefficient is usually used for doing cyclical adjustments, but it should also be applicable for measuring the impact of changes in nominal potential GDP on structural balance in the absence of discretionary adjustments to tax and expenditure parameters.)’

On this basis John does some calculations – using a more conservative co-efficient of 0.2. He finds the structural deficit is effectively wiped out by 2019 / 2020 without any additional austerity because growth has done all the heavy lifting.

I would suggest that this line of argument is flawed. First, I assume the co-efficient he uses refers to the cyclical sensitivity measurement of 0.4. This measurement is used to deconstruct the deficit into its ‘cyclical’ and ‘structural’ components. Essentially, you measure the gap between the real GDP and potential GDP growth and then apply the 0.4 to see how much of the gap is cyclical.

And herein lies the first problem – the 0.4 is an instrument to define the cyclical component of the output gap. It is not a measurement which defines the relationship between nominal growth rates and deficit reduction – whether it is the general or structural deficit. It is analogous to using a car clamp to change a light bulb. It is the wrong instrument. As the Department of Finance puts it:

‘Indeed, by definition, reducing the structural element of the deficit will require policy action. . . .‘

The whole point of structural deficit measurements is to determine what the deficit will be when the economy returns to full capacity. If the economy is firing on all cylinders and there is still a deficit, then the Government must take policy action to correct this, because growth cannot.

In doing his calculations, John assumes that real and potential GDP grow at the same rate. Never mind that the Government estimates that real GDP is growing at twice the rate of potential GDP in 2015 (yes, I know, this suggest that the economy is ‘over-heating’ – one of the absurdities with the model that the Department of Finance is using). If the output gap is zero, there is no role for applying the 0.4 co-efficient because there is no cyclical component to measure.

Seamus Coffey does his own calculations based on John’s more conservative co-efficient of 0.2 and applies it to GDP growth (though Seamus does say ‘There is no way of knowing what this’ co-efficient is). He comes up with a similar result to John.

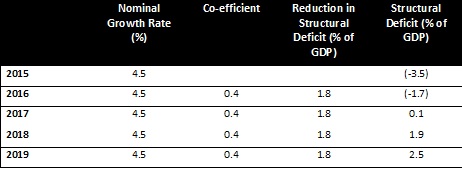

But there is a problem here. Why use a conservative 0.2 co-efficient? If you believe that 0.4 tells the story, go with it. And why, use a nominal growth rate of 3.5 percent? The Government claims that in 2015 the nominal growth rate is 4.5 percent. So let’s go with that.

What do we get? We find that the structural deficit turns into a structural surplus without doing anything.

And what a surplus! By 2019 we will have a structural surplus of 2.5 percent. We outdo even the Germans. We get to go to the top of the class.

Is this likely? No. But we don’t have to argue the toss about cyclical sensitivity measurements or coefficients of elasticity. We merely have to go to the IMF’s own projection – which helps because (a) they stretch out to 2017 and (b) they assume, like John, no fiscal adjustment after 2015. What do they find?

In percentage terms, the reduction in the structural deficit is minimal: less than 0.1 percent of GDP each year.

But why should this surprise us? If there is deficit left over after the output gap is closed (after the economy returns to full capacity), what remains is the structural deficit which requires ‘policy action’ to reduce.

Political Implications

But there’s more to all this than duelling statistics. The Government and their austerity supporters have co-opted the language of progressives to avoid answering a fundamental question: what the cost of the Fiscal Treaty will be in terms of future austerity measures. They are now talking about ‘growth’ being the main instrument of deficit-reduction. The Government has even gone so far as to say that investment will grow the productive capacity and, therefore, reduce the deficit. Some of us have been saying that since the start of the crisis – UNITE and the trade union movement, TASC, contributors on Progressive-Economy; all we got was ridicule and scorn.

Here’s how the Department of Finance puts it:

‘Indeed, by definition, reducing the structural element of the deficit will require policy action, though not necessarily taxation and expenditure adjustments. Other options are available . . . . Such measures include labour market reforms - some of which are already in train - together with investment in technology and infrastructure to boost the productive capacity of the economy. To this end, the Government has established NewERA and the Strategic Investment Fund . . .

This ambitious programme of microeconomic reforms, by boosting the productive capacity of the economy, is expected to help reduce the structural element of the deficit by the middle part of the decade. For example, reforms along the lines of those set out in the Action Plan for Jobs 2012 and the Pathways to Work initiative, aimed at addressing some of the skills mis-match in the labour market, should help lower the unemployment rate. This would have a structurally beneficial impact on the public finances, on both the revenue and expenditure sides. In other words, the structural fiscal position is set to improve with these microeconomic reforms.’

And, yet, yet – the Government still refuses to provide a projection for this. If they are convinced that investment and labour market reforms will boost our productivity, they can project this – through the ‘potential GDP’ which measures the contribution of labour, capital and productivity.

This is all a charade. At the same time as the Government is assuring us that growing our potential GDP will reduce the structural deficit, they are actually revising downwards potential GDP.

In the last budget, the Government projected that our productive capacity would grow by 3.4 percent between 2010 and 2015. Only a few months later, the Government is now projecting growth at 2.4 percent. This revision downwards reflects their lower GDP projections.

In other words, we are going forward by going backwards.

This is the ultimate game plan. Stonewall any questions about the cost of the Fiscal Treaty with talk of growing our productive capacity even as you revise downwards our productive capacity. ‘Prove’ that growth will reduce the structural deficit by using variables that have little reference to structural deficit reduction. But don’t ‘prove’ it too much because it will look nonsensical. Ignore what current projections (IMF) have to say about all this. Even ignore the definition of a structural deficit. Above all, abandon your austerity clothes and don the robes of an expansionary programme – even as you promise to cut public investment next year and cut spending on public services and social protection by even more than you did this year.

Do all this. But don’t call it austerity.

7 comments:

This post is just 'disingenuousness-squared' - and an implicit argument for unsustainable and economically damaging 'raid, tax and spend' policies.

Economic growth is generated by increased productive, allocative and dynamic efficienies - and the removal of existing inefficiencies and deadweight costs. This has to be accompanied by deep-seated institutional reforms because the economy is seriously unbalanced - as are most other EU economies each in their own idiosyncratic ways (but with Ireland probably more than most). Both mainstream economists and those with a left-wing bias have nothing useful to say on this. The former are constrained by thier narrow, neoclassical microeconomic mindset; the latter - and this is particularly the case in Ireland - are quite happy with the existing instituional arrangements (though they would like to have more political power) and will strenuously defend them as they provide the means to minimise public spending reductions, to obstruct badly needed structural reforms and to provide a basis for stupid 'raid, tax and spend' policies.

You quote the DoF on structural reform:

"Other options are available . . . . Such measures include labour market reforms - some of which are already in train - together with investment in technology and infrastructure to boost the productive capacity of the economy. To this end, the Government has established NewERA and the Strategic Investment Fund . . ."

But this is precisely the problem. The Troika desired a through-going programme of structural refrom to counteract the inevitable detrimental impact of the necessary fiscal adjustment. But these 'reforms' are so innocuous and ineffective as to be almost irrelevant - and are of use only as a political optical illusion. The use of kid gloves to tackle monopoly profit-gouging and inefficiences in the private sheltered sectors is despicable, but the principal reason why key elements of these 'reforms' are irrevelant is the concerted, behind-the-scenes - and almost totally successful - opposition of managements and staff in the public and semi-state sectors.

The main reason the various agencies - both national and international - are continuously downgrading growth projections for the domestic economy is that the sheltered sectors (private, public and semi-state) have been successful in whittling these structural reforms down to almost nothingness.

It's surely past time for a bit of honesty and less of this hypocrisy and disingenuousness.

Paul Hunt relies on the usual canard that the public sector is the demon that is preventing economic growth but, provides no concrete evidence to back up his claims. There would be no modern economy in Ireland without public sector investment. Our basic infrastructure, roads, railways, electricity generation,telephones, television, hospitals, schools, public housing, wouldn’t exist today without it. Private capital contributed nothing to all this. State investment in Agriculture with research institutes, colleges, disease eradication, breeding improvements, mechanisation, made the industry what it is today.

The same has occurred in other countries. The citadel of Capitalism, the USA, also developed with massive public subsidies. State-funded investments in the internet, by the US National Science Foundation (NSF) grant funded the discovery by Google of its own algorithm. Would there be any iPad without the state-funded innovations in computer development ,communication technologies, GPS and touch-screen display? Where would GSK and Pfizer be without the $600bn the US National Institutes of Health put into research that has led to 75% of the most innovative new drugs in the last decade?The gigantic US aircraft and military sector receives billions of public money in overpriced contracts every year while housing, education and health are starved of funding.

What the state did was to take on the greatest risk, before the private sector dared to enter, acting as an “entrepreneurial” state. In biotech, venture capital entered 15 years after the state invested in the biotech knowledge base. In nanotech, scientists in the NSF coined the term before anyone in private business understood its potential returns.

Paul Hunt relies on slander of the whole idea of state investment and is in denial of the brazen delinquency of the globalised financial sector which is the real culprit behind the massive debt crisis we are currently mired in. De-regulated casino banks and finance speculation funders, set up in a privileged position, were allowed to create massive amounts of debt not based on production values of any kind and help themselves to billions of dollars of bonuses and returns which they turned into cash for themselves and their cronies. These corporate thieves now have turned over their fake debt iou’s for the ordinary public to pay for with wage cuts and destruction of public services and a further agenda to monopolise the entire public sphere for even more profit for themselves.

We, the public, should no longer tolerate the dictatorship of this ruinous elite. Our money and our labour should not be used to “fix” a thoroughly rotten system but instead should contribute to its long overdue demise and abolition.

Michael

this is very useful, and you have highlighted the logical contortions required to fit these ideas.

We are told that the new Treaty will have no effect that requires further cuts. We are also told that the current cuts- and more- are necessary because of the structural deficit (SD). Therefore the structural deficit will disappear by some other, magic formula. Growth is the answer, even though a SD is a measure of the deficit that specifically excludes the effects of growth.

If it weren't so serious, it would be laughable.

In fact, the DoF estimate of the sensitivity of government finances to changes in GDP is 0.6, as shown previously

http://www.progressive-economy.ie/2011/11/mtfs-iii-sensitivity-of-government.html

That being the case, even with the lower growth profile of 3.5% per annum the SD would be in surplus by 3.9% of GDP in 2019. Under the higher growth path of 4.5%, the SD would be a whopping 6.9% of GDP by that time.

No wonder the the sensitivity is cut by two-thirds. Only in this way can the logically impossible assertions noted above be made to 'fit'.

Paul Hunt relies on the usual canard that the public sector is the demon that is preventing economic growth but, provides no concrete evidence to back up his claims. There would be no modern economy in Ireland without public sector investment. Our basic infrastructure, roads, railways, electricity generation,telephones, television, hospitals, schools, public housing, wouldn’t exist today without it. Private capital contributed nothing to all this. State investment in Agriculture with research institutes, colleges, disease eradication, breeding improvements, mechanisation, made the industry what it is today.

The same has occurred in other countries. The citadel of Capitalism, the USA, also developed with massive public subsidies. State-funded investments in the internet, by the US National Science Foundation (NSF) grant funded the discovery by Google of its own algorithm. Would there be any iPad without the state-funded innovations in computer development ,communication technologies, GPS and touch-screen display? Where would GSK and Pfizer be without the $600bn the US National Institutes of Health put into research that has led to 75% of the most innovative new drugs in the last decade?The gigantic US aircraft and military sector receives billions of public money in overpriced contracts every year while housing, education and health are starved of funding.

What the state did was to take on the greatest risk, before the private sector dared to enter, acting as an “entrepreneurial” state. In biotech, venture capital entered 15 years after the state invested in the biotech knowledge base. In nanotech, scientists in the NSF coined the term before anyone in private business understood its potential returns.

Paul Hunt relies on slander of the whole idea of state investment and is in denial of the brazen delinquency of the globalised financial sector which is the real culprit behind the massive debt crisis we are currently mired in. De-regulated casino banks and finance speculation funders, set up in a privileged position, were allowed to create massive amounts of debt not based on production values of any kind and help themselves to billions of dollars of bonuses and returns which they turned into cash for themselves and their cronies. These corporate thieves now have turned over their fake debt iou’s for the ordinary public to pay for with wage cuts and destruction of public services and a further agenda to monopolise the entire public sphere for even more profit for themselves.

We, the public, should no longer tolerate the dictatorship of this ruinous elite. Our money and our labour should not be used to “fix” a thoroughly rotten system but instead should contribute to its long overdue demise and abolition.

FearFeasaMacLéinn,

You may adress me directly if you wish. Or perhaps you lack the bottle to address your ad hominem attack directly?

My issue is with the structure, organisation and management of the public sector - and with the pay levels needed to allow workers to meet the inflated cost base of the sheltered sectors. It is with the structure and financing of the infrastructure and utility sectors. I fully accept that the vast majority of workers in the public and semi-state sectors do a magnificent job - often beyond the call of duty, but they are stymied in so many ways.

And I doubt you will acknowledge it, but the primary objectives of the entire Euro crisis resolution process are to re-balance the exercise of power between sovereign and bond market participants and sovereign governments and to ensure effective EU-wide supervision of banks and regulation of financial activities.

Because the EU is an association of sovereign states and because many governing politicians (and their predecessors) misled their voters - and rightly fear their wrath - progress is grindingly slow - and far slower than Irish people would like.

And good luck with your efforts to secure the demise and abolition of capitalism.

"You may address me directly if you wish. Or perhaps you lack the bottle to address your ad hominem attack directly?"

I thought I was addressing you directly, as I used the name attached to your post. I made no personal attack on you, only criticised the ideas as expressed by you in your post. On the other hand you attacked Michael Taft’s article with accusations of ‘disingenuosness’

"My issue is with the structure, organisation and management of the public sector -..."

These are undoubtedly issues worthy of discussion but, not out of context as you attempt to do, accompanied by exaggeration of the effect of savings in state expenditure might have on reduction of current state debt. The public sector in Ireland played no part in the financial gambling which derailed the Irish economy. You failed, in your reply, to answer any of the points I raised about actually existing capitalism which contradict your demonising of the public sector.

"And I doubt you will acknowledge it, but the primary objectives of the entire Euro crisis resolution process are ...."

I have no problem acknowledging the existence of such rhetorical statements but, my doubts are whether any such statements would result in any action by the Eurocrats which would go directly against the interests of the corporate or financial monopolies which dominate the world economy today.

Worldwide, the wealthiest 10 percent of the population save most of their money. They lend savings and create new credit to the bottom 90 percent, or gamble in derivatives or other zero-sum activities in which their gain, if there is a gain, finds its counterpart in some other parties’ loss. The system is kept going not just by government spending, but by new credit creation which reaches towards infinity because of planned de-regulation of financial “markets”. That supports consumption, temporarily, and increasing lending against property assets; stocks and bonds enable borrowers to bid up their prices, allowing their owners to borrow yet more against these assets. The virtual economy expands until current revenue no longer covers the debt’s carrying charges.

That’s what brings the Bubble Economy down with a crash. Asset-price inflation gives way to crashing prices and negative equity for property owners and for much financial debt leveraging as well. When prices for property or other collateral decline, it can no longer be pledged for more loans to keep the circular flow of lending and debt repayment in motion.

This kind of circular financial flow is quite different from the circular flow that exists where workers and their employers spend their wages and profits on consumer goods and investment goods. The financial circular flow is between the increasingly monopolised banks and their clients and this circular flow swells as it diverts more and more spending from the “real” economy’s circular flow between income and spending. Finance capital expands relative to industrial capital. This is where the “imbalance” really exists in the current crisis. There is nothing in the current EU “solutions” to change the balance of power between finance and industrial capital.

"Because the EU is an association of sovereign states.."

The EU can never be anything else since there is no such thing as a “European” people, but, a collection of diverse nationalities. The fantasy dream of the Eurocrats and federalists is just that, a fantasy.

"And good luck with your efforts to secure the demise and abolition of capitalism".

It’s capitalism which needs the luck, not me. It’s doing a great job of arranging its own demise all by itself. The system only continues to exist by denying the people who work the larger part of the “fruits of their labour” by using economic coercion to force wages to the absolute tolerable minimum, given the balance of political forces at any particular time in its history, and expropriating the major part of produced value to itself.

If you cannot see that bubble-era increases in pay and employment in the public sector were funded by ephemeral taxation receipts, or that many public officials failed to provide appropriate policy advice or exercise effective bank supervision or financial regulation, or if you are convinced that the structure, financing and regulation of the provision of publicly-owned or public-directed infrastructure and utility services is efficient and requires no fundamental reform, or if you fail to grasp the thrust of the developements taking place in the EU, then there is nothing I can do or say since you are impervious to evidence and reason.

I don't always agree with Brendan Keenan - and in this instance I still don't fully agree with him, but this piece:

http://www.independent.ie/business/irish/fiscal-treaty-is-really-about-a-new-regime-to-rescue-euro-3103839.html

captures some key features of the ongoing saga.

Post a Comment