Paul Sweeney: This is the third of four (maybe five) posts on China. The first examined Chinese investment and the second FDI in China and its impact on workers’ rights and trade unions in the “communist” state. This one is about Beijing’s scramble for influence and resources in Africa.

China is Africa's second-largest trading partner after the United States. The continent needs China’ extensive investment to rebuild its failing infrastructure. Chinese companies are replacing Western companies with contracts to build roads, railways, pipelines, hydroelectric dams, and to upgrade ports.

Chinese interest in Africa is direct and indirect; large landholdings, factories, investment and construction of infrastructure etc. For example, China is rebuilding oil-rich but corrupt Nigeria's poor and inefficient railway system. However, China will supply nearly all the equipment and technical personnel, and at prices which it determines. And in line with other projects in Africa, China will supply most of the workers.

China also requires the energy supplies and huge minerals resources of Africa. The comrades in Beijing know that West African oil reserves are a resource that can reduce its dependence on volatile Middle Eastern markets.

The United States and the West are aware of the growing Chinese involvement and investment in Africa. While the United States does not have a colonial past (except as the first colony to break free) as do the major European countries, it is still viewed as the world’s only Superpower today by many in Africa. So the Chinese are welcomed.

U.S. legislation forbids aid for projects that may transfer U.S. jobs abroad, while Chinese aid is actively encouraging Chinese companies in key industries and also to even move factories to Africa. China's aid is often non-transparent, and many investments pay no attention of local interests and ignore local communities.

Ireland’s Tullow Oil is siding with the huge Chinese state oil company China National Offshore Oil Company (CNOOC) rather than with US companies. "Our shareholders believe in Africa," its boss, Aiden Heavey says. American investors, by contrast, are still wary and "tend to stick offshore". Tullow grew from nothing into the top third of the FTSE 100 with a market capitalisation of Stg£11.3bn, thanks to two of the biggest oil discoveries of the past decade, remains to a great extent "unexplored". Even last week Tullow found more oil in Ghana.

Tullow is negotiating with France's Total and CNOOC to farm out at least half its assets in Uganda's Lake Albert basin, where it has played the main role in the discovery so far of 750m barrels of oil. The deal would deliver a "hell of a combination", Mr Heavey argues.

"The Chinese will be very helpful in building up other industries and CNOOC is a very attractive option there because the Chinese have proved in the past that they will put the infrastructure in place," Heavey said, adding that Total brings oil expertise, financial firepower and long experience in Africa to the equation.

Chinese companies are also considering the purchase of interests in Nigerian oil companies, including the stakes currently held by major American companies.

Beijing is encouraging Chinese companies to buy great tracts of farmland abroad, particularly in Africa and South America, to help guarantee food security. Concern over food supplies has increased in China, Japan and Russia. Russia plans to form a state grain trading company to control up to half of the country's cereal exports. Cofco, China's state-owned food processing group, is working with Itochu, the Japanese trading company, to buy grain and other agricultural commodities in global markets to build pricing power and so combat rising food costs.

The congested roads in Nairobi are being widened and repaved as "a gift from the people of China.” While the investment will ease congestion for Kenyan motorists, it is really secondary to Chinese interests which require modern infrastructure to move African commodities to ports for shipment to China. It has been reported that China recently purchased half the farm land under cultivation in the Congo!

In Namibia, China established its first overseas military base to track its satellite and manned space flights.

The issue of Chinese involvement is not uncontested, and is turning nasty in parts of Africa. In Nigeria, the Movement for the Emancipation of the Niger Delta (MEND) has said it will expel all Chinese workers in the area. In April 2007, nine Chinese workers were killed in an attack by armed men on an oil field in eastern Ethiopia.

In South Africa, the textile union claims around 100,000 jobs have been lost as Chinese synthetic fabrics replace cotton prints in street markets across Africa and, in 2007, South Africa's unions threatened to boycott anyone selling Chinese products, including on street markets. Rene N'Guetta Kouassi, the head of the African Union's economic affairs department, warned: "Africa must not jump blindly from one type of neo-colonialism into Chinese-style neo-colonialism" (AFP, September 30th 2009).

China is known to work uncritically with some of the nastiest regimes in Africa. It sells arms, jet fighters, and military vehicles to Zimbabwe, Sudan, Ethiopia and, in the UN, China has used its veto power to block sanctions against tyrannical regimes in Sudan and Zimbabwe.

Sudan, with its huge oil reserves, is the largest recipient of Chinese investment. It sells two-thirds of its oil to Beijing. China has been criticised for its links with this government for its role in the ongoing crisis in Darfur.

The working conditions in many Chinese aid-funded projects are poor. Many Chinese developers still see environmental destruction as the price to be paid for economic progress. For example, the Bui Dam will flood a major part of a national park, and will probably generate much greenhouse gases. This dam, in Ghana, is an example of China's resource-backed lending. In 2007, China Exim Bank, the Chinese state import-export bank, approved $562 million in loans for this hydropower project on the Black Volta River. Ghana mortgaged its cocoa exports to access this loan.

China is also investing $1bn in a coal project in Mozambique’s Tete province. Wuhan Iron and Steel, one of China’s biggest steel producers, will spend $200m on an 8 per cent share of Riversdale, an Australian company developing two coalfields there. Wuhan will also commit a further $800m to the Zambezi coal reserve. The coal is one of the world’s largest untapped reserves of coking and thermal coal. Coking coal is used to make steel, while power plants provide a market for thermal coal. Wuhan will buy about 40 per cent of the coking coal produced from Zambezi, and the company will have the right to purchase at least 10 per cent of that produced from the neighbouring Benga project. And another Chinese company will build connecting infrastructure to get the coal to port by barge!

Many Chinese firms employ large numbers of local workers in many projects, but wages remain low. However, there is evidence that African workers are learning new skills because of the availability of Chinese-funded work. Taking advantage of low labour costs, the Chinese are also building factories across Africa. "China consistently respects and supports African countries," Yan Xiao Gang, China's economic attaché in Ethiopia, told the BBC. "It never imposes its own will on African countries, nor interferes in the domestic affairs of African countries."

On the plus side, Africa does well when commodity prices are high, and it is China which has pushed them up, with its huge demand. Poor African consumers like the cheap Chinese goods. Chinese migrant traders are increasingly selling cheap clothes, plastic goods, shoes, and household wares. In many of the smallest towns and the largest cities in Africa, Chinatowns are emerging up, with bazaars selling cheap imports from China. But against this, as African economies continue to export unprocessed goods, its indigenous manufacturing industry fails. And those cheap imports have threatened the collapse of Africa's textile industry, and local manufacturing. Most African countries have now a growing trade deficit with China.

African governments like China's loans which are cheaper and have much fewer strings attached than loans from the IMF or World Bank. Chinese interest in Africa is stimulating other countries and firms’ interest in the continent, and so investors and traders are setting up shop there. China's gifts to modern-day Africa will soon include a major new conference centre at the headquarters of the African Union in Addis Ababa.

In conclusion, China’s interest in Africa brings many benefits to the continent’s 50 states and its peoples, with its huge demand for resources, its investment in infrastructure, and its cheap goods for its citizens. China also gives less tied and cheaper loans than the ideologically-laced loans from the IMF and World Bank. But on the other hand, we have seen that uneven international development means that African industry is threatened, and while workers have jobs and roads, they are being exploited too.

China’s scramble for Africa is an interesting space, with many shades of history repeating itself. In the next post, I shall examine the role of Chinese state companies, just as Ireland’s short-sighted government establishes the Privatisation Board.

Friday, 30 July 2010

Thursday, 29 July 2010

The unacknowledged demise of the Government's fiscal strategy

Michael Taft: Strange how some things don’t get into the debate. For instance, the ESRI’s recent Recovery Scenarios judged the Government’s fiscal strategy a failure. It estimated that not only will the Government fail to bring public finances under control by 2014 (if we take the Maastricht guideline as the ‘control’ threshold), it will not be able to do so by 2020. Did any of this get into the debate? Were there discussions on the failure of spending cuts? No. The debate is impervious to such awkward interventions. Spending cuts are good. No amount of reality will be allowed to perturb the consensus.

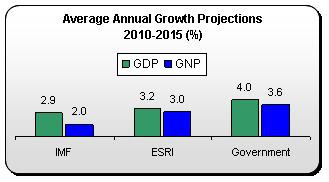

The ESRI presented two growth scenarios for the Irish economy – high-growth and low-growth. In reality, the low-growth scenario is more likely for the simple reason that it is not really ‘low’. It’s lower than the Government’s projections (which have been labelled ‘optimistic’ by the IMF and the OECD) but higher than the IMF estimates. So it’s pretty much in the mid-range.

On the basis of this low-growth scenario, the ESRI says the Government cannot reach the Maastricht threshold – not by 2014, not by 2015 not even by 2020.

• By 2015 the deficit is estimated to be 4.1 percent (not counting any banking subsidies)

• By 2020 the deficit is estimated to be 4.5 percent

In addition, they estimate our overall debt levels will be 102 percent of GDP in 2015, rising to 106 percent five years later.

The reason the deficit and debt start rising after 2015 is because the ESRI estimates that real growth will start to ease off, falling from an average 3.2 percent over the next five years, to 2.1 percent afterwards. On this basis, we would have to cut the deficit to well below -3 percent by 2015, just to ensure we don’t rise above it again in a few years. They summarise the problem:

‘The lower level of economic activity would reduce government revenue from taxation while the higher unemployment rate and borrowing would increase government expenditure on welfare payments and interest payments. This would result in a significant deterioration in the general government balance . . ‘

So why, according to the ESRI, would this state of affairs come about? They first assume the economy won’t respond to increased world growth as robustly as in the past. But they also point out that a poorly functioning banking system, higher cost of capital and structural unemployment could also contribute to a low-growth scenario.

What they don’t mention is the impact of the Government’s deflationary cuts - which is strange since they point out that the Government’s €3 billion fiscal contraction in the 2011 budget will cut economic growth (by approximately 1 percent – though this was before the Government’s announcement that spending cuts, which are more deflationary, will play a more prominent role in the composition of the contraction).

It is even stranger since they have just released a revised set of fiscal multipliers, updating their paper from last year. These updated multipliers show that they previously under-estimated the impact of spending cuts on economic growth:

• A €1 billion cut in public sector wages will reduce GNP by 0.4 percent (previously it was 0.3 percent)

• A €1 billion cut in public sector employment (about 17,000 jobs) will reduce GNP growth by 1.0 percent (previously t was 0.9 percent)

These might seem marginal but given the scale of cutbacks the Government (€2.4 billion in pay cuts, €3.6 billion in non-wage consumption, €2.6 billion in investment cuts), it all adds up.

The key metric is employment and this, more than anything else, helps explain the low levels of growth and, so, the failure of the Government’s fiscal policy. The ESRI estimates that employment will grow by an average 1.3 percent between 2010 and 2015. This compares to the Government’s estimate of 2.0 percent average.

Again, this might not seem much but add it up. But by 2015, the ESRI is estimating we will have approximately 70,000 fewer jobs than the Government’s projections. When you factor in the impact on tax revenue, unemployment costs and the significant social costs of long-term and structural unemployment – you start to see why the Government’s fiscal strategy will fail.

None of this should come as any news – if we were fortunate to get the news: the IMF similarly projected the Government’s fiscal strategy will fail. So, too, did the Ernst & Young / Oxford Economics report (though they held out hope that the deficit might come under control by 2018/2019 – but only at growth rates that exceed the ESRI’s estimates).

Of course, some might be tempted to say, that after nearly €9 billion of spending cuts with the prospect of billions more planned, all we need to do is cut just that little bit more. Just dig a little deeper and we’ll get out of the hole. But that’s the problem – every new estimate, every new projection tells us that fiscal consolidation is getting further and further away the more we cut. How much longer do we go along with this ‘Boxer mentality’ in the face of an emerging consensus that the Government’s strategy is flawed at its core; that no amount of tweaking will rescue it. Indeed, further cuts, in addition to what the Government is planning, will only undermine economic and employment growth even more. What will we do then? Call for even more cuts? How deep does the hole have to get before we stop digging?

So what have got? Low growth, escalating debt, high unemployment and emigration, sluggish economy – and the failure to repair public finances; if the ESRI buried the Government’s fiscal consolidation strategy, it also buried the McCarthy report. You probably didn’t hear about that either.

That’s why my next post will deal with that.

The ESRI presented two growth scenarios for the Irish economy – high-growth and low-growth. In reality, the low-growth scenario is more likely for the simple reason that it is not really ‘low’. It’s lower than the Government’s projections (which have been labelled ‘optimistic’ by the IMF and the OECD) but higher than the IMF estimates. So it’s pretty much in the mid-range.

On the basis of this low-growth scenario, the ESRI says the Government cannot reach the Maastricht threshold – not by 2014, not by 2015 not even by 2020.

• By 2015 the deficit is estimated to be 4.1 percent (not counting any banking subsidies)

• By 2020 the deficit is estimated to be 4.5 percent

In addition, they estimate our overall debt levels will be 102 percent of GDP in 2015, rising to 106 percent five years later.

The reason the deficit and debt start rising after 2015 is because the ESRI estimates that real growth will start to ease off, falling from an average 3.2 percent over the next five years, to 2.1 percent afterwards. On this basis, we would have to cut the deficit to well below -3 percent by 2015, just to ensure we don’t rise above it again in a few years. They summarise the problem:

‘The lower level of economic activity would reduce government revenue from taxation while the higher unemployment rate and borrowing would increase government expenditure on welfare payments and interest payments. This would result in a significant deterioration in the general government balance . . ‘

So why, according to the ESRI, would this state of affairs come about? They first assume the economy won’t respond to increased world growth as robustly as in the past. But they also point out that a poorly functioning banking system, higher cost of capital and structural unemployment could also contribute to a low-growth scenario.

What they don’t mention is the impact of the Government’s deflationary cuts - which is strange since they point out that the Government’s €3 billion fiscal contraction in the 2011 budget will cut economic growth (by approximately 1 percent – though this was before the Government’s announcement that spending cuts, which are more deflationary, will play a more prominent role in the composition of the contraction).

It is even stranger since they have just released a revised set of fiscal multipliers, updating their paper from last year. These updated multipliers show that they previously under-estimated the impact of spending cuts on economic growth:

• A €1 billion cut in public sector wages will reduce GNP by 0.4 percent (previously it was 0.3 percent)

• A €1 billion cut in public sector employment (about 17,000 jobs) will reduce GNP growth by 1.0 percent (previously t was 0.9 percent)

These might seem marginal but given the scale of cutbacks the Government (€2.4 billion in pay cuts, €3.6 billion in non-wage consumption, €2.6 billion in investment cuts), it all adds up.

The key metric is employment and this, more than anything else, helps explain the low levels of growth and, so, the failure of the Government’s fiscal policy. The ESRI estimates that employment will grow by an average 1.3 percent between 2010 and 2015. This compares to the Government’s estimate of 2.0 percent average.

Again, this might not seem much but add it up. But by 2015, the ESRI is estimating we will have approximately 70,000 fewer jobs than the Government’s projections. When you factor in the impact on tax revenue, unemployment costs and the significant social costs of long-term and structural unemployment – you start to see why the Government’s fiscal strategy will fail.

None of this should come as any news – if we were fortunate to get the news: the IMF similarly projected the Government’s fiscal strategy will fail. So, too, did the Ernst & Young / Oxford Economics report (though they held out hope that the deficit might come under control by 2018/2019 – but only at growth rates that exceed the ESRI’s estimates).

Of course, some might be tempted to say, that after nearly €9 billion of spending cuts with the prospect of billions more planned, all we need to do is cut just that little bit more. Just dig a little deeper and we’ll get out of the hole. But that’s the problem – every new estimate, every new projection tells us that fiscal consolidation is getting further and further away the more we cut. How much longer do we go along with this ‘Boxer mentality’ in the face of an emerging consensus that the Government’s strategy is flawed at its core; that no amount of tweaking will rescue it. Indeed, further cuts, in addition to what the Government is planning, will only undermine economic and employment growth even more. What will we do then? Call for even more cuts? How deep does the hole have to get before we stop digging?

So what have got? Low growth, escalating debt, high unemployment and emigration, sluggish economy – and the failure to repair public finances; if the ESRI buried the Government’s fiscal consolidation strategy, it also buried the McCarthy report. You probably didn’t hear about that either.

That’s why my next post will deal with that.

Evolution ... and economists

The following is the text of a letter from Terry McDonough carried in today's Irish Times:

Michael Casey, reviewing The Company of Strangers: A Natural History of Economic Life (Business, July 26th), reads that evolutionary theorists believe the murder of 20 million Congolese by Belgian colonists was not down to imperialism but due to an evolutionary failure to develop sufficient trust in strangers. And yet the remainder of that day’s business pages are replete with the most touching examples of misplaced trust. We learn from Wolfgang Munchau that the strategy behind the recently completed stress tests (grade inflation for banks) was premised on the assumption of an innocent trust in the results by investors and the public, validated apparently by your reports of a positive response from “the markets”.

We are informed by Tony Jackson that pension funds are still too trusting of the private equity industry despite a report on the opposite page that this industry has “underperformed stockmarkets, taken excessive risks, and overcharged investors”. We find out that despite rising losses at Aras Sláinte, “the group continues to have the solid support of its bankers and shareholders” (one of whom is reported to be a private equity firm associated with Anglo-Irish bank). Speaking of Anglo-Irish bank, we find that after the NAMA process, it lent a developer a further €25 million and entrusted him with a line of credit for over €353 million. Still on NAMA, a survey finds that 66 per cent of Irish chief financial officers think NAMA will improve credit availability.

Finally, in what is perhaps the most moving example, we are told that, in response to queries over royalty payments to executives, director Ivan Yates is reassured because management has said its lawyers and auditors approved the controversial payments. According to the scientists, all of this would seem to violate basic human nature. On this evidence, evolutionary psychologists would appear to be no more worthy of trust than say . . . economists.

Michael Casey, reviewing The Company of Strangers: A Natural History of Economic Life (Business, July 26th), reads that evolutionary theorists believe the murder of 20 million Congolese by Belgian colonists was not down to imperialism but due to an evolutionary failure to develop sufficient trust in strangers. And yet the remainder of that day’s business pages are replete with the most touching examples of misplaced trust. We learn from Wolfgang Munchau that the strategy behind the recently completed stress tests (grade inflation for banks) was premised on the assumption of an innocent trust in the results by investors and the public, validated apparently by your reports of a positive response from “the markets”.

We are informed by Tony Jackson that pension funds are still too trusting of the private equity industry despite a report on the opposite page that this industry has “underperformed stockmarkets, taken excessive risks, and overcharged investors”. We find out that despite rising losses at Aras Sláinte, “the group continues to have the solid support of its bankers and shareholders” (one of whom is reported to be a private equity firm associated with Anglo-Irish bank). Speaking of Anglo-Irish bank, we find that after the NAMA process, it lent a developer a further €25 million and entrusted him with a line of credit for over €353 million. Still on NAMA, a survey finds that 66 per cent of Irish chief financial officers think NAMA will improve credit availability.

Finally, in what is perhaps the most moving example, we are told that, in response to queries over royalty payments to executives, director Ivan Yates is reassured because management has said its lawyers and auditors approved the controversial payments. According to the scientists, all of this would seem to violate basic human nature. On this evidence, evolutionary psychologists would appear to be no more worthy of trust than say . . . economists.

Tuesday, 27 July 2010

The Austerity Debate

Slí Eile: Don't miss the Great Austerity Debate running on the Financial Times at this site. Some heavy hitters have weighed in followed by a thread of comments. You may have missed the Austerity debate on the home ground on irisheconomy here. Funny thing right now is that if you ask people are they for or agin stimulus/deflation they will tell you that they are all for a jobs-creating stimulus while, at the same time, imposing pain through deflation. Pain must be good. Per crucem ad lucem is the battle cry of the deflationists - to the light via the cross. Yet, the evidence that stimulus will not work, cannot be afforded and could spook the markets is thin. It is incumbent on those of us who argue for stimulus to spell out what it would mean, how long it would run, what levels of spending, taxation and borrowing at home and abroad would be envisaged and what sets of assumptions, scenarios and 'what if' circumstances were factored in. The debate, internationally, will not go away as most industrial economies stuck in a deficit trap and trade/capital imbalance cannot easily deflate their way of the impasse. Neither can they readily devalue or pump prime their way out. The fundamental contradictions within a 'for profit' economy have come home to roost. Yet, the time is not right for a fundamental change in economic and social relations - or is it? Underlying all the simulations and scenarios considered by agencies from ESRI to OECD to IMF to ECion is the presumption that the current world order and system of economic production is here to stay. We need to think bigger and bolder than that - if only for the sake of the coming generations. We need a vision stimulus to offer hope and justice where governments, media conspire to depress and sometimes deceive.

Minimum wage - facts, fiction and flights of fancy

Sinéad Pentony: The minimum wage rate is €8.65 per hour and it has been frozen since 2007. The introduction of the two per cent income levy in the 2009 supplementary budget resulted in an effective cut to the minimum wage reducing it to €8.48, because if your income is greater than the minimum threshold of €15,028 per year or €289 per week, you pay the levy on the full amount of your income. There have recently been calls by the Restaurant Association of Ireland (RAI) for JLC rates to be reduced to the minimum wage level, and from other business lobbies for a reduction in the minimum wage by one euro.

It was in that context that TASC made a presentation to the Oireachtas Joint Committee on Enterprise, Trade and Employment on ‘The Minimum Wage’. TASC’s evidence demonstrated that any reduction to the minimum wage would exacerbate the deflationary situation and have a negative impact on the public finances. In the media debate following TASC’s submission, the business lobbies focused on the cost of the minimum wage and how it is ‘unsustainable’, ‘preventing businesses from hiring’ and ‘a major contributor to a loss in competitiveness’. Once again, it’s important to identify the facts from the fiction in relation to the minimum wage and to look at the latest evidence on competitiveness.

Despite what you may read or hear, the minimum wage rate is not the second highest in Europe for the following reasons:

1. First, when comparing minimum wages across a number of countries you can only do so by taking the Purchasing Power Parities into consideration i.e. calculating how much you can buy with your minimum wages. This is done by expressing the minimum wage in terms of a common unit called the Purchasing Power Standard (PPS). When expressed in PPS terms, Ireland’s ranking drops from second to sixth place, reflecting our higher cost of living. Ireland’s monthly minimum wage is €1,152 in PPS. The UK is in fifth place with a monthly minimum wage of €1,154 (in PPS) and France in fourth place with a monthly minimum wage of €1,189 (in PPS)(details here).

2. Second, Eurostat data calculates wages per month. Ireland’s monthly rates are calculated on the basis of a 39 hour week, France on the basis of a 35 hour week and the UK on the basis of the 38.1 hour week. If we differentiate for the number of hours worked in the three countries we find that the hourly minimum wage is €7.84 (PPS) in France; €6.99 (PPS) in the UK and €6.82 (PPS) in Ireland.

3. Third, the data only refers to those European Members that have statutory minimum wages. This means that the dataset does not include the Scandinavian countries. Collective bargaining is used to set minimum wages in these countries and an October 2008 study by Swedish economists showed that Sweden, Finland and Denmark all had higher hourly minimum wages in 2006 than Ireland, as did Norway which is not a member of the EU.

4. Eurostat also calculates the minimum wage as a per cent of average monthly earnings. The minimum wage in Ireland was 42 per cent of average industrial earnings in 2008, which puts Ireland in ninth place in the EU, or in twelfth place if we include the corresponding 2006 percentages for the Scandinavian countries

When calculating the cost of employing a person, it is more accurate to look at the overall cost of labour which is made up of labour and payroll taxes (PRSI). Ireland has one of the lowest levels of employers’ social protection contribution in the OECD. The Irish rate (10.8 per cent) is significantly lower than the OECD average (15.2 per cent) and the euro area average (27 per cent), which reduces the total cost of employing workers in Ireland. The hospitality sector is the largest employer of low wage workers and labour costs in Ireland in this sector are the third lowest in the EU 15. Only Greece and Portugal had lower costs per employee than Ireland.

When we look at the facts in the cold light of day it is clear that the minimum wage is not out of step with other European countries and when we consider the total costs of employing people, Ireland is indeed very competitive. However, if the minimum wage is causing serious problems for businesses, surely it would be highlighted in any analysis of competition?

Last week the National Competitiveness Council published its annual report on competitiveness for 2010, and it demonstrates that the minimum wage is not a factor impacting on business’s capacity to survive the current challenging trading environment. They found that Ireland’s cost competitiveness has improved considerably for a range of key business inputs such as energy, property and a number of business services. However, the areas where key inputs in Ireland remain relatively expensive include broadband, waste disposal and legal fees. There is no mention of the minimum wage being prohibitive for business ... and in fact the report found that “Irish salary levels are broadly in line with the euro area average across the benchmarked occupations”(p.22.)

Business lobby groups have also been arguing that the minimum wage is preventing them from hiring, and that the costs associated with hiring minimum wage workers is putting business under pressure. This argument is not supported by a single shred of evidence. In fact, the evidence supports the opposite – that the minimum wage has little or no impact on employment. David Metcalf at the London School of Economics undertook empirical research and a wide ranging review of the literature in 2007 and found that the British National Minimum Wage has little or no impact on employment (see also here).

There is no doubt that the recession has impacted on businesses and has led to many businesses having to close their doors and cease trading. However, these difficulties have not been caused by the minimum wage. Factors such as access to credit, high commercial rents, professional fees, waste charges, the price of food and the collapse in demand, in particular, have had a devastating effect on the SME sector. These are the factors that need to be addressed to support businesses in these difficult times – rather than an unsubstantiated attack on the lowest paid workers in our economy.

It was in that context that TASC made a presentation to the Oireachtas Joint Committee on Enterprise, Trade and Employment on ‘The Minimum Wage’. TASC’s evidence demonstrated that any reduction to the minimum wage would exacerbate the deflationary situation and have a negative impact on the public finances. In the media debate following TASC’s submission, the business lobbies focused on the cost of the minimum wage and how it is ‘unsustainable’, ‘preventing businesses from hiring’ and ‘a major contributor to a loss in competitiveness’. Once again, it’s important to identify the facts from the fiction in relation to the minimum wage and to look at the latest evidence on competitiveness.

Despite what you may read or hear, the minimum wage rate is not the second highest in Europe for the following reasons:

1. First, when comparing minimum wages across a number of countries you can only do so by taking the Purchasing Power Parities into consideration i.e. calculating how much you can buy with your minimum wages. This is done by expressing the minimum wage in terms of a common unit called the Purchasing Power Standard (PPS). When expressed in PPS terms, Ireland’s ranking drops from second to sixth place, reflecting our higher cost of living. Ireland’s monthly minimum wage is €1,152 in PPS. The UK is in fifth place with a monthly minimum wage of €1,154 (in PPS) and France in fourth place with a monthly minimum wage of €1,189 (in PPS)(details here).

2. Second, Eurostat data calculates wages per month. Ireland’s monthly rates are calculated on the basis of a 39 hour week, France on the basis of a 35 hour week and the UK on the basis of the 38.1 hour week. If we differentiate for the number of hours worked in the three countries we find that the hourly minimum wage is €7.84 (PPS) in France; €6.99 (PPS) in the UK and €6.82 (PPS) in Ireland.

3. Third, the data only refers to those European Members that have statutory minimum wages. This means that the dataset does not include the Scandinavian countries. Collective bargaining is used to set minimum wages in these countries and an October 2008 study by Swedish economists showed that Sweden, Finland and Denmark all had higher hourly minimum wages in 2006 than Ireland, as did Norway which is not a member of the EU.

4. Eurostat also calculates the minimum wage as a per cent of average monthly earnings. The minimum wage in Ireland was 42 per cent of average industrial earnings in 2008, which puts Ireland in ninth place in the EU, or in twelfth place if we include the corresponding 2006 percentages for the Scandinavian countries

When calculating the cost of employing a person, it is more accurate to look at the overall cost of labour which is made up of labour and payroll taxes (PRSI). Ireland has one of the lowest levels of employers’ social protection contribution in the OECD. The Irish rate (10.8 per cent) is significantly lower than the OECD average (15.2 per cent) and the euro area average (27 per cent), which reduces the total cost of employing workers in Ireland. The hospitality sector is the largest employer of low wage workers and labour costs in Ireland in this sector are the third lowest in the EU 15. Only Greece and Portugal had lower costs per employee than Ireland.

When we look at the facts in the cold light of day it is clear that the minimum wage is not out of step with other European countries and when we consider the total costs of employing people, Ireland is indeed very competitive. However, if the minimum wage is causing serious problems for businesses, surely it would be highlighted in any analysis of competition?

Last week the National Competitiveness Council published its annual report on competitiveness for 2010, and it demonstrates that the minimum wage is not a factor impacting on business’s capacity to survive the current challenging trading environment. They found that Ireland’s cost competitiveness has improved considerably for a range of key business inputs such as energy, property and a number of business services. However, the areas where key inputs in Ireland remain relatively expensive include broadband, waste disposal and legal fees. There is no mention of the minimum wage being prohibitive for business ... and in fact the report found that “Irish salary levels are broadly in line with the euro area average across the benchmarked occupations”(p.22.)

Business lobby groups have also been arguing that the minimum wage is preventing them from hiring, and that the costs associated with hiring minimum wage workers is putting business under pressure. This argument is not supported by a single shred of evidence. In fact, the evidence supports the opposite – that the minimum wage has little or no impact on employment. David Metcalf at the London School of Economics undertook empirical research and a wide ranging review of the literature in 2007 and found that the British National Minimum Wage has little or no impact on employment (see also here).

There is no doubt that the recession has impacted on businesses and has led to many businesses having to close their doors and cease trading. However, these difficulties have not been caused by the minimum wage. Factors such as access to credit, high commercial rents, professional fees, waste charges, the price of food and the collapse in demand, in particular, have had a devastating effect on the SME sector. These are the factors that need to be addressed to support businesses in these difficult times – rather than an unsubstantiated attack on the lowest paid workers in our economy.

Monday, 26 July 2010

Selling the family silver: bad for the economy and citizens

Tom O'Connor: The newly established government Review Group on State Assets and Liabilities has been assigned a task: ‘To draw up a list of possible asset disposals’. The range of state owned enterprises which could be up for grabs is breathtaking and includes: all the main Irish ports; Bord Gais; the ESB; RTE; An Post; CIE; Dublin Bus; Irish Rail, the National Oil Reserves Agency and many others.

The plan is to raise billions for the state coffers from the sale of many of these companies. The hope is that this could be set off against the projected exchequer deficit of €26 billion for next year and the national debt which now stands at €84 billion. Many of these companies are indeed valuable. The values put on Bord Gais and ESB are €3.5 and €5 billion respectively.

However, it would be a serious mistake to sell off these state owned enterprises. The proposed sales are a smash and grab exercise aimed at raising quick money for the government without any real consideration of the consequences. The problems which the sale of Eircom continues to cause for the Irish economy highlight the dangers of privatisation.

The sale of Eircom raised €8.4 billion for the government but has done untold damage to the competitiveness of the Irish economy: the company has been bought and sold several times, and has had four different owners in recent years. The sale has resulted in the company not been able to develop its broadband infrastructure to anything like the level which is required in the modern business environment, and this has hampered the development of high speed internet in Ireland ever since.

In the aftermath of the various sales of the company in the hands of ruthless venture capitalists, it now owes nearly €2 billion. Previously it owed very little. It has also started to shed considerable numbers of workers and has only limited ability, as a result of its debt, to finance the rolling out of high speed broadband.

The privatisation of state enterprises is based on an ideological position which assumes that private companies achieve higher levels of performance than state owned enterprises. However, a study of companies privatised by the Irish government from 1991 to 2003 by Reeves and Palcic (2005) found no evidence for this assertion. They also found that shareholders and employees who receive 15% of the shares tend to be the main winners in privatisation, not the government.

Perhaps one of the most compelling arguments against the sale of State Owned Enterprises is the loss of national control overall in hugely strategic areas which determine our economic viability and competitiveness. If the two largest energy producing companies where sold to private investors, industry and consumers could end up being at the mercy of super-profit-seeking business owners which could drive up costs and make Irish businesses uncompetitive. At present, the government by way of the energy regulator can control the price of energy.

It is precisely due to super-profit-seeking privately owned businesses controlling goods and services that should be kept in state ownership, that health care is so expensive in the USA. There, private Health Management Companies (HMOs) own most hospitals and charge exorbitant fees. The result is that basic health insurance is at least 800 dollars a month per person in the USA. The same argument can be cited to oppose the privatisation of the countries ports, RTE and others. It has been reported that Ruport Murdoch is interested in purchasing RTE. In that event, once in an almost monopoly position, the cost of TV viewing would be likely to rise significantly.

The sale of ports would put the country at a huge strategic disadvantage. The UK government in recent years has privatised its ports for a return of 6 billion and has sold the London-based Thames Water company for 9 billion. If Ireland were to sell its ports and its domestic water infrastructure, it is likely that these utilities would be run as public-private partnerships (PPS). These are exceptionally costly for the state and the taxpayer in the long term, and it is likely that hefty charges for water and the use of ports would ensue to the hardship of consumers and the disadvantage of businesses. One might also argue that the loss of ownership and strategic control of a country’s ports strongly compromises national sovereignty.

Also, in Ireland at present, the ESB is responsible for integrating its supply grid with that in Northern Ireland in a move towards closer economic co-operation, which was been lauded only this week by Northern Ireland’s Deputy First Minister Martin Mc Guinness at the Magill Summer School. If the ESB were owned by private shareholders, there is no guarantee that this would happen.

Of course, the biggest problem is the loss of employment. In the wake of the privatisation of ACC Bank and Aer Lingus (amongst others) since 2005, the Central Statistics Office has shown that the numbers employed in state owned enterprises fell from 57,400 to 52,300 by 2009, a loss of 5,100 jobs, which the CSO attributes mainly to privatisation.

The privatisation of Bord Gais, ESB, An Post and other semi-state companies would result in a dramatic downsizing of the workforces in these companies. At a time when unemployment stands at 450,000 and where the government is content to sit out the recession without stimulating the economy, the prospect of the state itself putting thousands or even tens of thousands people out of work, due to privatisations, would seem to be unthinkable.

Interestingly, it is the opposite course of action which is now being proposed in the global post-financial meltdown world: Prof. Aldo Mustacchio of Harvard Business School has written several papers in the past two years in which he highlights the need to use state owned enterprises as vehicles for employment creation and to help significantly in national economic recovery.

Many large state owned enterprises have been performing exceptionally throughout the world, he says, from the state owned oil company Petrobas in Brazil to Statoil in Norway and the State owned Gazprom company in Russia. There are many other companies in other economic sectors also in countries such as Singapore and India. The mistake in Ireland has been to allow private interests to take control of valuable natural resources with no return to the exchequer. The case of the Erris gas field in Mayo, which was essentially given away free of charge by then Minister for Energy, Ray Burke in the mid 1990s, is a case in point.

However, it would be a mistake to think that new state owned enterprises would be flabby and inefficient which many politicians and economists from a right-wing persuasion would have us believe. There is a future for lean and competitive state owned enterprises in Ireland where performance and productivity would be high and where performance management systems would predominate.

State owned companies of this type have existed in Sweden for many years. At present there are 55 state owned enterprises in Sweden. In 2006 these companies turned over 50 billion and generated net profits of 8 billion for the exchequer.

It is for these reasons that any hasty attempt by government to sell the family silver in an ill thought out and hasty fashion to reduce indebtedness should be strenuously opposed by Irish society.

This piece first appeared in the Irish Examiner

The plan is to raise billions for the state coffers from the sale of many of these companies. The hope is that this could be set off against the projected exchequer deficit of €26 billion for next year and the national debt which now stands at €84 billion. Many of these companies are indeed valuable. The values put on Bord Gais and ESB are €3.5 and €5 billion respectively.

However, it would be a serious mistake to sell off these state owned enterprises. The proposed sales are a smash and grab exercise aimed at raising quick money for the government without any real consideration of the consequences. The problems which the sale of Eircom continues to cause for the Irish economy highlight the dangers of privatisation.

The sale of Eircom raised €8.4 billion for the government but has done untold damage to the competitiveness of the Irish economy: the company has been bought and sold several times, and has had four different owners in recent years. The sale has resulted in the company not been able to develop its broadband infrastructure to anything like the level which is required in the modern business environment, and this has hampered the development of high speed internet in Ireland ever since.

In the aftermath of the various sales of the company in the hands of ruthless venture capitalists, it now owes nearly €2 billion. Previously it owed very little. It has also started to shed considerable numbers of workers and has only limited ability, as a result of its debt, to finance the rolling out of high speed broadband.

The privatisation of state enterprises is based on an ideological position which assumes that private companies achieve higher levels of performance than state owned enterprises. However, a study of companies privatised by the Irish government from 1991 to 2003 by Reeves and Palcic (2005) found no evidence for this assertion. They also found that shareholders and employees who receive 15% of the shares tend to be the main winners in privatisation, not the government.

Perhaps one of the most compelling arguments against the sale of State Owned Enterprises is the loss of national control overall in hugely strategic areas which determine our economic viability and competitiveness. If the two largest energy producing companies where sold to private investors, industry and consumers could end up being at the mercy of super-profit-seeking business owners which could drive up costs and make Irish businesses uncompetitive. At present, the government by way of the energy regulator can control the price of energy.

It is precisely due to super-profit-seeking privately owned businesses controlling goods and services that should be kept in state ownership, that health care is so expensive in the USA. There, private Health Management Companies (HMOs) own most hospitals and charge exorbitant fees. The result is that basic health insurance is at least 800 dollars a month per person in the USA. The same argument can be cited to oppose the privatisation of the countries ports, RTE and others. It has been reported that Ruport Murdoch is interested in purchasing RTE. In that event, once in an almost monopoly position, the cost of TV viewing would be likely to rise significantly.

The sale of ports would put the country at a huge strategic disadvantage. The UK government in recent years has privatised its ports for a return of 6 billion and has sold the London-based Thames Water company for 9 billion. If Ireland were to sell its ports and its domestic water infrastructure, it is likely that these utilities would be run as public-private partnerships (PPS). These are exceptionally costly for the state and the taxpayer in the long term, and it is likely that hefty charges for water and the use of ports would ensue to the hardship of consumers and the disadvantage of businesses. One might also argue that the loss of ownership and strategic control of a country’s ports strongly compromises national sovereignty.

Also, in Ireland at present, the ESB is responsible for integrating its supply grid with that in Northern Ireland in a move towards closer economic co-operation, which was been lauded only this week by Northern Ireland’s Deputy First Minister Martin Mc Guinness at the Magill Summer School. If the ESB were owned by private shareholders, there is no guarantee that this would happen.

Of course, the biggest problem is the loss of employment. In the wake of the privatisation of ACC Bank and Aer Lingus (amongst others) since 2005, the Central Statistics Office has shown that the numbers employed in state owned enterprises fell from 57,400 to 52,300 by 2009, a loss of 5,100 jobs, which the CSO attributes mainly to privatisation.

The privatisation of Bord Gais, ESB, An Post and other semi-state companies would result in a dramatic downsizing of the workforces in these companies. At a time when unemployment stands at 450,000 and where the government is content to sit out the recession without stimulating the economy, the prospect of the state itself putting thousands or even tens of thousands people out of work, due to privatisations, would seem to be unthinkable.

Interestingly, it is the opposite course of action which is now being proposed in the global post-financial meltdown world: Prof. Aldo Mustacchio of Harvard Business School has written several papers in the past two years in which he highlights the need to use state owned enterprises as vehicles for employment creation and to help significantly in national economic recovery.

Many large state owned enterprises have been performing exceptionally throughout the world, he says, from the state owned oil company Petrobas in Brazil to Statoil in Norway and the State owned Gazprom company in Russia. There are many other companies in other economic sectors also in countries such as Singapore and India. The mistake in Ireland has been to allow private interests to take control of valuable natural resources with no return to the exchequer. The case of the Erris gas field in Mayo, which was essentially given away free of charge by then Minister for Energy, Ray Burke in the mid 1990s, is a case in point.

However, it would be a mistake to think that new state owned enterprises would be flabby and inefficient which many politicians and economists from a right-wing persuasion would have us believe. There is a future for lean and competitive state owned enterprises in Ireland where performance and productivity would be high and where performance management systems would predominate.

State owned companies of this type have existed in Sweden for many years. At present there are 55 state owned enterprises in Sweden. In 2006 these companies turned over 50 billion and generated net profits of 8 billion for the exchequer.

It is for these reasons that any hasty attempt by government to sell the family silver in an ill thought out and hasty fashion to reduce indebtedness should be strenuously opposed by Irish society.

This piece first appeared in the Irish Examiner

Stimulus and austerity

Peter Connell: Over on irisheconomy.ie there has been an enlightening discussion on one of our favourite topics – austerity versus stimulus. The discussion, at least in parts, seems to represent a genuine engagement between those who believe a stimulus package would be misguided given the state’s fiscal deficit and open economy (a belief espoused by the overwhelming majority of economists, journalists and politicians) and those who argue that a properly targeted stimulus can start to address the critical issue of mass unemployment, depressed domestic demand and the fiscal deficit itself (the position we’re pretty familiar with here on progressive-economy).

Up to now there has been no debate. Part of the reason is that it’s extremely difficult the get the pro-stimulus arguments into the public domain. Those who comment on economic issues in the national media almost all subscribe to the ‘fiscal austerity’ consensus. Those who put forward the pro-stimulus position are routinely dismissed as not understanding the gravity of the State’s fiscal position or promoting narrow sectional interests. During the week, Paul Krugman bemoaned the quality of economic discourse on both sides of the Atlantic. In Ireland we should be so lucky to have the kind of discourse that’s taking place in the US and the UK, for example! So, in that context we should welcome the engagement that’s taking place between Karl Whelan, Michael Burke and Michael Taft on irisheconomy.ie. It’s a start.

What’s less encouraging is the content of the interview given by Eamon Gilmore on the Pat Kenny show last Monday morning. In the interview, Gilmore firmly nails his colours to the mast by affirming the Labour Party’s support for a €3 billion fiscal contraction in the forthcoming December budget. He goes on to express support for the government’s stated target of reducing the deficit to less than 3% of GDP by 2014.

On the latter point, this seems an ill-advised position for a prospective Taoiseach to adopt. If, as most progressives hope, Gilmore is Taoiseach after the next election, then his stated commitment to meeting this 3% target may be one he regrets making as most independent commentators now accept that Ireland has little prospect of meeting it in 2014. The IMF recently predicted that our deficit will be 5.9% in 2014 (see page 30 of the report). The Ernst & Young / Oxford Economics survey suggests we won't reach Maastrich compliance until 2018/2019. Further, two days later the ESRI report (see page 79) implied that additional fiscal contraction beyond that already planned by the government would be required to meet the 3% target.

From a policy point of view the realistic (and sensible) thing to do is set this 2014 – 3% straightjacket aside. That opens out the debate and helps focus on the fact that the deflationary policies pursued to date are strangling the domestic economy and suppressing the growth in revenue which has to be part of any solution that addresses the deficit in the medium term.

Eamon Gilmore’s stated support for a €3 billion ‘fiscal correction’ in the December budget is even more unfortunate. In fairness, in the interview he indicates that the €1 cut in the capital programme would be supplemented by funds from the Strategic Investment Bank the party proposes to establish (hardly realistic in the context of the December budget) and part of the cut in current spending would come from the reform of property and pension tax allowances. Unfortunately, in terms of the public discourse on macroeconomic policy, these details will receive little prominence. By supporting the €3 billion fiscal correction, the Labour Party ends up being co-opted on to the side of those arguing that there is no alternative to fiscal austerity. The result is that the range of ideas that gain prominence in the public domain is reduced, and we end up with an even more lop-sided debate on how to solve our problems. The consensus reigns.

Up to now there has been no debate. Part of the reason is that it’s extremely difficult the get the pro-stimulus arguments into the public domain. Those who comment on economic issues in the national media almost all subscribe to the ‘fiscal austerity’ consensus. Those who put forward the pro-stimulus position are routinely dismissed as not understanding the gravity of the State’s fiscal position or promoting narrow sectional interests. During the week, Paul Krugman bemoaned the quality of economic discourse on both sides of the Atlantic. In Ireland we should be so lucky to have the kind of discourse that’s taking place in the US and the UK, for example! So, in that context we should welcome the engagement that’s taking place between Karl Whelan, Michael Burke and Michael Taft on irisheconomy.ie. It’s a start.

What’s less encouraging is the content of the interview given by Eamon Gilmore on the Pat Kenny show last Monday morning. In the interview, Gilmore firmly nails his colours to the mast by affirming the Labour Party’s support for a €3 billion fiscal contraction in the forthcoming December budget. He goes on to express support for the government’s stated target of reducing the deficit to less than 3% of GDP by 2014.

On the latter point, this seems an ill-advised position for a prospective Taoiseach to adopt. If, as most progressives hope, Gilmore is Taoiseach after the next election, then his stated commitment to meeting this 3% target may be one he regrets making as most independent commentators now accept that Ireland has little prospect of meeting it in 2014. The IMF recently predicted that our deficit will be 5.9% in 2014 (see page 30 of the report). The Ernst & Young / Oxford Economics survey suggests we won't reach Maastrich compliance until 2018/2019. Further, two days later the ESRI report (see page 79) implied that additional fiscal contraction beyond that already planned by the government would be required to meet the 3% target.

From a policy point of view the realistic (and sensible) thing to do is set this 2014 – 3% straightjacket aside. That opens out the debate and helps focus on the fact that the deflationary policies pursued to date are strangling the domestic economy and suppressing the growth in revenue which has to be part of any solution that addresses the deficit in the medium term.

Eamon Gilmore’s stated support for a €3 billion ‘fiscal correction’ in the December budget is even more unfortunate. In fairness, in the interview he indicates that the €1 cut in the capital programme would be supplemented by funds from the Strategic Investment Bank the party proposes to establish (hardly realistic in the context of the December budget) and part of the cut in current spending would come from the reform of property and pension tax allowances. Unfortunately, in terms of the public discourse on macroeconomic policy, these details will receive little prominence. By supporting the €3 billion fiscal correction, the Labour Party ends up being co-opted on to the side of those arguing that there is no alternative to fiscal austerity. The result is that the range of ideas that gain prominence in the public domain is reduced, and we end up with an even more lop-sided debate on how to solve our problems. The consensus reigns.

Saturday, 24 July 2010

The Economics Anti-Textbook....at last some fresh thinking on economics

John Barry: Have just received a review copy of The Economics Anti-Textbook: A Critical Thinker's Guide to Micro-economics by Rod Hill and Tony Myatt http://www.zedbooks.co.uk/book.asp?bookdetail=4326. From a quick review it should be on all undergraduate economics courses in the spirit of pluralism in economic thinking. Some lovely quotes "The purpose of studying economics is not to acquire a set of ready-made answers to economic questions, but to learn how to avoid being deceived by economists" (Joan Robinson) and "Will raising the incomes of all increase the happiness of all? The answer to this question can now be given with somewhat greater assurance than twenty years ago...It is 'no'" (Richard Easterlin).

It also includes a series of thought-provoking 'questions for your professor' throughout; such as "Why does the textbook suppose that democracy must end at the workplace door? In whose interest is it that economic democracy remain off the agenda?' and "The competitive labour markey model predicts that if a firm reduces its wage by one cent below the equilibrium its entire workforce will quit. Why don't we test this prediction?"

The book also includes a postscript on the global financial meltdown which as they put it "illustrates the importance of imperfect and assymmetrical information, externalities, limited rationality and inappropriate incentives. In particular, it illustrates the necessity of appropriate government regulation, and the ability of powerful business interests to change the rules of the game" .

Wish I had had this textbook when I was an ungraduate!

It also includes a series of thought-provoking 'questions for your professor' throughout; such as "Why does the textbook suppose that democracy must end at the workplace door? In whose interest is it that economic democracy remain off the agenda?' and "The competitive labour markey model predicts that if a firm reduces its wage by one cent below the equilibrium its entire workforce will quit. Why don't we test this prediction?"

The book also includes a postscript on the global financial meltdown which as they put it "illustrates the importance of imperfect and assymmetrical information, externalities, limited rationality and inappropriate incentives. In particular, it illustrates the necessity of appropriate government regulation, and the ability of powerful business interests to change the rules of the game" .

Wish I had had this textbook when I was an ungraduate!

Friday, 23 July 2010

The Privatisation Board: What will it do?

Jim Stewart: The composition of the Privatisation Board, and its terms of reference, makes inevitable that the conclusions will be: privatisation of all major state Commercial State Bodies as a preferred solution; if not full privatisation, part privatisation via public/private partnership; and as a final option drastic reduction of any State subsidies as in the case of the CIE Group. Cutting subsidies to CIE was already one of the recommendation of the McCarthy/Department of Finance Report (p. 74, reduce Public Service Obligations to CIE; replace lightly used rail services with bus routes, etc.). Cutting public transport has been a particular obsession of McCarthy, who opposed Dart electrification. It is one of a few examples of proposed cuts in the Report of the Special Group on Public Service Number and Expenditure, not contained in evaluation papers published by the Department of Finance.

The same procedures used in producing the McCarthy/Department of Finance report will likely be followed in this new report. Officials in the Department of Finance will draft chapters, proposals and conclusions which will be largely accepted by the Privatisation Board.

Who is driving these policies?

These recommendations are likely to be as already described. The reason for this is that prevailing IMF views are largely held within the Department of Finance. While privatisation was not a policy recommended by the recent IMF Article IV consultation, the report in several places acknowledges IMF staff agreement with “the authorities” (not defined but referred to elsewhere as “the officials of Ireland” and also states the IMF report also states that meetings were held with senior officials from the Department of Finance, etc.). The IMF together with the World Bank helped establish privatisation as part of the Washington consensus, often with disastrous policies for developing countries. These discredited policies are now being reintroduced as conditions for IMF loans to countries with large budget deficits such as Greece.

Why privatisation is not a solution

Privatisation largely involves an exchange of ownership. The State will obtain financial assets in exchange for real assets. These financial assets could be invested in other real assets, but this is unlikely, rather Government borrowing/debt will be reduced. This exchange will be costly. Firms such as Goldman Sachs, Merrill Lynch, PricewaterhouseCoopers, Arthur Cox, etc.(all featuring in advice to the Government in relation to the banking crisis) will again be paid large fees. Apart from the cost, privatisation is no solution to Irish economic problems. The States net Balance Sheet remains the same, but the policies privatised companies may pursue will be very different. Some firms such as the ESB are natural monopolies. Regulation is key - an area where Irish agencies have a particularly poor track record. State control of monopolies can address deficiencies in regulation. What about commercial policies? Paul Sweeney has argued coherently that commercial policies of formerly State owned companies have been disastrous for Ireland’s economic success the best known is Telecom Eireann. But policies pursued by other privatised firms have added to the economic crisis for example the former ICC and ACC banks. The operations of the former Irish Sugar company (Greencore) are now focussed largely outside Ireland, and as such are unlikely to contribute to the development of agribusiness within Ireland as recently expressed in the 2020 Food Harvest Report.

In the current crisis we have been badly let down by former and current employees of the Central Bank, the financial regulator, those who designed and encouraged our gross over reliance on tax incentives, those in charge of our planning process, but in particular by institutions largely in the private sector, banks, building societies, professional firms such as auditors. Corporate governance has not been an issue in Commercial State Bodies in contrast to private sector firm such as Banks, the Quinn group, and DCC. The solution is not more economists with their misguided views on ‘efficient markets’, and ‘rational behaviour’. Banks in recent years have lost billions, competition policy as implemented by the EU Commission has lost billions more. Nor is the solution privatisation.

Arguments against privatisation are compelling. It is important that they are expressed.

The same procedures used in producing the McCarthy/Department of Finance report will likely be followed in this new report. Officials in the Department of Finance will draft chapters, proposals and conclusions which will be largely accepted by the Privatisation Board.

Who is driving these policies?

These recommendations are likely to be as already described. The reason for this is that prevailing IMF views are largely held within the Department of Finance. While privatisation was not a policy recommended by the recent IMF Article IV consultation, the report in several places acknowledges IMF staff agreement with “the authorities” (not defined but referred to elsewhere as “the officials of Ireland” and also states the IMF report also states that meetings were held with senior officials from the Department of Finance, etc.). The IMF together with the World Bank helped establish privatisation as part of the Washington consensus, often with disastrous policies for developing countries. These discredited policies are now being reintroduced as conditions for IMF loans to countries with large budget deficits such as Greece.

Why privatisation is not a solution

Privatisation largely involves an exchange of ownership. The State will obtain financial assets in exchange for real assets. These financial assets could be invested in other real assets, but this is unlikely, rather Government borrowing/debt will be reduced. This exchange will be costly. Firms such as Goldman Sachs, Merrill Lynch, PricewaterhouseCoopers, Arthur Cox, etc.(all featuring in advice to the Government in relation to the banking crisis) will again be paid large fees. Apart from the cost, privatisation is no solution to Irish economic problems. The States net Balance Sheet remains the same, but the policies privatised companies may pursue will be very different. Some firms such as the ESB are natural monopolies. Regulation is key - an area where Irish agencies have a particularly poor track record. State control of monopolies can address deficiencies in regulation. What about commercial policies? Paul Sweeney has argued coherently that commercial policies of formerly State owned companies have been disastrous for Ireland’s economic success the best known is Telecom Eireann. But policies pursued by other privatised firms have added to the economic crisis for example the former ICC and ACC banks. The operations of the former Irish Sugar company (Greencore) are now focussed largely outside Ireland, and as such are unlikely to contribute to the development of agribusiness within Ireland as recently expressed in the 2020 Food Harvest Report.

In the current crisis we have been badly let down by former and current employees of the Central Bank, the financial regulator, those who designed and encouraged our gross over reliance on tax incentives, those in charge of our planning process, but in particular by institutions largely in the private sector, banks, building societies, professional firms such as auditors. Corporate governance has not been an issue in Commercial State Bodies in contrast to private sector firm such as Banks, the Quinn group, and DCC. The solution is not more economists with their misguided views on ‘efficient markets’, and ‘rational behaviour’. Banks in recent years have lost billions, competition policy as implemented by the EU Commission has lost billions more. Nor is the solution privatisation.

Arguments against privatisation are compelling. It is important that they are expressed.

Leprechauns, fairies and Professor Fitzgerald's response

Thursday, 22 July 2010

Having a go in the dark

Michael Taft: That the Sunday Business Post has another go at public sector workers should hardly be news. Every time they mention public sector workers, whatever the context or story, they are apt to attach the rider ‘highest paid in the Europe’. Now they are doing one better with the headline ‘highest paid in the world’. Their front page story is based on data leaked from a National Competitiveness Council report (a convenient leak as discussed over at Cedar Lounge Revolution) to be published soon but, in truth, the data they use is pretty old hat. No doubt, any attempt to deconstruct the data will be ignored – it has in the past. But let’s take up the cudgels one more time and look specifically at the health sector. For any fact-based analysis shows the newspaper headlines to be wide of the mark; indeed, it shows that they are missing a real story that should be pre-occupying us.

The story is probably close to the mark when comparing high-end professionals – the consultant doctors etc.; there is some data to show they are paid above European norms. Of course, this is part of a general story – in both the private and public sector – of phenomenally high-pay at the upper ends which distorts averages. This is why Ireland compares so badly to other EU countries in wage equality statistics. So there’s not a whole lot new there.

The story goes on to quote health statistics from the OECD Health at a Glance reports which, in the words of the OECD itself, should be ‘interpreted with caution’. And for good reason. Let’s look at hospital nurses pay in the 2009 publication. First, this does not measure hourly labour costs – which is the true determiner of cost to the employer; in the case of public sector employees, the Government. Second, it doesn’t compare like with like. For instance, data sources vary from country to country (some include private sector, some include part-time, some include non-hospital staff, some omit certain grades, etc.) – reflecting a real problem in making comparisons that can stick.

Third – and this is a problem throughout OECD wage statistics – most data is compiled on the basis of taking the total amount of wages and dividing it by the total number of employees to get, as they put it, ‘the average gross annual wage’. However, this can be highly misleading. Take this comparison from the EU Klems database (which does measure hourly labour costs).

• In Ireland, annual employee compensation (including non-wage costs) was €44,800 in the whole economy in 2007. In the Netherlands, it was €37,750. On that basis you’d say – wow, we are really high paid compared to the Dutch.

• However, when hourly labour compensation is examined we find the situation reversed. In Ireland, hourly labour costs were €24.82; in Netherlands it was €28.08. What accounts for this discrepancy?

Simple: the Dutch work less hours per employee. In 2007, each Dutch employee worked, on average, 1,344 hours per year; the Irish worked 1,805. Not only is the average working week lower in the Netherlands, there is a higher level of part-time workers.

So if you compare average annual incomes you’re likely to fall into this mistake. So when the OECD puts nurses’ average annual income in 5th place among countries surveyed (including low income Greece, Mexico and the Slovak Republic), it only tells us so much.

Where the OECD methodology is more helpful is when it compares one set of workers with another set in the same economy, since the measurement is internally consistent When this is done, it shows that Irish nurses’ making the same as the Irish average wage – which puts them 15th out of 19 in terms of intra-national comparisons. In other words, in 14 countries nurses make more in relation to the average wage in their own country. On this comparison, Irish hospital nurses are not raking it in.

So is there somewhere we can go to find a robust international comparison of labour costs in the public health sector? Unfortunately, not yet; though the OECD is trying to establish an internationally agreed base-line. However, we can turn to the EU Klemsto find a story that the Sunday Business Post might wish to investigate; though I suspect if they dug too deeply it might lead them to a politically unpalatable conclusion (unpalatable for them).

Hourly labour costs in the Irish health sector were €34.57 per hour in 2007; in the Netherlands it was €25.84. This, again, might lead us to conclude that Irish public health sector workers are, indeed, costly.

But there’s an odd trend here. In 2000, Irish labour costs in this sector were €19.74; in Netherlands it was €20.51. What explains this extra-ordinary growth and turnaround? Of course, we can always put it down to greedy public sector unions, benchmarking, milking the taxpayer, etc. However, this simplistic explanation doesn’t add up.

Given that all public sector workers were covered under the same wage agreements, the same benchmarking deals, we should – according to the greedy-public-sector-worker thesis – expect to find similar increased costs in the Public Administration sector. Except in that sector (which employs a third of all pubic sector workers), nominal hourly labour costs increased by only €6.29 per hour compared to health sector costs which increased by €14.65 per hour.

How could this be? The problem with measuring labour costs in the health sector is that 45 percent of labour is in the private sector. Unfortunately, we don’t have a breakdown between public and private health sectors. But what we may be seeing is substantially increasing labour costs arising from the costly, socially perverse and economically inefficient interpenetration of the public and private in what should be a free and public good. In other words, if public sector health workers’ labour costs have increased in the same manner as other public sector workers, the issue doesn’t lie in the public realm.

It’s hard to know; and that’s the problem. Labour costs in the Public Administration sector is lower than average Eurozone costs; ditto for the Education sector. But the health sector – which is split between public and private – significantly exceeds Eurozone averages.

We do know that of those private sector health enterprises which granted wage increases in 2009, the average increase was 15 percent; for public sector health enterprises it was 7 percent. In the heart of the recession, incomes in the private health sector were rising faster than those in the public sector (though we don’t know that nurses pay was rising this fast in the private sector).

And we do know the EU/CSO shows that between 2003 and 2008 the top 10 percent households took 73 percent of the total gross PAYE income increase in the State. Not only is Ireland suffering from wage inequality, it is getting worse – and I suspect that, public or private, not too many nurses feature in the top 10 percent.

Here is a real story – costs are increasing in public services where the private sector is playing a significant role; and income is rising faster in households which have a disproportionate number of high-end professionals. The Sunday Business Post might want to investigate this further. But I will give them this warning.

They might have to conclude that we need a truly public health sector where goods are delivered, not on the ability to pay, but on need; and we might have to do something about those high incomes.

In the meantime, for want of any analysis that goes beyond dubious headlines, repeat after me: ‘Surely, gosh, we have the highest paid public workers in the whole wide world.’

The story is probably close to the mark when comparing high-end professionals – the consultant doctors etc.; there is some data to show they are paid above European norms. Of course, this is part of a general story – in both the private and public sector – of phenomenally high-pay at the upper ends which distorts averages. This is why Ireland compares so badly to other EU countries in wage equality statistics. So there’s not a whole lot new there.