Michael Burke: The Q1 real GDP figures show the economy expanding by 2.7%. No doubt these will be hailed as a turning-point, and even a vindication of policy. If only that were true.

As everyone knows, this is a twin-track or two-speed economy. Organisations such as the ESRI, OECD, IMF and EU Commission all forecast that the export sector would recover reflecting the rebound in global demand following the recession, but that the domestic economy would remain mired in recession. That's what is happening. GNP, the domestic sector of the economy contracted again in Q1 by 0.5%, for the ninth consecutive quarter, far longer than in any other Euro Area economy.

But even this is to understate the true picture. Usually, growth data is presented in real terms, so that it is real activity that is captured not just inflation. But Ireland is experiencing deflation, a generalised fall in prices. So, concentrating on the 'real' numbers means not extracting the effects of deflation. To do that, we have to go to the nominal numbers, the actual Euros produced or spent in each category of national income.

Then the picture is more accurate. Just much worse. On this measure, GDP grew by just 0.1% in Q1 (€38.752bn compared to €38.715bn in Q4 2009- that's just ¤37mn) and GNP contracted by a massive 6.8% in the quarter. Nominal GDP fell 4.4% year-on-year and is now 20.2% below its end-2007 peak. GNP fell 8.6% from a year ago and is now 27.6% below its peak. This is an Irish Depression.

If we take the components of growth the data are as follows: personal consumption is down 4.6% year-on-year, -19.6% from the peak; current govt. spending down 8.9%, -11.2% from peak, and investment remains the biggest single contributor to the slump with gross fixed capital formation falling 7.6%, -66.4% from its peak. The decline in investment actually exceeds the decline in GDP, and accounts for 93% of the decline in GNP. Exports are the only bright spot, up 3.5% from a year ago, belying the idea that the economy is uncompetitive, they are 5.1% below their peak. But the improvement in net exports is actually greater as import demand continues to decline.

Unsurprisingly, given the litany of declines in all other sectors, net exports more than accounts for the entirety of quarterly GDP growth, €2,137bn of a total improvement of just €37mn. Taken together, personal consumption, government current spending and investment fell by more than ¤2bn in the quarter. Because this is on export-only recovery and the sector is capital-intensive, dependent on imports and has ultra-low taxes, this 'recovery' will actually lead to increased joblessness, bankruptcies and a widening of the deficit. Even worse, rampant deflation will increase the real debt for all households, businesses and of course the government, making interest payments and debt repayment more burdensome from shrinking national incomes.

Wednesday, 30 June 2010

Prices and profiteering in the food sector

Michael Taft: There will be many attempts to explain the high costs of food and beverages in Ireland – a state of affairs that is hardly new. Everyone throughout the food supply chain, from the farm-gate to the retail shelf, will be blamed and will seek to lay the blame somewhere else. I’d like to highlight one aspect – profit levels in the food and beverage manufacturing sector. This is not the full explanation for high food and beverage costs; but any explanation that doesn’t factor in our extra-ordinary profit levels will be unsatisfactory.

There are three databases that refer to profit levels (or ‘gross operating surplus’ or ‘capital compensation’).

First, is the Eurostat dataset that measures gross operating surplus as percentage of turnover; in other words – how much turnover is taken as profit. The latest year we have data for this measurement is 2003. After that, Irish data is not disclosed on the grounds of ‘confidentiality’. But in that year, Irish profit levels headed the table by a long ways. Nearly a quarter of turnover was taken as profit. With the exception of the UK, profits made up less than 10 percent of turnover in other EU countries for which we have data.

The second measurement is contained in Eurostat’s European Business statistical book 2007. While this contains the same numbers as the Eurostat dataset, it provides nominal turnover and gross operating surplus numbers. From this, we can assess what would happen if Irish companies took the same amount of profit as other countries and reduced their prices accordingly.

• If Irish companies took the same amount of profit as UK companies, food and beverage prices could be reduced by 10 percent.

• If Irish companies took the same amount of profit as other non-UK EU-15 countries, food and beverage costs could be reduced by between 14 percent and 17 percent.

The third measurement comes from the EU Klems database. This has the advantage of having more current numbers – from 2007 with the ability to measure profits per employee hour worked in the Food & Beverage sector. This shows an even more dramatic gap between Ireland and the Eurozone.

Ireland is well ahead of the game, making well over four times the Eurozone average. If the profit take in Ireland were at Eurozone levels, prices could be reduced by 16 percent.

In all these measurements, however, there is a problem – the statistical distortions created by the accounting activities of multi-nationals which, through transfer-pricing, use Ireland as a tax-laundering stop-over. It is difficult, though not impossible, to assess the extent of these distortions. In the Food sector, such activities would be less than in the manufacturing sector at large. Indigenous companies make up nearly half of all turnover in this sector (as opposed to 21 percent for all industries). However, in the Food sector anyway, it is difficult to see profit levels returning to European averages even taking into account multi-national accounting activities, though I will try to follow this up in a subsequent post.

The only organisation that has considered this issue in any depth is UNITE the Union, with its publication, ‘The Truth About Irish Profits’. It took a similar approach – using European data – to assess the contribution of high profits to high prices.

This is only the manufacturing sector. A broader analysis of profit levels would have to be conducted in all elements of the food supply chain – wholesale, retail, input costs, etc. But it is clear that high, potentially inexplicably high, profit levels may be contributing to high costs.

PS: For the real devaluationists among you, labour costs can’t be blamed for high costs. Irish labour costs per hour in the Food & Beverage sector were in 2007, according to the EU Klems, 9 percent below the EU-15 average and 21 percent below our peer group (non-Mediterranean countries).

There are three databases that refer to profit levels (or ‘gross operating surplus’ or ‘capital compensation’).

First, is the Eurostat dataset that measures gross operating surplus as percentage of turnover; in other words – how much turnover is taken as profit. The latest year we have data for this measurement is 2003. After that, Irish data is not disclosed on the grounds of ‘confidentiality’. But in that year, Irish profit levels headed the table by a long ways. Nearly a quarter of turnover was taken as profit. With the exception of the UK, profits made up less than 10 percent of turnover in other EU countries for which we have data.

The second measurement is contained in Eurostat’s European Business statistical book 2007. While this contains the same numbers as the Eurostat dataset, it provides nominal turnover and gross operating surplus numbers. From this, we can assess what would happen if Irish companies took the same amount of profit as other countries and reduced their prices accordingly.

• If Irish companies took the same amount of profit as UK companies, food and beverage prices could be reduced by 10 percent.

• If Irish companies took the same amount of profit as other non-UK EU-15 countries, food and beverage costs could be reduced by between 14 percent and 17 percent.

The third measurement comes from the EU Klems database. This has the advantage of having more current numbers – from 2007 with the ability to measure profits per employee hour worked in the Food & Beverage sector. This shows an even more dramatic gap between Ireland and the Eurozone.

Ireland is well ahead of the game, making well over four times the Eurozone average. If the profit take in Ireland were at Eurozone levels, prices could be reduced by 16 percent.

In all these measurements, however, there is a problem – the statistical distortions created by the accounting activities of multi-nationals which, through transfer-pricing, use Ireland as a tax-laundering stop-over. It is difficult, though not impossible, to assess the extent of these distortions. In the Food sector, such activities would be less than in the manufacturing sector at large. Indigenous companies make up nearly half of all turnover in this sector (as opposed to 21 percent for all industries). However, in the Food sector anyway, it is difficult to see profit levels returning to European averages even taking into account multi-national accounting activities, though I will try to follow this up in a subsequent post.

The only organisation that has considered this issue in any depth is UNITE the Union, with its publication, ‘The Truth About Irish Profits’. It took a similar approach – using European data – to assess the contribution of high profits to high prices.

This is only the manufacturing sector. A broader analysis of profit levels would have to be conducted in all elements of the food supply chain – wholesale, retail, input costs, etc. But it is clear that high, potentially inexplicably high, profit levels may be contributing to high costs.

PS: For the real devaluationists among you, labour costs can’t be blamed for high costs. Irish labour costs per hour in the Food & Beverage sector were in 2007, according to the EU Klems, 9 percent below the EU-15 average and 21 percent below our peer group (non-Mediterranean countries).

Tuesday, 29 June 2010

More of the same

Michael Burke: There has been much discussion about the ESRI's view that Ireland will eventually recover to have a stronger growth rate than most other EU economies. The interest was sparked because some took it to be a vindication of government policy. But the ESRI forcasts are not exceptional; they're very much in line with those of the OECD, IMF and, in the short-run, the EU Commission.

But neither are they a vindication of government policy.

To take just one of the assessments, that of the IMF, in its recent annual assessmnent of the economy there were lots of encouraging words on policy. 'Assertive', 'credibility', 'resolve', 'appropriately ambitious fiscal consolidation' all get an airing in the first two paragraphs, so you get the picture.

But, just as you wouldn't ask Seamus Heaney for a inflation forecast, no-one ever reads the IMF publications for the beauty of their writing. It's the numbers we care about. Here is a summary of some the key numbers

* GDP falling by 0.5% this year

* A gradual rise in GDP growth to 3.5% in 2015

* Unemployment peaking at 13.5% this year

* But structural unemployment keeping the rate at 9% in 2015

There's one more shocking number to come, but let's deal with these first. The recession here began at the start of 2008, for the Euro Area as a whole it began one year later. The Euro Area began to recover in mid-2009 while all the official foreasts have the economy here contracting again in the first half of this year. Therefore the Irish recession will be precisely two-and-a-half years long, compared to 6 months for the Euro Area as a whole.

The forecast increase in GDP growth to 3.5% provides little cause for celebration. The last time this economy had a lower growth rate than that was in 1993, recovering from the strait-jacket of the European Exchange Rate Mechanism and an overvalued punt. In addtion, as all the forecasts agree, the recovery will be a statistical one only as net exports pick-up on the back of rising global demand (but, incidentally, nailing the nonsense about 'lack of competitiveness').

But, since the export sector relies heavily on foreign imports, because it is not especially labour-intensive and, above all, because it is so lowly-taxed, none of this statistical improvement will be reflected in domestic ativity or create jobs (or narrow the deficit). So, shockingly, unemployment is still expected to be 9% in 2015. And although the IMF does not state it, given that employment prospects are so poor, the declining unemployment rate must arise overwhelmingly from continued mass emigration.

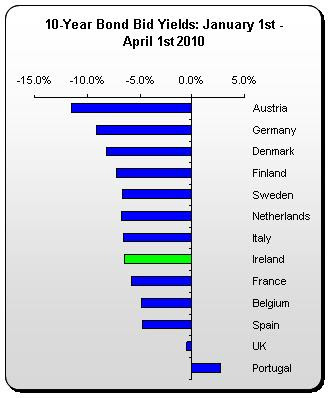

This might be of little concern to the IMF, which states that "[Government] actions have reassured the global policy community and international financial markets." We won't dwell on the fact that Irish 10yr government bond yields were 5.6% yesterday, having started the crisis at 4.1%, nor that most other yields have fallen since that time. But at least the 'global policy community' is reassured, by which the IMF means, well, the IMF and others.

Yet the only other number of significance is the most shocking of all. The IMF arguments that prior measures are on a track 'leading towards' deficit-reduction. But not on the track itself, as they argue for further fiscal consolidation measures equivalent to 4.5% of GDP. And, if growth is not as robust as the government foecasts 'a clear possibility' the IMF says, the measures will need to be even larger.

To put this in context, the €3bn in further measures the government is talking about is 1.8% of GDP, on top of the 2008 ad 2009 budgets, emergency budget and measures which amounted to 8.9% of GDP. So, rather than the government's €3bn measures, the IMF reckons they should be at least €7.35bn, probably more. That's at least half the fiscal tightening already seen to date.

It is to repeat a fiscal tightening which led to wider, not norrower deficits (7.3% of GDP to 14.3%),and the longest, deepest recession in the Euro Area, as well as a surge in both unemployment and emigration. Repeating the same experiment and expecting a different outcome is madness.

But neither are they a vindication of government policy.

To take just one of the assessments, that of the IMF, in its recent annual assessmnent of the economy there were lots of encouraging words on policy. 'Assertive', 'credibility', 'resolve', 'appropriately ambitious fiscal consolidation' all get an airing in the first two paragraphs, so you get the picture.

But, just as you wouldn't ask Seamus Heaney for a inflation forecast, no-one ever reads the IMF publications for the beauty of their writing. It's the numbers we care about. Here is a summary of some the key numbers

* GDP falling by 0.5% this year

* A gradual rise in GDP growth to 3.5% in 2015

* Unemployment peaking at 13.5% this year

* But structural unemployment keeping the rate at 9% in 2015

There's one more shocking number to come, but let's deal with these first. The recession here began at the start of 2008, for the Euro Area as a whole it began one year later. The Euro Area began to recover in mid-2009 while all the official foreasts have the economy here contracting again in the first half of this year. Therefore the Irish recession will be precisely two-and-a-half years long, compared to 6 months for the Euro Area as a whole.

The forecast increase in GDP growth to 3.5% provides little cause for celebration. The last time this economy had a lower growth rate than that was in 1993, recovering from the strait-jacket of the European Exchange Rate Mechanism and an overvalued punt. In addtion, as all the forecasts agree, the recovery will be a statistical one only as net exports pick-up on the back of rising global demand (but, incidentally, nailing the nonsense about 'lack of competitiveness').

But, since the export sector relies heavily on foreign imports, because it is not especially labour-intensive and, above all, because it is so lowly-taxed, none of this statistical improvement will be reflected in domestic ativity or create jobs (or narrow the deficit). So, shockingly, unemployment is still expected to be 9% in 2015. And although the IMF does not state it, given that employment prospects are so poor, the declining unemployment rate must arise overwhelmingly from continued mass emigration.

This might be of little concern to the IMF, which states that "[Government] actions have reassured the global policy community and international financial markets." We won't dwell on the fact that Irish 10yr government bond yields were 5.6% yesterday, having started the crisis at 4.1%, nor that most other yields have fallen since that time. But at least the 'global policy community' is reassured, by which the IMF means, well, the IMF and others.

Yet the only other number of significance is the most shocking of all. The IMF arguments that prior measures are on a track 'leading towards' deficit-reduction. But not on the track itself, as they argue for further fiscal consolidation measures equivalent to 4.5% of GDP. And, if growth is not as robust as the government foecasts 'a clear possibility' the IMF says, the measures will need to be even larger.

To put this in context, the €3bn in further measures the government is talking about is 1.8% of GDP, on top of the 2008 ad 2009 budgets, emergency budget and measures which amounted to 8.9% of GDP. So, rather than the government's €3bn measures, the IMF reckons they should be at least €7.35bn, probably more. That's at least half the fiscal tightening already seen to date.

It is to repeat a fiscal tightening which led to wider, not norrower deficits (7.3% of GDP to 14.3%),and the longest, deepest recession in the Euro Area, as well as a surge in both unemployment and emigration. Repeating the same experiment and expecting a different outcome is madness.

Monday, 28 June 2010

There's got to be someone to blame

Slí Eile: The Department of Finance has come in for increased criticism and attention in recent times. Periodically, Eddie Molloy has written about the failings of that Department (see for example his latest article in the Irish Times here).

Typically, the following assumptions and assertions are made:

1 The Department of Finance has lacked economist skills and specialisms

2 The Department lacks expertise in relation to banking

3 The Department is excessively deferential to politicians

4 The Department doesn't like to be criticised

5 The Department is not accountable in the same way that other bodies are.

Each of these assumptions (or assertions) has a ring of truth. But, is that the whole story?

Employ more economists in Merrion Street?

If more economists were drafted in to Finance in the last 10-15 years would this have made any fundamental difference to the fiscal and other policy outcomes? Methinks not. Some clue to the answer lies in what was being said or not said by ESRI, the media and financial market economists and, last but not least, academic economists (the only true economists around according to academic economists). It should be borne in mind that many civil servants with an economics degree and some research training either fled the ship for greener pastures elsewhere (for the impoverished private sector) or aspired to a generalist career where specialisms can be a liability. If only Merrion Street were packed with PhD economists? With the greatest of respect to economists I would not have many of them deciding on levels of public service, taxation and investment going by what some of them were saying then and now.

The Department of Finance completed, itself, a review in 2009. It got little attention. You can read it here. It was bland. for example, it said (page 24):

Overall, the view was that economics, policy analysis and appraisal skills are available in the Department, and will continue to be required. However, it was suggested that Taxation, Governance, Regulatory Impact Analysis, HR and Employment Law skills needed to be built up to meet future challenges. There was a view that specialist technical skills, such as Legal and Drafting Skills could be “bought in” as necessary. This would be to address particular tasks, for example legislative requirements, or to deal with periodic demands for technical skills

Expertise in banking?

Clearly many officials did not have a grasp of financial reality in the summer and early Autumn of 2008. It was knee-jerk time following a predictable cycle of, first denial, second disbelief, third panic, fourth blanket guarantees and the rest is history (nationalisation, recapitalisation and black holes). Guarantee everything from deposits to bonds in haste and regret at leisure as the saying goes about lifelong commitments. If Finance lacked banking expertise it is not obvious that the experts from the banking world would have advised or acted differently. Even those academic economists caught in the glare of the September 2008 crisis had 40 different opinions about what to do over banking (easier to agree that NAMA is wrong; harder to defined exactly what can and should be done exactly both then and now).

Yes Minister?

Clearly a feature of civil service cultures the world over is deference (or obsequiousness) to the Minister of the day. A strength of the Service, here, is the degree to which it is independent of the political and offers a vital resource and continuity as Governments change over the decades. Still, one cannot avoid the impression that civil servants tasked with advising and then implementing the decisions of politicians could have been clearer and more courageous about contesting various received wisdoms including the costly and idiotic 'de-centralisation' scheme beloved of some local chambers of commerce or the drive to cut capital gains tax, income taxes etc

Thou shall not criticise?

Nobody likes to admit that they got it wrong or that they have a part in the current social and economic malaise. Is there a risk that people can put up straw men: Seánie, Fingleton, the Central Bank, the Department of Finance, the Public Service Unions, the Church, the British, the European Union, your parents, your children. In reality, it seems to me that we are just have an exceptionally wicked and severe bout of economic slump. That's global capitalism for you. The fact that it is being prolonged at global level by deflationary strategies (and in the case of Ireland made worse due to bad decisions in the past as well as present) means that we need to balance domestic self-flagellation against the financial and political hurricanes that continue to sweep the world (with the divine Markets in foul mood like the deities of old).

Accountable?

Who is accountable? The Oireacthas has very limited powers to initiate, call to account and to rectify. The Committee system plays a constructive role but the Government parties call the shots when it comes to follow-through.

The real danger of moving public ire to just one Government Department is that we can miss the more fundamental point about public service in a democracy.

Public service should be renewed and viewed as a calling and vocation to serve the public (common) good. Whether the service involves nursing, policing, teaching, administering or regulating it has been viewed as something undertaken under trust and within a framework of accountability, ultimately, to the Oireachtas where expenditures and legal provision apply.

It is clear that there have been individual as well as systemic failures within the broad public service. At best, these failures relate to lack of planning, lack of openness and lack of transparency. At worst, these failures reflect a marked lack of responsibility in regulation and proactive response to clear societal risks. In a few cases, corruption has been present (e.g. in regard to land re-zoning and bribing of public officials). It is regrettable that these failures have been used by some commentators to sully the image and reputation of the entire public service. Assertions, unsubstantiated by data or evidence, have been made about a service that is bloated, inefficient, sclerotic and incompetent.

The 2008 review by the OECD of the Irish public service paints a different picture. It suggests a service that is relatively smaller than in other countries and one that has managed to deliver significant success over the decades. Nevertheless, the Irish public service needs to be reformed and practices, culture and working approaches need to change. This is more than just an attempt to import business planning and customer service speak into public service delivery. It is, also, more than a mere opening up of competition for various posts in the system which has thrived for too long on time served and restrictive practices in regard to promotion and recruitment.

One of the first principles of public service reform should be a return to the idea of public service as a noble calling to serve the common good. Idealism, leadership and service to the public good must inform service delivery and policy design. For too long, managerialism, pragmatism and excessive deference to the political establishment has held back the public service from offering more independent and provocative advice as well as assuming greater responsibility and accountability where individuals and teams are held responsible to implement a project within a given timeframe.

Public service reform needs to involve a cultural shift away from secrecy, top-down control and detached decision-making. Bringing about change is never easy. The introduction of legislation such as Freedom of Information and Ethics in Public Office along with Equality legislation in the 1990s involved contestation.

The Labour Party has already stated it support for:

* greater mobility of staff within the public sector;

* full flexibility of movement between all branches of the public and civil service for relevant grades (where there has been much talk but no delivery to date); and

* Open recruitment to all public service posts (not universal in many cases)

With the follow-up to the OECD Review published in 2008 on Irish public service reform, change is happening at snail's pace and it very much 'top down' rather than led from the ranks.

Paradoxically, the imposition of 'control and command', more than ever, in regard to every single post subject to the public service moratorium allied to micro-management form the centre of relatively small grant payment runs counter to the spirit of the OECD report which advocated more delegation of responsibility and authority to decide on resource allocation allied to 'working within budgets' and being called to account for outcomes and delivery rather than micro-management of input and process. The system does not seem to learn or apply the lessons of past failed initiatives from the 1960s Devlin Report onwards.

Typically, the following assumptions and assertions are made:

1 The Department of Finance has lacked economist skills and specialisms

2 The Department lacks expertise in relation to banking

3 The Department is excessively deferential to politicians

4 The Department doesn't like to be criticised

5 The Department is not accountable in the same way that other bodies are.

Each of these assumptions (or assertions) has a ring of truth. But, is that the whole story?

Employ more economists in Merrion Street?

If more economists were drafted in to Finance in the last 10-15 years would this have made any fundamental difference to the fiscal and other policy outcomes? Methinks not. Some clue to the answer lies in what was being said or not said by ESRI, the media and financial market economists and, last but not least, academic economists (the only true economists around according to academic economists). It should be borne in mind that many civil servants with an economics degree and some research training either fled the ship for greener pastures elsewhere (for the impoverished private sector) or aspired to a generalist career where specialisms can be a liability. If only Merrion Street were packed with PhD economists? With the greatest of respect to economists I would not have many of them deciding on levels of public service, taxation and investment going by what some of them were saying then and now.

The Department of Finance completed, itself, a review in 2009. It got little attention. You can read it here. It was bland. for example, it said (page 24):

Overall, the view was that economics, policy analysis and appraisal skills are available in the Department, and will continue to be required. However, it was suggested that Taxation, Governance, Regulatory Impact Analysis, HR and Employment Law skills needed to be built up to meet future challenges. There was a view that specialist technical skills, such as Legal and Drafting Skills could be “bought in” as necessary. This would be to address particular tasks, for example legislative requirements, or to deal with periodic demands for technical skills

Expertise in banking?

Clearly many officials did not have a grasp of financial reality in the summer and early Autumn of 2008. It was knee-jerk time following a predictable cycle of, first denial, second disbelief, third panic, fourth blanket guarantees and the rest is history (nationalisation, recapitalisation and black holes). Guarantee everything from deposits to bonds in haste and regret at leisure as the saying goes about lifelong commitments. If Finance lacked banking expertise it is not obvious that the experts from the banking world would have advised or acted differently. Even those academic economists caught in the glare of the September 2008 crisis had 40 different opinions about what to do over banking (easier to agree that NAMA is wrong; harder to defined exactly what can and should be done exactly both then and now).

Yes Minister?

Clearly a feature of civil service cultures the world over is deference (or obsequiousness) to the Minister of the day. A strength of the Service, here, is the degree to which it is independent of the political and offers a vital resource and continuity as Governments change over the decades. Still, one cannot avoid the impression that civil servants tasked with advising and then implementing the decisions of politicians could have been clearer and more courageous about contesting various received wisdoms including the costly and idiotic 'de-centralisation' scheme beloved of some local chambers of commerce or the drive to cut capital gains tax, income taxes etc

Thou shall not criticise?

Nobody likes to admit that they got it wrong or that they have a part in the current social and economic malaise. Is there a risk that people can put up straw men: Seánie, Fingleton, the Central Bank, the Department of Finance, the Public Service Unions, the Church, the British, the European Union, your parents, your children. In reality, it seems to me that we are just have an exceptionally wicked and severe bout of economic slump. That's global capitalism for you. The fact that it is being prolonged at global level by deflationary strategies (and in the case of Ireland made worse due to bad decisions in the past as well as present) means that we need to balance domestic self-flagellation against the financial and political hurricanes that continue to sweep the world (with the divine Markets in foul mood like the deities of old).

Accountable?

Who is accountable? The Oireacthas has very limited powers to initiate, call to account and to rectify. The Committee system plays a constructive role but the Government parties call the shots when it comes to follow-through.

The real danger of moving public ire to just one Government Department is that we can miss the more fundamental point about public service in a democracy.

Public service should be renewed and viewed as a calling and vocation to serve the public (common) good. Whether the service involves nursing, policing, teaching, administering or regulating it has been viewed as something undertaken under trust and within a framework of accountability, ultimately, to the Oireachtas where expenditures and legal provision apply.

It is clear that there have been individual as well as systemic failures within the broad public service. At best, these failures relate to lack of planning, lack of openness and lack of transparency. At worst, these failures reflect a marked lack of responsibility in regulation and proactive response to clear societal risks. In a few cases, corruption has been present (e.g. in regard to land re-zoning and bribing of public officials). It is regrettable that these failures have been used by some commentators to sully the image and reputation of the entire public service. Assertions, unsubstantiated by data or evidence, have been made about a service that is bloated, inefficient, sclerotic and incompetent.

The 2008 review by the OECD of the Irish public service paints a different picture. It suggests a service that is relatively smaller than in other countries and one that has managed to deliver significant success over the decades. Nevertheless, the Irish public service needs to be reformed and practices, culture and working approaches need to change. This is more than just an attempt to import business planning and customer service speak into public service delivery. It is, also, more than a mere opening up of competition for various posts in the system which has thrived for too long on time served and restrictive practices in regard to promotion and recruitment.

One of the first principles of public service reform should be a return to the idea of public service as a noble calling to serve the common good. Idealism, leadership and service to the public good must inform service delivery and policy design. For too long, managerialism, pragmatism and excessive deference to the political establishment has held back the public service from offering more independent and provocative advice as well as assuming greater responsibility and accountability where individuals and teams are held responsible to implement a project within a given timeframe.

Public service reform needs to involve a cultural shift away from secrecy, top-down control and detached decision-making. Bringing about change is never easy. The introduction of legislation such as Freedom of Information and Ethics in Public Office along with Equality legislation in the 1990s involved contestation.

The Labour Party has already stated it support for:

* greater mobility of staff within the public sector;

* full flexibility of movement between all branches of the public and civil service for relevant grades (where there has been much talk but no delivery to date); and

* Open recruitment to all public service posts (not universal in many cases)

With the follow-up to the OECD Review published in 2008 on Irish public service reform, change is happening at snail's pace and it very much 'top down' rather than led from the ranks.

Paradoxically, the imposition of 'control and command', more than ever, in regard to every single post subject to the public service moratorium allied to micro-management form the centre of relatively small grant payment runs counter to the spirit of the OECD report which advocated more delegation of responsibility and authority to decide on resource allocation allied to 'working within budgets' and being called to account for outcomes and delivery rather than micro-management of input and process. The system does not seem to learn or apply the lessons of past failed initiatives from the 1960s Devlin Report onwards.

The Black Dog

Paul Krugman in the NYT yesterday thinks the non-event at Toronto has condemned us to a depression, only the third in the history of capitalism, and he blames it on wrong-headed government policies.

It’s almost as if the financial markets understand what policy makers seemingly don’t: that while long-term fiscal responsibility is important, slashing spending in the midst of a depression, which deepens that depression and paves the way for deflation, is actually self-defeating...

And who will pay the price for this triumph of orthodoxy? The answer is, tens of millions of unemployed workers, many of whom will go jobless for years, and some of whom will never work again.

Thursday, 24 June 2010

Thinking outside the box on stage

Slí Eile: Who said that the Dismal Science is not sometimes dismal? David McWilliams is providing a highly enjoyable, informative, provocative and controversial performance, currently, at the Peacock. If you have a chance to see it, go ! See here.

The thrust of this fast-moving and incisive stand-up comedy is that the crisis we face is more that of (Irish) cronyism than (world) capitalism. He draws on TASC work extensively on (and acknowledges) Mapping the Golden Circle.

The key message is that the ‘Insiders’ have it sown up and NAMA is one massive ‘Class Rescue Plan’ for bankers, corporate borrowers, lawyers, brokers and the professional classes. McWilliams posits that there are two groups:

The Insiders – found in every village, town and city – are those with a stake in our country who believe that today’s status quo must be preserved at all costs.

The Outsiders – who might live next door – are those who realise that the status quo is part of the problem.

In populist mode, he suggests that Government cannot take on the ‘Insiders’ ‘on the left’ in the public service trade unions standing in the way with restrictive work practices without at the same time taking on the Insiders ‘on the right’ (in banks and corporations and firms benefiting from the NAMA bail-out). The Outsiders include the negative equity people who are stuck here or the vulnerable young or the unemployed some of whom are/will be force to emigrate.

In a gripping performance that lasts an amazing non-stop 100 minutes one’s mood changes from hilarious laughter against an unfolding comic tragedy to shock and anger to, finally, reflection on how we might get out of this mess. His rallying cry is:

A Stop bailing out Anglo-Irish and let them go to the wall

B Pursue competitive devaluation through break up in the Eurozone (he seems to see this as inevitable anyway)

C Invest in new innovative product and service lines internationally (the Jack Charlton Plan to rally the diaspora).

I would not quibble with A and C above. Few would have advocated B or seen it as a realistic option up to 6 months. Who is to know now? Contrarians should not be dismissed lightly especially when they got it largely right before. I don’t think that advocating a break up in the Eurozone is a wise strategy right now for Ireland. The point is to invest in new skills and jobs by targeted expansion in Ireland’s low-tax and low-spend public sphere. The problem about debt – as McWilliams shows – is mainly about corporate and banking debt which has been ‘nationalised’ in the past months so that we the taxpayers and welfare recipients pay the bill and cover the risk.

In the final moments of the show, McWilliams calls for a return to capitalism and an end to cryonyism (or what others have referred to as socialism for bankers). Others might prefer to call for a better regulated capitalism and a more humane one founded on welfare and re-distributional policies. Still others like Michael Moore in his stand-up comedy Capitalism a Love Story says that 'Capitalism is an evil, and you cannot regulate evil….You have to eliminate it and replace it with something that is good for all people and that something is democracy.'

I am with Moore on that crucial point.

The thrust of this fast-moving and incisive stand-up comedy is that the crisis we face is more that of (Irish) cronyism than (world) capitalism. He draws on TASC work extensively on (and acknowledges) Mapping the Golden Circle.

The key message is that the ‘Insiders’ have it sown up and NAMA is one massive ‘Class Rescue Plan’ for bankers, corporate borrowers, lawyers, brokers and the professional classes. McWilliams posits that there are two groups:

The Insiders – found in every village, town and city – are those with a stake in our country who believe that today’s status quo must be preserved at all costs.

The Outsiders – who might live next door – are those who realise that the status quo is part of the problem.

In populist mode, he suggests that Government cannot take on the ‘Insiders’ ‘on the left’ in the public service trade unions standing in the way with restrictive work practices without at the same time taking on the Insiders ‘on the right’ (in banks and corporations and firms benefiting from the NAMA bail-out). The Outsiders include the negative equity people who are stuck here or the vulnerable young or the unemployed some of whom are/will be force to emigrate.

In a gripping performance that lasts an amazing non-stop 100 minutes one’s mood changes from hilarious laughter against an unfolding comic tragedy to shock and anger to, finally, reflection on how we might get out of this mess. His rallying cry is:

A Stop bailing out Anglo-Irish and let them go to the wall

B Pursue competitive devaluation through break up in the Eurozone (he seems to see this as inevitable anyway)

C Invest in new innovative product and service lines internationally (the Jack Charlton Plan to rally the diaspora).

I would not quibble with A and C above. Few would have advocated B or seen it as a realistic option up to 6 months. Who is to know now? Contrarians should not be dismissed lightly especially when they got it largely right before. I don’t think that advocating a break up in the Eurozone is a wise strategy right now for Ireland. The point is to invest in new skills and jobs by targeted expansion in Ireland’s low-tax and low-spend public sphere. The problem about debt – as McWilliams shows – is mainly about corporate and banking debt which has been ‘nationalised’ in the past months so that we the taxpayers and welfare recipients pay the bill and cover the risk.

In the final moments of the show, McWilliams calls for a return to capitalism and an end to cryonyism (or what others have referred to as socialism for bankers). Others might prefer to call for a better regulated capitalism and a more humane one founded on welfare and re-distributional policies. Still others like Michael Moore in his stand-up comedy Capitalism a Love Story says that 'Capitalism is an evil, and you cannot regulate evil….You have to eliminate it and replace it with something that is good for all people and that something is democracy.'

I am with Moore on that crucial point.

Tuesday, 22 June 2010

Portable Mortgages

Nat O'Connor: Two contradictory pieces in the news about mortgages. On the one hand, it was reported that some lenders are preparing to offer 'negative equity' mortgages of up to 125 per cent (Irish Independent). However the Central Bank proposes to restrict how much customers can borrow (Irish Examiner article and Irish Independent take on same story). Presumably, the new lending rules will make negative equity mortgages difficult, if not possible. Yet, do we want people 'trapped' in their homes, when job opportunities or other circumstances might require them to move?

An example of the negative equity mortgage goes as follows: John buys a house for €300,000 with a mortgage for €250,000. However the current market price of his house is only €200,000. Hence he is in 'negative equity'. Let's say John wants to move and has located another house priced at €200,000 that he wants to buy. Normally the bank won't permit him to sell, as his original mortgage is secured on his first house. However, the 'negative equity mortgage' is a loan of €250,000 to buy the house for €200,000. In other words, John ends up in the same position of negative equity but gets to move to a new house.

The negative equity mortgage could be a good thing, if it allows John to move to where there are job opportunities or if it allows him to move closer to his social networks. Currently, renting is not going to cover the mortgage, so it's not a viable option. Hence, John is either stuck in his first house or he needs to sell it.

But there are risks. The first risk is that house prices may continue to fall. But that's not a major problem as that would affect John in his first house anyway. The worst scenario would be if John bought a new property for €200,000 that was more over-priced than his current house, but it's really John's responsibility to shop around and get advice.

The second risk is that John will incur extra costs in moving that will weaken his ability to pay his mortgage. Stamp duty is the main cost there. Brian Cowen recently strongly defended his decision to not cut stamp duty, but it is a significant barrier to labour mobility. (Aside: Mr Cowen argues that the tax dampened property prices and speculation. It may have deterred quick buy-and-sell of property, but it seems likely that much of the pricing of houses was designed to recover the cost of stamp duty; so stamp duty may actually have boosted price inflation rather than dampened it. At any rate, it might be phased out in favour of property tax. The sooner the better).

Another cost is that John might lose first time buyer's mortgage interest relief (if applicable to his first house). And moving house inevitably costs money (from movers to legal fees), but then again John has to compare his income in the first house and his income in the second. If a job opportunity beckons, it might be worth the cost. Of course, there are many other factors in the cost-benefit analysis. The new house might be closer to friends or family, or to schools, or whatever.

A third possible risk is that people would seek a negative equity mortgage as a way of gaining access to cash. In our example, that might involve John seeking to borrow €275,000. This could be to pay the stamp duty or it could be to get cash for doing up the new house. In any case, there is a risk that adding to his mortgage debt could be the final straw and bring about an inability to pay.

Despite the above risks, it seems likely that there are some scenarios where something like the negative equity mortgage would be a good thing. If the proposed central bank regulations do not permit this to occur, then maybe some other options need to be considered. For example, in other countries mortgages can be portable. The legal detail is different, but it would work the same way as the above scenario. John would simply move his existing mortgage and secure it against the new house. He'd buy the house for €200,000 and still owe his bank €250,000.

Portable mortgages would also prevent a situation where people 'top up' their mortgage and take on extra debt. It would also benefit those who have mortgages without negative equity. Overall it would be a way of getting movement in the property market. Hopefully the Central Bank's rush to control risk will not elimate the possibility of innovative solutions to the housing crisis that could allow people to continue to make choices to improve their own situations.

An example of the negative equity mortgage goes as follows: John buys a house for €300,000 with a mortgage for €250,000. However the current market price of his house is only €200,000. Hence he is in 'negative equity'. Let's say John wants to move and has located another house priced at €200,000 that he wants to buy. Normally the bank won't permit him to sell, as his original mortgage is secured on his first house. However, the 'negative equity mortgage' is a loan of €250,000 to buy the house for €200,000. In other words, John ends up in the same position of negative equity but gets to move to a new house.

The negative equity mortgage could be a good thing, if it allows John to move to where there are job opportunities or if it allows him to move closer to his social networks. Currently, renting is not going to cover the mortgage, so it's not a viable option. Hence, John is either stuck in his first house or he needs to sell it.

But there are risks. The first risk is that house prices may continue to fall. But that's not a major problem as that would affect John in his first house anyway. The worst scenario would be if John bought a new property for €200,000 that was more over-priced than his current house, but it's really John's responsibility to shop around and get advice.

The second risk is that John will incur extra costs in moving that will weaken his ability to pay his mortgage. Stamp duty is the main cost there. Brian Cowen recently strongly defended his decision to not cut stamp duty, but it is a significant barrier to labour mobility. (Aside: Mr Cowen argues that the tax dampened property prices and speculation. It may have deterred quick buy-and-sell of property, but it seems likely that much of the pricing of houses was designed to recover the cost of stamp duty; so stamp duty may actually have boosted price inflation rather than dampened it. At any rate, it might be phased out in favour of property tax. The sooner the better).

Another cost is that John might lose first time buyer's mortgage interest relief (if applicable to his first house). And moving house inevitably costs money (from movers to legal fees), but then again John has to compare his income in the first house and his income in the second. If a job opportunity beckons, it might be worth the cost. Of course, there are many other factors in the cost-benefit analysis. The new house might be closer to friends or family, or to schools, or whatever.

A third possible risk is that people would seek a negative equity mortgage as a way of gaining access to cash. In our example, that might involve John seeking to borrow €275,000. This could be to pay the stamp duty or it could be to get cash for doing up the new house. In any case, there is a risk that adding to his mortgage debt could be the final straw and bring about an inability to pay.

Despite the above risks, it seems likely that there are some scenarios where something like the negative equity mortgage would be a good thing. If the proposed central bank regulations do not permit this to occur, then maybe some other options need to be considered. For example, in other countries mortgages can be portable. The legal detail is different, but it would work the same way as the above scenario. John would simply move his existing mortgage and secure it against the new house. He'd buy the house for €200,000 and still owe his bank €250,000.

Portable mortgages would also prevent a situation where people 'top up' their mortgage and take on extra debt. It would also benefit those who have mortgages without negative equity. Overall it would be a way of getting movement in the property market. Hopefully the Central Bank's rush to control risk will not elimate the possibility of innovative solutions to the housing crisis that could allow people to continue to make choices to improve their own situations.

Monday, 21 June 2010

City 44

Nat O'Connor In its 2008 Index of Global Cities, Foreign Policy ranked Dublin 44 out of the top 60 'global' cities on the planet (specific article here, subscribers only). The world map and index diagram can be seen here.

The premise is that "The world's biggest, most interconnected cities help set global agendas, weather transnational dangers, and serve as the hubs of global integration. They are the engines of growth for their countries and the gateways to the resources of their regions." In this context, "The cities that host the biggest capital markets, elite universities, most diverse and well-educated populations, wealthiest multinationals, and most powerful international organizations are connected to the rest of the world like nowhere else."

I'm interested in the "engines of growth" idea and also in the changing role of cities and city-regions vis-à-vis nation states in the world economy. To add to Michael Taft's post on urgent priorities, a focus on the specific policy required to develop Dublin can possibly complement the generic approaches needed to boost the whole Irish economy. In this context, I think the Dublin Development Plan is important and likewise, an elected mayor for Dublin could have an important role in the long-term, if given sufficient powers.

To put the rank of 44th into context, Dublin is not even ranked in the largest 600 world cities in 2010 by http://www.citymayors.com/. Clearly, cities in China and India dominate the list, but a total of 43 EU cities are in the top 600 world's largest cities (Dublin is 49th in size, according to citymayor.com's data). However, in the Foreign Policy listing, Dublin is the 14th highest EU city. So it is worth digging into our ranking to see what 'good things' are helping us compete above our size.

The Global Cities Index ranks cities according to 24 metrics across five dimensions: business activity; human capital; information exchange; cultural experience; and global political engagement. The latter two measures go beyond economics and illustrate that other factors, like quality of life and engagement in world affairs, matter for success.

Dublin ranks (out of 60) as follows:

41st for business activity

39th for human capital

48th for information exchange

30th for cultural experience

48th for political engagement

The Foreign Policy article suggests that global cities can play different roles, depending on their strengths and weaknesses. As such, it is not just about Dublin being 'more global', but about finding a niche for Dublin among the cities of the world. And the choices made about Dublin's development will help or limit the econoimc opportunities the rest of Ireland can seek in the global economy. What follows is my guess on the kind of factors Dublin scored well on and some thoughts on how we might develop our strengths and weaknesses in order to support the development of the whole Irish economy.

Business activity (41/60): Foreign Policy defines business activity as the value of a city's capital markets, the number of Fortune Global 500 firms headquartered there, and the volume of the goods that pass through the city.

I guess the IFSC model positioned Ireland well in terms of business activity, with Dublin providing access to financial markets and the offices of many global firms. Obviously, the global financial system is in a mess. Moreover, TASC has highlighted that many of the tax avoidance aspects of the IFSC are unsustainable, if not counter-productive. Hence there is a need to ensure a sustainable and useful direction for the IFSC model. In the past, there was talk of converting the IFSC into a centre for global carbon credit trading. Professor Ray Kinsella (UCD) recently spoke at TASC's stimulus seminar about his long-standing ideas for an International Medical Service Centre, along a similar model, tapping the knowledge and interests of the pharmaceutical industries already investing here. I think the IFSC probably does need a new direction and/or a replacement as an engine for growth. That will require a broad consensus and strong Government leadership to create something big that is also sustainable.

Human capital (39/60): This includes how well the city acts as a magnet for diverse groups of people and talent, the size of a city's immigrant population, the number of international schools, and the percentage of residents with university degrees.

In this context, emigration (including the exodus of recent EU imigrants) is not helping Ireland. As ever, people with degrees are also likely to be among the most mobile, which lowers the education profile of the remaining population. Initiatives like DCU's collaboration agreement with Indian universities shows an awareness of the global market, and last week's conference, Re-Inventing the University, is part of the conversation we need about how ideas fuel economic activity and provides some ideas for moving beyond the clichés about the 'knowledge economy' and formulating what role we want universities to play.

Information exchange (48/60): This is how well news and information is dispersed about and to the rest of the world. The number of international news bureaus, the amount of international news in the leading local papers, and the number of broadband subscribers.

This is one of Dublin's weaker rankings. Luckily they are only measuring broadband access in Dublin, not the rest of the country or it would be worse. Also, the fact that British media is readily available in Dublin may compensate for the relative weakness of national titles, and RTÉ, to covering global affairs. There is a valuable role the Irish media could take in cultivating a broader public interest in consuming news about the rest of the world. This could also put some of our economic problems and policy dilemmas into perspective, as well as provide an alternative English langugage analysis to the dominant voices in Anglo-American news reporting.

Cultural experience (30/60): The level of diverse attractions for international residents and travelers. That includes everything from how many major sporting events a city hosts to the number of performing arts venues it boasts.

Dublin's strongest rank was for cultural experience. In other words, Dublin is a relatively nice place to live. This illustrates the importance of culture in the economy. Cutbacks to sports and the arts - and even the visible deterioration of public space through closed shops and businesses - will impinge on future development opportunities. There is wisdom in the advice to paint the shop during a downturn; we should be looking at cost-neutral ways of making Dublin a great place to live, in lots of little ways, so that the next major international employer has more reasons to prefer Dublin to other cities in the EU. I think the city councils have been consciously doing this, with such things as DublinBikes, farmers' markets, festivals, etc. But cutbacks are likely to fall heavily on the staff who provide the 'soft' and intangible services at local authority level. There is a need to treat these things as part of Dublin's core offering, not as nice optional extras. This is one area where powers and budgets could be quickly transfered from central government to the elected Dublin mayor.

Political engagement (48/60): The degree to which a city influences global policymaking and dialogue. This was measured by examining the number of embassies and consulates, major think tanks, international organizations, sister city relationships, and political conferences a city hosts.

I imagine the new national conference centre has been identified as an asset for the international market, but overall this is a weaker area for Dublin. Ireland hosts many NGOs working in developing countries. As an example, this could be built on, positioning Dublin as a centre for expertise in development. Universities could be encouraged to supply appropriate degrees. Another example is that when Sweden closed its embassy there was concern in the news, possibly because of the fear that Dublin would lose out on positive externalities if a lot of EU countries closed their embassies here. It remains to be seen if the EU can function well enough to replace the need for each member-state to have representation in the other 26 countries. This would probably require a much larger EU office in Dublin to replace the embassies, but that could be something small countries like Ireland encourage the EU to develop.

Overall then, if the Dublin city-region is an engine for Ireland's future economic development, then perhaps looking at the characteristics of a successful global city can help shape policy in a more productive direction than deflation and bust. Dublin in 2008 had major competitive advantages compared to other EU cities. Now is the time to consolidate remaining advantages and build more of them.

The premise is that "The world's biggest, most interconnected cities help set global agendas, weather transnational dangers, and serve as the hubs of global integration. They are the engines of growth for their countries and the gateways to the resources of their regions." In this context, "The cities that host the biggest capital markets, elite universities, most diverse and well-educated populations, wealthiest multinationals, and most powerful international organizations are connected to the rest of the world like nowhere else."

I'm interested in the "engines of growth" idea and also in the changing role of cities and city-regions vis-à-vis nation states in the world economy. To add to Michael Taft's post on urgent priorities, a focus on the specific policy required to develop Dublin can possibly complement the generic approaches needed to boost the whole Irish economy. In this context, I think the Dublin Development Plan is important and likewise, an elected mayor for Dublin could have an important role in the long-term, if given sufficient powers.

To put the rank of 44th into context, Dublin is not even ranked in the largest 600 world cities in 2010 by http://www.citymayors.com/. Clearly, cities in China and India dominate the list, but a total of 43 EU cities are in the top 600 world's largest cities (Dublin is 49th in size, according to citymayor.com's data). However, in the Foreign Policy listing, Dublin is the 14th highest EU city. So it is worth digging into our ranking to see what 'good things' are helping us compete above our size.

The Global Cities Index ranks cities according to 24 metrics across five dimensions: business activity; human capital; information exchange; cultural experience; and global political engagement. The latter two measures go beyond economics and illustrate that other factors, like quality of life and engagement in world affairs, matter for success.

Dublin ranks (out of 60) as follows:

41st for business activity

39th for human capital

48th for information exchange

30th for cultural experience

48th for political engagement

The Foreign Policy article suggests that global cities can play different roles, depending on their strengths and weaknesses. As such, it is not just about Dublin being 'more global', but about finding a niche for Dublin among the cities of the world. And the choices made about Dublin's development will help or limit the econoimc opportunities the rest of Ireland can seek in the global economy. What follows is my guess on the kind of factors Dublin scored well on and some thoughts on how we might develop our strengths and weaknesses in order to support the development of the whole Irish economy.

Business activity (41/60): Foreign Policy defines business activity as the value of a city's capital markets, the number of Fortune Global 500 firms headquartered there, and the volume of the goods that pass through the city.

I guess the IFSC model positioned Ireland well in terms of business activity, with Dublin providing access to financial markets and the offices of many global firms. Obviously, the global financial system is in a mess. Moreover, TASC has highlighted that many of the tax avoidance aspects of the IFSC are unsustainable, if not counter-productive. Hence there is a need to ensure a sustainable and useful direction for the IFSC model. In the past, there was talk of converting the IFSC into a centre for global carbon credit trading. Professor Ray Kinsella (UCD) recently spoke at TASC's stimulus seminar about his long-standing ideas for an International Medical Service Centre, along a similar model, tapping the knowledge and interests of the pharmaceutical industries already investing here. I think the IFSC probably does need a new direction and/or a replacement as an engine for growth. That will require a broad consensus and strong Government leadership to create something big that is also sustainable.

Human capital (39/60): This includes how well the city acts as a magnet for diverse groups of people and talent, the size of a city's immigrant population, the number of international schools, and the percentage of residents with university degrees.

In this context, emigration (including the exodus of recent EU imigrants) is not helping Ireland. As ever, people with degrees are also likely to be among the most mobile, which lowers the education profile of the remaining population. Initiatives like DCU's collaboration agreement with Indian universities shows an awareness of the global market, and last week's conference, Re-Inventing the University, is part of the conversation we need about how ideas fuel economic activity and provides some ideas for moving beyond the clichés about the 'knowledge economy' and formulating what role we want universities to play.

Information exchange (48/60): This is how well news and information is dispersed about and to the rest of the world. The number of international news bureaus, the amount of international news in the leading local papers, and the number of broadband subscribers.

This is one of Dublin's weaker rankings. Luckily they are only measuring broadband access in Dublin, not the rest of the country or it would be worse. Also, the fact that British media is readily available in Dublin may compensate for the relative weakness of national titles, and RTÉ, to covering global affairs. There is a valuable role the Irish media could take in cultivating a broader public interest in consuming news about the rest of the world. This could also put some of our economic problems and policy dilemmas into perspective, as well as provide an alternative English langugage analysis to the dominant voices in Anglo-American news reporting.

Cultural experience (30/60): The level of diverse attractions for international residents and travelers. That includes everything from how many major sporting events a city hosts to the number of performing arts venues it boasts.

Dublin's strongest rank was for cultural experience. In other words, Dublin is a relatively nice place to live. This illustrates the importance of culture in the economy. Cutbacks to sports and the arts - and even the visible deterioration of public space through closed shops and businesses - will impinge on future development opportunities. There is wisdom in the advice to paint the shop during a downturn; we should be looking at cost-neutral ways of making Dublin a great place to live, in lots of little ways, so that the next major international employer has more reasons to prefer Dublin to other cities in the EU. I think the city councils have been consciously doing this, with such things as DublinBikes, farmers' markets, festivals, etc. But cutbacks are likely to fall heavily on the staff who provide the 'soft' and intangible services at local authority level. There is a need to treat these things as part of Dublin's core offering, not as nice optional extras. This is one area where powers and budgets could be quickly transfered from central government to the elected Dublin mayor.

Political engagement (48/60): The degree to which a city influences global policymaking and dialogue. This was measured by examining the number of embassies and consulates, major think tanks, international organizations, sister city relationships, and political conferences a city hosts.

I imagine the new national conference centre has been identified as an asset for the international market, but overall this is a weaker area for Dublin. Ireland hosts many NGOs working in developing countries. As an example, this could be built on, positioning Dublin as a centre for expertise in development. Universities could be encouraged to supply appropriate degrees. Another example is that when Sweden closed its embassy there was concern in the news, possibly because of the fear that Dublin would lose out on positive externalities if a lot of EU countries closed their embassies here. It remains to be seen if the EU can function well enough to replace the need for each member-state to have representation in the other 26 countries. This would probably require a much larger EU office in Dublin to replace the embassies, but that could be something small countries like Ireland encourage the EU to develop.

Overall then, if the Dublin city-region is an engine for Ireland's future economic development, then perhaps looking at the characteristics of a successful global city can help shape policy in a more productive direction than deflation and bust. Dublin in 2008 had major competitive advantages compared to other EU cities. Now is the time to consolidate remaining advantages and build more of them.

The urgent priorities

Michael Taft: Professor Ray Kinsella, a leading light in common sense economics, put it this way on Saturday View:

‘The economic strategy upon which the state is embarked upon is counter-productive and will not work . . . We face another series of budgets that are bleeding demand from the economy . . . Our priorities have been to shore up banks that have been at the epicentre of this crisis; to stabilise the public finances; and, at some distance, to support families and businesses. We have it the wrong way around. We should be engaged in hand-to-hand fighting to support every business in the country with joined up thinking. We should support families. That in itself should stabilise the public finances . . . We have much less time to do all this than we think. Europe is in crisis. Greece has been downgraded to junk status. Portugal and Spain are in big trouble. The stabilisation fund that was announced last May has not been bought by the financial markets. We are in big trouble in Europe and unless we get our act sorted out here together. . we will have run out of track.’

Out of track; progressives should heed this warning. There is an urgency to unite around a common analysis and a common set of demands. For let’s be honest: to date, progressives have been all over the place. Some accept the fiscal conservatism of the orthodoxy, some argue for tax-driven consolidation, some accept spending cuts, some call for traditional stimulus measures, some urge long-term investment measures; there is no common thread running through any of this.

Added to this, with some exceptions, is the aspirational nature of many of our demands. To call for jobs or any other kind of stimulus without stipulating exactly what this means; to call for stimulus while at the same time acquiescing to the Government’s fiscal parameters (that is, fiscal contraction); to call for all manner of good things without specifying where we are going to source the money: why should anyone take us seriously?

Progressives must break from what is, in many respects, our own self-imposed irrelevancy. Therefore, I put forward the following three principles around which it might be possible to build a broad alliance for a new economic departure. These are only principles – not an entire programme. But starting points are crucial to mapping our way of this morass.

1. Stop Digging an Even Deeper Hole

The Government’s fiscal consolidation policies are failing. Cutting spending during a recession is irrational and self-defeating. The only way to a balanced budget is through increasing income. And the only way to do this is to increase investment and employment levels. Full stop. Anything that undermines growth, investment and job creation is only adding to our long-term debt. Full stop.

Therefore, a key demand coming into the autumn and the budget debate is that there should be no real cuts in current public spending. Cutting spending has been an economic disaster at every level – driving down output, consumption and employment. First rule when you’re in a hole: stop digging.

This is not the same as saying unproductive spending shouldn’t be cut; it should be (though those who claim there is billions of wasteful spending rarely give examples). Cut unproductive spending if it can be found and re-direct it into productive spending; this is money we won’t have to borrow – see below. But most of all – stop digging.

2. Investment, Investment, Investment

Economic investment has been cut to shreds. Overall investment is, in nominal terms, back to 1999 levels. Now, the Government intends to cut public investment by over 20 percent in real terms by 2014. There’s one word for this: madness.

Investment will have to be either supplied by the state or directed by it. Waiting for private sector investment to find its way into productive economy could be a long, long wait. As Davy pointed out, during the period of easy money, investment (save for the public sector) was mostly blown on housing or unproductive activities. Now that money’s tight, what chance of this changing?

But if we argue for more investment where should it go? What are the projects or areas that will (a) add to our productive capacity and (b) get people back to work? What are the investment priorities that we would need to make in any event, regardless of the fiscal crisis? Here are some concrete, specific proposals to start that debate:

• Fine Gael’s NewERA proposals: the expansion of, and establishment of new, public enterprises to drive infrastructural investment

• Green New Deals: Labour, ICTU and Comhar have all forward proposals under this heading.

• IBEC’s Capital Investment proposals: the employers’ body has provided a detailed list capital projects to raise out productivity and economic efficiency.

• Human Capital: Sinn Fein’s ‘GI Bill-type’ proposal could help integrate the various bodies, agencies and programmes into a comprehensive investment programme into human capital.

• Adelaide Hospital Society’s Universal Health Care: increasing output and equity for the same price as we spend on our two-tier health service – now that’s real reform

• Children and Families: public networks of early childhood education, childcare and wrap-around or full-service schools would boost knowledge capital and employ thousands (though the real returns would be long-term).

As many of these would have a long-lead in time from inception to implementation to return, we need temporary measures to get an immediate bang for our buck. There are a number of shovel-ready capital projects – particularly at the local authority level – that should be immediately financed. These would constitute interim measures.

The above list shows the range of proposals already being advanced to boost growth and employment. There are more. Professor Kinsella’s proposed specialist science and technology bank is an example of positive forward thinking. Tom O’Connor’s updated Telesis approach to indigenous tech-companies is another. We will need to model, cost and prioritise these – striking a balance between long-term productivity gains and short-term employment boost. But the point here is that there are a considerable number of job-creation proposals – let’s move on them.

3. Where’s the Money? Here’s the Money

How do we get our hands on the investment to get these output, productivity and employment-raising activities going? The Government’s deflationary strategy has ended in tears in the international markets (our 10-year spreads vie with Portugal to be the worst in the EU-14). Resort to international borrowing, possible at the start of the recession, is now being closed off.

There are five areas we can identify for investment resources:

Public enterprise: they have the ability to leverage investment for commercial return projects. Take Next Generation Broadband: IBEC estimates the cost of a network to be €2.2 billion with a 12-year ROI time horizon. A model outlined by Donal Palcic shows how a public enterprise-private investment partnership can work. And rather than costing the state, it would be a beneficiary in the short-term as two-thirds of the cost is made up in civil engineering work (more tax revenue, reduced unemployment costs). And afterwards, we have a real revenue-raising asset in place.

Use our Savings: The ESRI estimates we will have nearly €50 billion (or nearly 40 percent of our GNP) by next year in Exchequer cash balances and Pension Reserve Fund assets. Not all of this can or should be accessed (billions are tied up in bank recapitalisation while we need to retain liquidity on our balance sheet). Still, can it be argued that we need this entire savings at a time when our economy desperately needs investment capital? Put some of it to work, boost output and, so, reduce long-term debt.

Redirect Pension Fund Contributions: The Government intends to put nearly €4 billion into the Pension Fund between 2012 and 2014. Redirect some, most, all of that into investment now. It doesn’t alter the Exchequer Balance Sheet output, but it will boost inputs (e.g. tax revenue, reduced unemployment costs) meaning lower debt.

Taxation: The ESRI has shown that taxation is less harmful to the economy than spending cuts. Raise taxation, particularly on the ‘savers’ (that is, high-income groups); this will have the least deflationary impact. Some of this money can be diverted into productive investment.

Public Sector Productivity Gains: if there are efficiencies to be had in the public sector (and not the Government’s Transformation Agenda which is just a cover for cutting public services, employment and working conditions), then redirect those savings into investment.

These are five areas in which we can start to access the resources for investment without the Exchequer resorting to the international markets. I’m sure others have more ideas. And with growth comes more resources for investment through increased revenue. This is how we get a virtuous cycle happening.

* * *

This is an outline, that’s all. We could add more policy points. For instance, we need to bury the 2014 Maastricht guideline target. No on believes we can reach it, so why base policy on a fantasy? The Ernst & Young / Oxford Economics report suggests that on current trends (and even with healthy GDP growth) we won’t bring the deficit into Maastricht compliance until 2018 or 2019. While this might be pessimistic, what it urgently shows is that we must get the process right. If we do that, the date will come right. If we don’t get the process right, target dates are meaningless.