Michael Taft: Even before the election has been officially announced, the debate has gotten off to a fairly dismal start. Yesterday, Labour’s Eamon Gilmore made the simple proposition that the target date for Maastricht compliance should be postponed until 2016. The reaction from Fianna Fail and Fine Gael has been extreme. You’d think Labour was proposing the end of capitalism as we know it.

Let’s get a grip on the real world. The IMF released an analysis of the Government’s four-year plan last December and assessed its potential to repair public finances. They found that by 2014, the deficit would be -5.1 percent of GDP (the Government is aiming for -2.8 percent). By 2015, it won’t be a whole lot better. The rate of deficit reduction slows to -4.8 percent. If this rate holds in subsequent years, Maastricht compliance won’t be achieved even by the end of the decade.

This shouldn’t be too surprising. The ESRI signalled that under a low-growth scenario, the deficit would still be below the Maastricht guideline by the end of decade.

So all Labour is acknowledging is what everyone knows (though only a few will say so publicly).

Why is this happening? Because the weight of the austerity programme is crushing growth. The IMF projects average annual growth up to 2014 to be 2.1 percent compared to the Government’s 2.8 percent. This lower growth projection will result in stubbornly high unemployment – estimated to be 11 percent in 2015 by the IMF. This burden, along with sluggish income growth, undermines the targets in the Government’s four-year plan.

John McHale refers to this in a thoughtful article in the Sunday Business Post. He posits three conditions to achieving debt stabilisation and regaining market confidence. First, a credible deficit-reduction plan; second, assurance that there are no additional losses on our banks’ balance sheets, and third, that nominal GDP growth ‘evolve broadly in line envisioned in recent IMF, ESRI and government forecasts’.

Regarding the first, we don’t have such a plan (austerity, as we have seen in the past two years, only deflates income and growth, but not debt); regarding the second – the markets continue to be wary and only the most stringent tests will assure them. Regarding the third point, however, we have a problem as the IMF, ESRI and government forecasts are telling us different things. Here are the latest nominal growth projections over the next two years:

Government: 6.8 percent

ESRI: 4.2 percent

IMF: 4.0 percent

EU: 4.0 percent

The IMF and EU project that nominal GDP growth will be 40 percent less than what the Government is hoping for. The ESRI’s projection isn’t a whole lot better.

But when it comes to GNP – the driver of most tax revenue and, therefore, the key to deficit reduction - the gap between the forecasts widen considerably.

Government: 5.6 percent

EU: 1.2 percent

ESRI: 0.8 percent

IMF: 0.5 percent

Now we can see why both the EU and IMF projections show the Government’s four-year plan will fail. Anaemic growth and high unemployment is a sure-fire recipe for high deficits and rising debt.

So when Labour calls for the Maastricht target deadline be postponed until 2016, all they are doing is taking a realistic account of the actually existing economy. Indeed, under current policy that deadline won’t be reached even by then.

If the argument centres on deadlines then it will be a dismal debate. Instead, what we need is a debate over a substantial and sustained investment drive (the only means to create sustainable growth that will translate into deficit-reduction) and alternatives to austerity measures.

That debate has yet to start in earnest.

Monday, 31 January 2011

Banking crisis looms

An Saoi: Last Friday's Irish Independent had a story suggesting that the Credit Union movement is skeptical about the value of the Government's Bank guarantee to depositors. Back in January 2009, the Registrar of Credit Unions wrote a letter to all Credit Unions advising in relation to surplus funds:

“In the current financial environment, priority should be given to the holding of surplus funds in short term deposit accounts in credit institutions where the amount deposited is statutorily guaranteed. Where commercial considerations clearly justify longer term deposits, these should only be considered where there is no undue risk to members’ savings. However, such investments should be the subject of detailed analysis and careful consideration by the full board, having regard to the future liquidity requirements of your credit union.”

In effect, Mr. Logue, the Registrar, told Credit Unions to place or keep over €3,000M on deposit in the Irish Banks, which would not have happened using any rational analysis – why would you risk placing all your spare cash on deposit in failing financial institutions that needed a State guarantee to stay open?

In a piece I did last week, see here, I commented on household deposits. It now seems a major group of commercial depositors also wish to withdraw their cash from the beleaguered Irish banks. Tuesday 1st February will see the publication of the December banking statistics by the Central Bank, which are likely to show further falls in deposits. It now appears that despite NAMA, all the money from the State & National Pension Fund that has gone into the banks to date and finally the next tranche to be poured into the black hole via the EU/IMF deal, no one trusts the Irish banking system. A banking crisis looms and will be the first of many such crises to face the incoming Government. Squeaky bum time!

“In the current financial environment, priority should be given to the holding of surplus funds in short term deposit accounts in credit institutions where the amount deposited is statutorily guaranteed. Where commercial considerations clearly justify longer term deposits, these should only be considered where there is no undue risk to members’ savings. However, such investments should be the subject of detailed analysis and careful consideration by the full board, having regard to the future liquidity requirements of your credit union.”

In effect, Mr. Logue, the Registrar, told Credit Unions to place or keep over €3,000M on deposit in the Irish Banks, which would not have happened using any rational analysis – why would you risk placing all your spare cash on deposit in failing financial institutions that needed a State guarantee to stay open?

In a piece I did last week, see here, I commented on household deposits. It now seems a major group of commercial depositors also wish to withdraw their cash from the beleaguered Irish banks. Tuesday 1st February will see the publication of the December banking statistics by the Central Bank, which are likely to show further falls in deposits. It now appears that despite NAMA, all the money from the State & National Pension Fund that has gone into the banks to date and finally the next tranche to be poured into the black hole via the EU/IMF deal, no one trusts the Irish banking system. A banking crisis looms and will be the first of many such crises to face the incoming Government. Squeaky bum time!

Friday, 28 January 2011

The Finance Bill and Davos - different discourses

Sinéad Pentony: The Finance Bill will bring the measures announced as part of Budget 2011 into law in the coming days. As the effects of these measures begin to be felt by families, business and the wider economy, it is worth restating the impact they will have, and comparing the Irish solutions to the crisis, to what is happening over at the World Economic Forum in Davos.

Budget 2011 measures represent a €6 billion adjustment that will reduce incomes at all levels through changes in taxation (€2.1 billion), with a disproportionate impact on low paid workers. Spending cuts on public services and social transfers (€2.2 billion) will see a further erosion of public services and push more people into poverty, while the capital spending budget cut ( €1.75 billion) will have a direct impact on our competitiveness and economic growth.

Cumulatively, the extreme austerity measures will result in:

• even more demand being taken out of a weak and fragile economy;

• businesses being put under increasing pressure as they struggle to remain viable;

• the jobs crisis continuing and the rate of emigration gathering pace;

• growing inequality - as more families and vulnerable groups are pushed into poverty because they no longer have an adequate income to meet their basic needs.

The absence of an investment strategy to stimulate growth and demand will make it increasingly difficult to address the deficit. The passing of the Finance Bill into law represents more of the same failed policy choices, and they will not address the fiscal and economic crises.

Meanwhile, over in Davos, the World Economic Forum is having its annual gathering of international business leaders, politicians, intellectuals and journalists to discuss the most pressing issues facing the world. The Forum is not normally associated with ‘progressive’ ideas but over the last number of days they have been talking about inequality, jobless growth and youth unemployment, amongst other things, as they grapple with finding solutions to the global financial, economic and fiscal crises.

Fears over jobless recovery and youth unemployment have prompted joint actions between the trade unions and Davos leaders to develop a coherent plan for G20 nations. Job creation coupled with the need to address the issue of growing income and wealth inequalities have been put forward as key parts of the solution. Some of the suggestions include the need to increase the wage share of national income; the creation of a universal safety net to protect workers who lose their jobs; and active labour market policies to create work, amongst others. Action is also needed to ensure the proceeds of growth are distributed more equally and concentrations of wealth are eliminated.

The passing of the Finance Bill into law will copperfasten measures that will do the exact opposite of the solutions being discussed in Davos. Ireland seems to be determined to cut its own idiosyncratic path.

The reduction in social transfer levels and the minimum wage will create a more unequal distribution of wealth, while the absence of any major job initiatives means the most promising job path for Ireland’s unemployed will continue to be the airline ticket out of the country.

Budget 2011 measures represent a €6 billion adjustment that will reduce incomes at all levels through changes in taxation (€2.1 billion), with a disproportionate impact on low paid workers. Spending cuts on public services and social transfers (€2.2 billion) will see a further erosion of public services and push more people into poverty, while the capital spending budget cut ( €1.75 billion) will have a direct impact on our competitiveness and economic growth.

Cumulatively, the extreme austerity measures will result in:

• even more demand being taken out of a weak and fragile economy;

• businesses being put under increasing pressure as they struggle to remain viable;

• the jobs crisis continuing and the rate of emigration gathering pace;

• growing inequality - as more families and vulnerable groups are pushed into poverty because they no longer have an adequate income to meet their basic needs.

The absence of an investment strategy to stimulate growth and demand will make it increasingly difficult to address the deficit. The passing of the Finance Bill into law represents more of the same failed policy choices, and they will not address the fiscal and economic crises.

Meanwhile, over in Davos, the World Economic Forum is having its annual gathering of international business leaders, politicians, intellectuals and journalists to discuss the most pressing issues facing the world. The Forum is not normally associated with ‘progressive’ ideas but over the last number of days they have been talking about inequality, jobless growth and youth unemployment, amongst other things, as they grapple with finding solutions to the global financial, economic and fiscal crises.

Fears over jobless recovery and youth unemployment have prompted joint actions between the trade unions and Davos leaders to develop a coherent plan for G20 nations. Job creation coupled with the need to address the issue of growing income and wealth inequalities have been put forward as key parts of the solution. Some of the suggestions include the need to increase the wage share of national income; the creation of a universal safety net to protect workers who lose their jobs; and active labour market policies to create work, amongst others. Action is also needed to ensure the proceeds of growth are distributed more equally and concentrations of wealth are eliminated.

The passing of the Finance Bill into law will copperfasten measures that will do the exact opposite of the solutions being discussed in Davos. Ireland seems to be determined to cut its own idiosyncratic path.

The reduction in social transfer levels and the minimum wage will create a more unequal distribution of wealth, while the absence of any major job initiatives means the most promising job path for Ireland’s unemployed will continue to be the airline ticket out of the country.

Thursday, 27 January 2011

Roubini and Rogoff call for haircuts

Tom McDonnell: Two internationally renowned economists, Ken Rogoff (a former chief economist of the IMF and Harvard Professor) and Nouriel Roubini of NYU and the National Bureau of Economic Research, have called on Ireland to impose burden sharing on the senior unsecured bondholders.

They say that failure to do so risks plunging Ireland into insolvency. Rogoff also predicts thatm on its current ‘Ceausescu like’ austerity path, Ireland may have to restructure the sovereign debt.

Ken Rogoff is the author of ‘This Time is Different: Eight Centuries of Financial Folly’. Nouriel Roubini is the author of ‘Crisis Economics: A Crash Course in the Future of Finance’.

They say that failure to do so risks plunging Ireland into insolvency. Rogoff also predicts thatm on its current ‘Ceausescu like’ austerity path, Ireland may have to restructure the sovereign debt.

Ken Rogoff is the author of ‘This Time is Different: Eight Centuries of Financial Folly’. Nouriel Roubini is the author of ‘Crisis Economics: A Crash Course in the Future of Finance’.

Wednesday, 26 January 2011

Not just for Section 23: Economic analysis and the Budget

Tom McDonnell: There has been much commentary in the last week about the Government’s decision to roll back on its commitment to end the Section 23 property tax breaks. The Government has instead committed to an economic analysis of the impact of ending the tax breaks. Although TASC called for the abolition of these reliefs in its pre- Budget submission, economic analysis of budgetary measures is in many ways a welcome development.

The larger issue here is the continuing failure to undertake economic analyses of all budgetary measures. For example, an announcement pointing to a forthcoming econometric analysis of the impact of €6 billion in austerity measures is glaringly conspicuous by its absence. The absence of serious analysis was a causal factor in the economic crash, and it would be criminally negligent not to learn from past mistakes.

At least six months before each annual budget, the Government of the day should produce a long list of the measures it is considering for the forthcoming budget. Each of these measures should then be subjected to a full cost-benefit analysis by independent economists. Opposition parties should have their own opportunity to submit proposals for analysis. The cost-benefit analysis should seek to quantify the impact of the proposal across a variety of indicators. Sample indicators include (but are not limited to) the impact on:

• Economic growth (short and long-term)

• Employment

• The exchequer borrowing requirement

• Economic equality, for example which groups will gain and which groups will lose

• The at risk of poverty rate and other poverty related indicators

• Quality of life indicators, for example health outcomes

• Aggregate stock and composition of productive physical capacity

• Aggregate stock and composition of human capital

• The national innovative capacity

• The environment

The results of each of the cost-benefit analyses should then be independently peer-reviewed and submitted to the Government two months in advance of the budget. Existing policies, for example tax expenditures, should be subjected to regular ex post analysis. All policy measures should be reviewed twelve months after implementation, and then again every two or three years.

In the run-up to the budget the Government’s chosen set of budget proposals should be submitted to an independent Fiscal Council, set up for the express purpose of ensuring the parameters of the budget are counter-cyclical and consistent with the principle of macroeconomic sustainability.

The Government of the day should also seek to ensure that the principle of multi-annual budgeting becomes standard practice. The publication of multi-annual budgetary frameworks, of the type outlined in the National Recovery Plan, need to become semi-annual events.

None of this in any way precludes or infringes on political or economic debate. Political parties will have different positions on the relative importance of the various indicators and these differences will lead to divergent policy choices.

Impact analysis will improve accountability and transparency in budgetary decisions and will make it more difficult for interest groups to lobby Governments to sneak through legislation that benefits their narrow sectional interest at the expense of the wider society.

An indicative timetable might look like this:

January to March: Passing of Finance Bill through the Dáil

April: Publication of ‘Four Year Budgetary Framework’

June: Publication of Long list of budget proposals

June-October: Cost benefit analyses of the long list

October: Publication of ‘Updated Four year Budgetary Framework’

November: Parameters of the current year’s proposed budget audited by independent fiscal council and findings published

December: Budget

The fiscal council should be a purely advisory body, entirely independent from political parties and from powerful vested interests. For example, this would automatically exclude all economists working in the financial sector (or, indeed, for other sectional interests). Lobbying a member of the fiscal council should be made illegal. Ideally, the head of the fiscal council should be an economist of international renown.

The larger issue here is the continuing failure to undertake economic analyses of all budgetary measures. For example, an announcement pointing to a forthcoming econometric analysis of the impact of €6 billion in austerity measures is glaringly conspicuous by its absence. The absence of serious analysis was a causal factor in the economic crash, and it would be criminally negligent not to learn from past mistakes.

At least six months before each annual budget, the Government of the day should produce a long list of the measures it is considering for the forthcoming budget. Each of these measures should then be subjected to a full cost-benefit analysis by independent economists. Opposition parties should have their own opportunity to submit proposals for analysis. The cost-benefit analysis should seek to quantify the impact of the proposal across a variety of indicators. Sample indicators include (but are not limited to) the impact on:

• Economic growth (short and long-term)

• Employment

• The exchequer borrowing requirement

• Economic equality, for example which groups will gain and which groups will lose

• The at risk of poverty rate and other poverty related indicators

• Quality of life indicators, for example health outcomes

• Aggregate stock and composition of productive physical capacity

• Aggregate stock and composition of human capital

• The national innovative capacity

• The environment

The results of each of the cost-benefit analyses should then be independently peer-reviewed and submitted to the Government two months in advance of the budget. Existing policies, for example tax expenditures, should be subjected to regular ex post analysis. All policy measures should be reviewed twelve months after implementation, and then again every two or three years.

In the run-up to the budget the Government’s chosen set of budget proposals should be submitted to an independent Fiscal Council, set up for the express purpose of ensuring the parameters of the budget are counter-cyclical and consistent with the principle of macroeconomic sustainability.

The Government of the day should also seek to ensure that the principle of multi-annual budgeting becomes standard practice. The publication of multi-annual budgetary frameworks, of the type outlined in the National Recovery Plan, need to become semi-annual events.

None of this in any way precludes or infringes on political or economic debate. Political parties will have different positions on the relative importance of the various indicators and these differences will lead to divergent policy choices.

Impact analysis will improve accountability and transparency in budgetary decisions and will make it more difficult for interest groups to lobby Governments to sneak through legislation that benefits their narrow sectional interest at the expense of the wider society.

An indicative timetable might look like this:

January to March: Passing of Finance Bill through the Dáil

April: Publication of ‘Four Year Budgetary Framework’

June: Publication of Long list of budget proposals

June-October: Cost benefit analyses of the long list

October: Publication of ‘Updated Four year Budgetary Framework’

November: Parameters of the current year’s proposed budget audited by independent fiscal council and findings published

December: Budget

The fiscal council should be a purely advisory body, entirely independent from political parties and from powerful vested interests. For example, this would automatically exclude all economists working in the financial sector (or, indeed, for other sectional interests). Lobbying a member of the fiscal council should be made illegal. Ideally, the head of the fiscal council should be an economist of international renown.

A new emergency Budget

Michael Taft: Whatever about the disputes over facilitating the passage of the Finance Bill, what people want to know is what parties are going to do about it when they get into office. And this is where progressives can stop feuding with each other and get the debate back to where it belongs – showing how Budget 2011 will do such harm to economic recovery and fiscal stability. And, more importantly, what can be done to remove that harm and show how a progressive platform will bring immediate benefit to the economy and living standards.

Here’s one way of doing that: a precondition for entering government should be the enactment of an emergency budget within 60 days based on three concrete pledges:

• Repeal the Universal Social Charge

• Immediately release funds for public investment

• Reverse the cuts in social welfare income and the minimum wage

Let’s go through these three pledges.

Pledge 1: Repeal the Universal Social Charge

The Universal Social Charge (USC) should be repealed and the previous tax regime – the Income Levy and Health Contribution Levy – should be reinstated. This has no budgetary implications as it would be, per Government estimates, fiscally neutral. But the benefit to households and the economy would be considerable:

As seen, low-income earners could benefit by up to €10 per week while higher income groups would lose out. This would help economic growth – low-income earners spend their additional income; high-income earners tend to save.

This platform could be developed. For instance, the Health Contribution Levy, while marinating its former thresholds, could be integrated into the Income Levy which has a more progressive base (e.g. rents and dividends are exempt from the Health Levy). Therefore, abolishing USC could actually be a revenue raising measure.

In addition, further progressive tax measures could be introduced alongside repealing the USC. The Community Platform, TASC, ICTU and other civil society organisations – all have put forward practical and easily implemented proposals in the areas of tax expenditures and extension of levies to capital income.

The total impact of this would be to increase tax revenue further while providing a small stimulus to low-average income households in the form of removing deflationary tax increases.

Pledge 2: Immediately Release Funds for Public Investment

The second pledge would be to immediately release €2 billion for investment – to come from a combination of the Pension Fund and Exchequer cash balances (we still have nearly €30 billion in liquid assets). This would be done in tandem with re-opening negotiations with the IMF/EU to ring-fence our cash and assets for investment/fiscal consolidation purposes.

To ensure it gets on-stream as quickly as possible, this investment would be largely pumped into ‘shovel-ready’ projects at central and local government (a good start would be refurbish every school to best standard in time for autumn classes).

However, we can go beyond ‘bricks and mortars’ – as UNITE has shown: modern information systems, preventative health initiatives, one-on-one tutoring to raise literacy and numeracy skills (both in schools and in the community), loan guarantee schemes for SMEs, etc.

The economy would not get a full year benefit from this increased investment. But let’s assume 50 percent of the total multiplier gets into the economy by year’s end (it will continue to benefit the economy for an additional 5 and a half years):

• 10,000 jobs created directly with an additional 3,000 to 4,000 spin-off jobs

• Reduction in unemployment and related costs

• An additional €350 million in tax revenue

• A GDP boost of 0.75 percent

A big impetus – which would take some time to get off the ground – would be an announcement that a public enterprise company will be established to build a Next Generation Broadband network to reach every household and business by 2015. While publicly-directed and owned, private investment can be leveraged in. This would be a clear signal of intent: that we are going to invest our way to economic recovery and fiscal stability.

Pledge 3: Reverse the cuts in social welfare income and the minimum wage

A pledge to reverse the cuts in social welfare income and the minimum wage should also be non-negotiable. This measure would boost demand and GDP, increase business turnover, protect retail employment and raise tax revenue (e.g. VAT, etc.). Therefore, it would end up costing the Exchequer far less than the headline cost of repealing the social welfare cuts (€397 million) while the reversing the minimum wage will actually boost Exchequer revenue.

There are other measures – minimal in cost but capable of lifting inequitable burdens on those on low incomes while increasing demand:

• Repealing the GMS co-payments – not likely to cost much after administrative savings are taken into account

• Protect all minimum wages – namely, no cut in pay rates and working conditions under Joint Labour Committees

• Increase Family Income Supplement by the amount as in Budget 2010 - €6 per child per week: this will enhance living standards of thousands of low and average income families with children.

Any increase on the public expenditure side would be more than compensated by tax measure introduced on high income groups (under Pledge 1), tax revenue from investment activity (under Pledge 2), and the benefit of higher demand that increasing people’s living standards would produce (under Pledge 3).

Its win-win-win.

* * *

This simple three-point programme does not address all the economic and social issues which progressive parties will have to address in their election manifestos, never mind when they are in government.

However, it would give a short, sharp signal to the electorate about progressive values and priorities. It will show people how people will be better off after 60 days of a progressive government. It will give everyone a clear picture of the medium-term direction of the new government.

And it will give something for progressive to agree over, instead of attacking each other. Such feuding only brings the prospect that more of the same failed economic thinking will dominate in the next government.

And who wants that?

Here’s one way of doing that: a precondition for entering government should be the enactment of an emergency budget within 60 days based on three concrete pledges:

• Repeal the Universal Social Charge

• Immediately release funds for public investment

• Reverse the cuts in social welfare income and the minimum wage

Let’s go through these three pledges.

Pledge 1: Repeal the Universal Social Charge

The Universal Social Charge (USC) should be repealed and the previous tax regime – the Income Levy and Health Contribution Levy – should be reinstated. This has no budgetary implications as it would be, per Government estimates, fiscally neutral. But the benefit to households and the economy would be considerable:

As seen, low-income earners could benefit by up to €10 per week while higher income groups would lose out. This would help economic growth – low-income earners spend their additional income; high-income earners tend to save.

This platform could be developed. For instance, the Health Contribution Levy, while marinating its former thresholds, could be integrated into the Income Levy which has a more progressive base (e.g. rents and dividends are exempt from the Health Levy). Therefore, abolishing USC could actually be a revenue raising measure.

In addition, further progressive tax measures could be introduced alongside repealing the USC. The Community Platform, TASC, ICTU and other civil society organisations – all have put forward practical and easily implemented proposals in the areas of tax expenditures and extension of levies to capital income.

The total impact of this would be to increase tax revenue further while providing a small stimulus to low-average income households in the form of removing deflationary tax increases.

Pledge 2: Immediately Release Funds for Public Investment

The second pledge would be to immediately release €2 billion for investment – to come from a combination of the Pension Fund and Exchequer cash balances (we still have nearly €30 billion in liquid assets). This would be done in tandem with re-opening negotiations with the IMF/EU to ring-fence our cash and assets for investment/fiscal consolidation purposes.

To ensure it gets on-stream as quickly as possible, this investment would be largely pumped into ‘shovel-ready’ projects at central and local government (a good start would be refurbish every school to best standard in time for autumn classes).

However, we can go beyond ‘bricks and mortars’ – as UNITE has shown: modern information systems, preventative health initiatives, one-on-one tutoring to raise literacy and numeracy skills (both in schools and in the community), loan guarantee schemes for SMEs, etc.

The economy would not get a full year benefit from this increased investment. But let’s assume 50 percent of the total multiplier gets into the economy by year’s end (it will continue to benefit the economy for an additional 5 and a half years):

• 10,000 jobs created directly with an additional 3,000 to 4,000 spin-off jobs

• Reduction in unemployment and related costs

• An additional €350 million in tax revenue

• A GDP boost of 0.75 percent

A big impetus – which would take some time to get off the ground – would be an announcement that a public enterprise company will be established to build a Next Generation Broadband network to reach every household and business by 2015. While publicly-directed and owned, private investment can be leveraged in. This would be a clear signal of intent: that we are going to invest our way to economic recovery and fiscal stability.

Pledge 3: Reverse the cuts in social welfare income and the minimum wage

A pledge to reverse the cuts in social welfare income and the minimum wage should also be non-negotiable. This measure would boost demand and GDP, increase business turnover, protect retail employment and raise tax revenue (e.g. VAT, etc.). Therefore, it would end up costing the Exchequer far less than the headline cost of repealing the social welfare cuts (€397 million) while the reversing the minimum wage will actually boost Exchequer revenue.

There are other measures – minimal in cost but capable of lifting inequitable burdens on those on low incomes while increasing demand:

• Repealing the GMS co-payments – not likely to cost much after administrative savings are taken into account

• Protect all minimum wages – namely, no cut in pay rates and working conditions under Joint Labour Committees

• Increase Family Income Supplement by the amount as in Budget 2010 - €6 per child per week: this will enhance living standards of thousands of low and average income families with children.

Any increase on the public expenditure side would be more than compensated by tax measure introduced on high income groups (under Pledge 1), tax revenue from investment activity (under Pledge 2), and the benefit of higher demand that increasing people’s living standards would produce (under Pledge 3).

Its win-win-win.

* * *

This simple three-point programme does not address all the economic and social issues which progressive parties will have to address in their election manifestos, never mind when they are in government.

However, it would give a short, sharp signal to the electorate about progressive values and priorities. It will show people how people will be better off after 60 days of a progressive government. It will give everyone a clear picture of the medium-term direction of the new government.

And it will give something for progressive to agree over, instead of attacking each other. Such feuding only brings the prospect that more of the same failed economic thinking will dominate in the next government.

And who wants that?

Tuesday, 25 January 2011

A code of ethics for economists?

Paul Sweeney: The failings of the economics profession in predicting the Crash of 2008 have been a widely commented upon and criticised. One of the contributing factors to the Crash was tainted “advice” and “opinion” which urged people to borrow money from financial institutions and “get on the property ladder”. This too often came from economists with direct or indirect links to the financial sector, while newspapers with fat property supplements or pages of adverts for tax-break investments also regularly relied on such commentators.

This month (January 2011) almost 300 economists haved called on the American Economic Association to establish a code of ethics requiring disclosure of even potential conflicts of interest. And the AEA’s executive has just voted to set up a committee to consider the matter. Prof George Martino of the University of Denver said "There is a lot of hand-wringing in this profession over whether... we may have contributed to the financial crisis." The last time the economists’ ethics came up (in 1994), the AEA dismissed the idea.

What would a code of ethics requiring full disclosure mean for economists in Ireland? First, it would hit many of RTE's radio economic commentators, many of whom have links and agendas which they did not nor do they still reveal. Nor has RTE insisted on such disclosure. Secondly, it may hit those “independent economists” who write articles for the newspapers and magazines and, thirdly, it might make government and its agencies less enthusiastic about hiring advice which is so ideologically tainted.

As an economist working for the trade union movement, I am often taken aback by the hostility shown by some in the media to my critical perspective on markets, and by the contrasting soft interviews with those who worked for financial companies during the boom. The implication is that they are “independent” and I am biased. Yet it was far clearer where I was coming from, representing the largest civil society organisation in Ireland, whereas the “independent economists” were representing themselves or the companies who paid them.

Economists who work for companies in finance or other sectors like transport, whether full-time or as consultants, have urged changes in economic policies which benefit their linked companies, often without disclosing their connections.

It’s true that many academic economists are remote from the real world, and working with industry can help educate them in the workings of the economy. But during Ireland’s boom years the finance sector economists, who seemed to have their own desks in RTE and Today FM, played a very influential role in opinion formation, which was ultimately very destructive on the eocnomy

A study by two MIT academics, Epstein and Carrick-Hagenbarth, examined the work of 19 prominent academic financial economists who advocated financial “reform” (de-regulation) in newspaper and journal articles between 2005 and 2009; the study found that the economists were not honest in pointing out how they were conflicted.

“Our main findings are that in the vast majority of the time, these economists did not identify these affiliations and possible conflicts of interest. In light of these and related findings we call for an economists’ code of ethics which would require academic economists to identify these connections in appropriate contexts.”

The 19 academic economists were consultants, on the boards of financial firms, or had been trustees or advisors to them. They did not mention their affiliations.

Even the Economist magazine recently cited George DeMartino of University of Denver commenting on economists who have pushed free market policies, including financial liberalisation “on the basis of limited understanding or worse, because they ignored ways in which the real world departs from the idealised one of neoclassical economic theory.”

DeMartino says that, in the light of the immense impact that their opinions have had on the lives of ordinary citizens because of the Crash, economists should be a bit more humble about the limits of their knowledge. I add: not just in America.

This month (January 2011) almost 300 economists haved called on the American Economic Association to establish a code of ethics requiring disclosure of even potential conflicts of interest. And the AEA’s executive has just voted to set up a committee to consider the matter. Prof George Martino of the University of Denver said "There is a lot of hand-wringing in this profession over whether... we may have contributed to the financial crisis." The last time the economists’ ethics came up (in 1994), the AEA dismissed the idea.

What would a code of ethics requiring full disclosure mean for economists in Ireland? First, it would hit many of RTE's radio economic commentators, many of whom have links and agendas which they did not nor do they still reveal. Nor has RTE insisted on such disclosure. Secondly, it may hit those “independent economists” who write articles for the newspapers and magazines and, thirdly, it might make government and its agencies less enthusiastic about hiring advice which is so ideologically tainted.

As an economist working for the trade union movement, I am often taken aback by the hostility shown by some in the media to my critical perspective on markets, and by the contrasting soft interviews with those who worked for financial companies during the boom. The implication is that they are “independent” and I am biased. Yet it was far clearer where I was coming from, representing the largest civil society organisation in Ireland, whereas the “independent economists” were representing themselves or the companies who paid them.

Economists who work for companies in finance or other sectors like transport, whether full-time or as consultants, have urged changes in economic policies which benefit their linked companies, often without disclosing their connections.

It’s true that many academic economists are remote from the real world, and working with industry can help educate them in the workings of the economy. But during Ireland’s boom years the finance sector economists, who seemed to have their own desks in RTE and Today FM, played a very influential role in opinion formation, which was ultimately very destructive on the eocnomy

A study by two MIT academics, Epstein and Carrick-Hagenbarth, examined the work of 19 prominent academic financial economists who advocated financial “reform” (de-regulation) in newspaper and journal articles between 2005 and 2009; the study found that the economists were not honest in pointing out how they were conflicted.

“Our main findings are that in the vast majority of the time, these economists did not identify these affiliations and possible conflicts of interest. In light of these and related findings we call for an economists’ code of ethics which would require academic economists to identify these connections in appropriate contexts.”

The 19 academic economists were consultants, on the boards of financial firms, or had been trustees or advisors to them. They did not mention their affiliations.

Even the Economist magazine recently cited George DeMartino of University of Denver commenting on economists who have pushed free market policies, including financial liberalisation “on the basis of limited understanding or worse, because they ignored ways in which the real world departs from the idealised one of neoclassical economic theory.”

DeMartino says that, in the light of the immense impact that their opinions have had on the lives of ordinary citizens because of the Crash, economists should be a bit more humble about the limits of their knowledge. I add: not just in America.

Monday, 24 January 2011

Where are all our deposits going?

An Saoi: Household savings should be the most stable part of the your deposit base. Very few households have access to an Austrian or Swiss bank account - deposits are normally kept close to home for ease of access. Yet Irish household deposits fell precipitously during November declining by 2.4% in just one month. While there has been a continuous decline all year since they peaked in January 2010, November saw the trickle becoming a flood.

Such a movement raises many questions. We were already aware that many savers have moved their cash from the Irish owned banks, not trusting the Government guarantee with savers opting for foreign operators such as Rabobank and, at a more local level, many of the larger better run Credit Unions have also seen a substantial influx of cash. The better off or better connected have always had other options as Kathleen Barrington mentioned in her Sunday Business Post column back in October, and discussed more recently here; however, this is clearly only open to a few.

The reasons for the decline may also be more mundane - depositors needed the cash for general living expenses, or have decided to repay debt with their deposits. However, savers and borrowers are generally not the same people, though many parents may be helping adult children with loans and living expenses.

There is also a possible third reason – the public have decided to open their purse strings and start spending because they believe in Brian Lenihan's words, “we have turned a corner.”

No, I gather you don't believe that either.

The probable causes are a mixture of the reasons mentioned above together with two others: 1) the need by many small and medium business owners to put money back into businesses as loans for working capital have dried up, and (2) migrants taking savings home with them.

The ECB is vainly attempting to wean the Irish banks off their dependence on the interbank market. They are to be forced to reduce their lending to the level of their deposits. by the sale of large parts of their loan books to others, complete with a State guarantee for the purchasers from the Irish taxpayer. The proceeds of these loan sales will of course be used to pay back the ECB. But if the Irish banks have a shrunken domestic deposit base, where is the money to balance their remaining loan books to come from? Loans in 2011 for whatever purpose are likely to be even harder to come by than in 2010.

Assuming that the trend continues, the banks will have a very small pool of savings to draw from for which they will have to pay premium rates of interest. This will force them to withdraw existing short-term facilities as they cannot extricate themselves from their long-term commitments in the form of mortgage loans. Loan repayments received will be used to pay off the ECB, leaving little or no money available for new lending. We are looking at a group of zombie like banks, open but with empty shelves.

December normally sees a substantial rise in household deposits. Therefore any further decline when the returns are published at the month will be disastrous. The snow and ice of December will have prevented the rich from taking their suitcases of cash to Switzerland & Austria. Movements are likely to be driven by domestic factors and it is already suggested that the November trend has continued into December.

However if this trend of deposit withdrawal is to continue through 2011 then the tightening of credit conditions will not only continue but get worse. No new money available for business, no new money for mortgages. The only financial institutions with cash available to lend are the Credit Unions, who are not involved to any degree involved in these two areas of lending.

The Government have consistently said that they had to get involved in guaranteeing the banks to keep cash moving. Well the only cash moving is out of the banks as quickly as possible.

Why should we be worried? Seamus Coffey provided a graphic analysis of the Central Bank trends in a post he did on the October figures available here.

Such a movement raises many questions. We were already aware that many savers have moved their cash from the Irish owned banks, not trusting the Government guarantee with savers opting for foreign operators such as Rabobank and, at a more local level, many of the larger better run Credit Unions have also seen a substantial influx of cash. The better off or better connected have always had other options as Kathleen Barrington mentioned in her Sunday Business Post column back in October, and discussed more recently here; however, this is clearly only open to a few.

The reasons for the decline may also be more mundane - depositors needed the cash for general living expenses, or have decided to repay debt with their deposits. However, savers and borrowers are generally not the same people, though many parents may be helping adult children with loans and living expenses.

There is also a possible third reason – the public have decided to open their purse strings and start spending because they believe in Brian Lenihan's words, “we have turned a corner.”

No, I gather you don't believe that either.

The probable causes are a mixture of the reasons mentioned above together with two others: 1) the need by many small and medium business owners to put money back into businesses as loans for working capital have dried up, and (2) migrants taking savings home with them.

The ECB is vainly attempting to wean the Irish banks off their dependence on the interbank market. They are to be forced to reduce their lending to the level of their deposits. by the sale of large parts of their loan books to others, complete with a State guarantee for the purchasers from the Irish taxpayer. The proceeds of these loan sales will of course be used to pay back the ECB. But if the Irish banks have a shrunken domestic deposit base, where is the money to balance their remaining loan books to come from? Loans in 2011 for whatever purpose are likely to be even harder to come by than in 2010.

Assuming that the trend continues, the banks will have a very small pool of savings to draw from for which they will have to pay premium rates of interest. This will force them to withdraw existing short-term facilities as they cannot extricate themselves from their long-term commitments in the form of mortgage loans. Loan repayments received will be used to pay off the ECB, leaving little or no money available for new lending. We are looking at a group of zombie like banks, open but with empty shelves.

December normally sees a substantial rise in household deposits. Therefore any further decline when the returns are published at the month will be disastrous. The snow and ice of December will have prevented the rich from taking their suitcases of cash to Switzerland & Austria. Movements are likely to be driven by domestic factors and it is already suggested that the November trend has continued into December.

However if this trend of deposit withdrawal is to continue through 2011 then the tightening of credit conditions will not only continue but get worse. No new money available for business, no new money for mortgages. The only financial institutions with cash available to lend are the Credit Unions, who are not involved to any degree involved in these two areas of lending.

The Government have consistently said that they had to get involved in guaranteeing the banks to keep cash moving. Well the only cash moving is out of the banks as quickly as possible.

Why should we be worried? Seamus Coffey provided a graphic analysis of the Central Bank trends in a post he did on the October figures available here.

Saturday, 22 January 2011

Q&A at the doorsteps

Slí Eile: There is a distinct possibility that you will be getting more callers to the front door in the next few weeks. Be conscious that there may be a link between recent and prospective events, on the one hand, and on the other the 'Presentation of the National Recover Plan' update on the Department of Finance website here. Nothing obviously new there. It just says: 'This document relates to the National Recovery Plan 2011-2014 published on 24 November 2010.

However, the information within takes into account later data in 2010 as well as measures taken in Budget 2011.' Perhaps it a reminder to the Markets, IMF, EU, Political Parties - and voters - that the national authorities mean business. Take page 38 - composition of expenditure savings. Now you may wish to ask those friendly canvassers some questions including:

Will your party go with the broad parameters of the IMF-EU deal and the National Recovery Plan which envisages a cumulative four year 2.8billion cut in social welfare on top of the 0.9bn this year (2011)?

If not, will your party cut something else instead (public sector pay by an additional 2.8bn on top of savings already envisaged?)

If not cut other areas will your party seek negotiate the entire Plan and deal?

If the Markets, the IMF and the EU say no what is your party's 'Plan B'?

Please straight answers to straight questions. Time is of the essence.

However, the information within takes into account later data in 2010 as well as measures taken in Budget 2011.' Perhaps it a reminder to the Markets, IMF, EU, Political Parties - and voters - that the national authorities mean business. Take page 38 - composition of expenditure savings. Now you may wish to ask those friendly canvassers some questions including:

Will your party go with the broad parameters of the IMF-EU deal and the National Recovery Plan which envisages a cumulative four year 2.8billion cut in social welfare on top of the 0.9bn this year (2011)?

If not, will your party cut something else instead (public sector pay by an additional 2.8bn on top of savings already envisaged?)

If not cut other areas will your party seek negotiate the entire Plan and deal?

If the Markets, the IMF and the EU say no what is your party's 'Plan B'?

Please straight answers to straight questions. Time is of the essence.

Friday, 21 January 2011

Thursday, 20 January 2011

Recovery? What recovery?

Michael Taft: The ESRI’s new quarterly analysis is out (though not available on-line for 30 days). Though its forecasts are more pessimistic than the Government’s projections, they state:

‘ . . . we would not place too great an emphasis on the difference. Instead, we take it as being an on-going indicator of the challenges which are faced in restoring the public finances to a sustainable path.’

Maybe so, but the challenges, then, are getting even challengier. Let’s summarise.

Economic Growth

The ESRI is projecting sluggish growth coming off the recession. Whereas the Government is hoping for 4.9 percent GDP growth over the next two years, the ESRI suggests it will be only 3.7 percent.

The gap between the two is even larger with GNP – 3.6 percent compared to 1.7 percent. The domestic economy, according to the ESRI, will grow by less than half the rate the Government projects.

That considerable gap is more understandable when we see that the ESRI projects that the economy will still be in a domestic-demand recession by 2012 – the fifth year running.

Employment

The Government is hoping that net job creation over the two years will be positive – 21,000. The ESRI, reflecting their pessimism on the domestic economy, sees employment falling – by 20,000. Industry will continue to slide despite the increase in merchandise exports, falling by over 4 percent, with the service sector registering a smaller percentage fall.

Emigration, which is rightfully getting big headlines, is projected to be 100,000 over the next two years. The Government projected emigration to be 100,000 as well – but over the four year period up to 2014. Even with this higher emigration, the ESRI projects that the unemployment rate will still be higher than the Government’s estimates by 2012: 13 percent compared to 12 percent.

Investment

The fall in investment has been the driver in the Irish recession. According to the ESRI it will be some time before it is a driver in the recovery (at least under current policy). Investment is expected to fall, in nominal terms, from €18 billion to €17.6 billion by 2012.

Let’s put that in some perspective. In 2007, capital formation stood at €46 billion. Of course, much of this was part of the boom which was always going to melt away. But the Government hasn’t helped – cutting public investment by half since 2008, from €9 billion to €4.7 billion this year (and €3.5 billion by 2014). The even greater reliance on private sector investment will mean minimal growth over the years ahead.

Exports

This is the one category going from strength to strength. The ESRI is even more optimistic than the Government, projecting exports to grow by 11 percent over the next two years, after a strong performance last year (estimated at over 8 percent). But while the ESRI predicts growth in all sectors (goods, services, tourism), they are most bullish on what is essentially the modern sectors which are dominated by multi-nationals. As pointed out here, growth in the multi-national sectors will have a far less impact on the domestic economy than growth in indigenous exports. So the headline rate looks positive, but we will need more details on the composition of exports (which the ESRI doesn’t have) to assess its final impact on economic growth.

Consumer Spending

Another category of negative growth. The Government is hoping that consumer spending will grow, though only marginally (0.9 percent over the next two years); the ESRI is projecting a further fall of – 1.5 percent. This is due to income tax increases, cuts in social transfers, falling employment and emigration, etc. We can also throw in rising interest rates – the ESRI projects that the ECB main rate will rise from 1.0 to 2.5 by 2012. Higher payments on mortgages and other debt, means less spending on goods and services. All in all, consumer sentiment is expected to be cautious with the savings ratio remaining high.

Public Finances

Domestic demand, investment, consumer spending, employment – all down from Government projections. Yet, the ESRI is still hopeful that Government deficit targets can be met. In 2012, they are projecting a deficit of -7.7 percent, only fractionally worse than the Government’s own -7.4 percent projection. They explain it this way.

On the revenue side, the ESRI estimates that tax revenue will be €1.6 billion lower than Government estimates by 2012 – reflecting low economic and employment growth.

On the expenditure side, the ESRI estimates that net current spending will be €900 million less. This is made up mostly of declining interest payments (€800 million) arising from the reduction of the Exchequer cash balances as part of the IMF/EU bail-out.

If interest payments fall at the rate ESRI projects, the Government might hope to reach their target. But with revenue slipping and more demand on expenditure arising from higher unemployment and low incomes, the ESRI may be too optimistic on this score.

‘ . . . we would not place too great an emphasis on the difference. Instead, we take it as being an on-going indicator of the challenges which are faced in restoring the public finances to a sustainable path.’

Maybe so, but the challenges, then, are getting even challengier. Let’s summarise.

Economic Growth

The ESRI is projecting sluggish growth coming off the recession. Whereas the Government is hoping for 4.9 percent GDP growth over the next two years, the ESRI suggests it will be only 3.7 percent.

The gap between the two is even larger with GNP – 3.6 percent compared to 1.7 percent. The domestic economy, according to the ESRI, will grow by less than half the rate the Government projects.

That considerable gap is more understandable when we see that the ESRI projects that the economy will still be in a domestic-demand recession by 2012 – the fifth year running.

Employment

The Government is hoping that net job creation over the two years will be positive – 21,000. The ESRI, reflecting their pessimism on the domestic economy, sees employment falling – by 20,000. Industry will continue to slide despite the increase in merchandise exports, falling by over 4 percent, with the service sector registering a smaller percentage fall.

Emigration, which is rightfully getting big headlines, is projected to be 100,000 over the next two years. The Government projected emigration to be 100,000 as well – but over the four year period up to 2014. Even with this higher emigration, the ESRI projects that the unemployment rate will still be higher than the Government’s estimates by 2012: 13 percent compared to 12 percent.

Investment

The fall in investment has been the driver in the Irish recession. According to the ESRI it will be some time before it is a driver in the recovery (at least under current policy). Investment is expected to fall, in nominal terms, from €18 billion to €17.6 billion by 2012.

Let’s put that in some perspective. In 2007, capital formation stood at €46 billion. Of course, much of this was part of the boom which was always going to melt away. But the Government hasn’t helped – cutting public investment by half since 2008, from €9 billion to €4.7 billion this year (and €3.5 billion by 2014). The even greater reliance on private sector investment will mean minimal growth over the years ahead.

Exports

This is the one category going from strength to strength. The ESRI is even more optimistic than the Government, projecting exports to grow by 11 percent over the next two years, after a strong performance last year (estimated at over 8 percent). But while the ESRI predicts growth in all sectors (goods, services, tourism), they are most bullish on what is essentially the modern sectors which are dominated by multi-nationals. As pointed out here, growth in the multi-national sectors will have a far less impact on the domestic economy than growth in indigenous exports. So the headline rate looks positive, but we will need more details on the composition of exports (which the ESRI doesn’t have) to assess its final impact on economic growth.

Consumer Spending

Another category of negative growth. The Government is hoping that consumer spending will grow, though only marginally (0.9 percent over the next two years); the ESRI is projecting a further fall of – 1.5 percent. This is due to income tax increases, cuts in social transfers, falling employment and emigration, etc. We can also throw in rising interest rates – the ESRI projects that the ECB main rate will rise from 1.0 to 2.5 by 2012. Higher payments on mortgages and other debt, means less spending on goods and services. All in all, consumer sentiment is expected to be cautious with the savings ratio remaining high.

Public Finances

Domestic demand, investment, consumer spending, employment – all down from Government projections. Yet, the ESRI is still hopeful that Government deficit targets can be met. In 2012, they are projecting a deficit of -7.7 percent, only fractionally worse than the Government’s own -7.4 percent projection. They explain it this way.

On the revenue side, the ESRI estimates that tax revenue will be €1.6 billion lower than Government estimates by 2012 – reflecting low economic and employment growth.

On the expenditure side, the ESRI estimates that net current spending will be €900 million less. This is made up mostly of declining interest payments (€800 million) arising from the reduction of the Exchequer cash balances as part of the IMF/EU bail-out.

If interest payments fall at the rate ESRI projects, the Government might hope to reach their target. But with revenue slipping and more demand on expenditure arising from higher unemployment and low incomes, the ESRI may be too optimistic on this score.

Monday, 17 January 2011

Economists’ disconnect with the real world not just confined to Ireland

Proinnsias Breathnach: The disconnect between the economics profession and the real world of business and commerce which is so apparent in Ireland is not, apparently, confined to this country. In an article on the strong performance of the German economy in 2010 in last Friday’s (January 14) Irish Times, Derek Scally quotes two German economists who attribute this performance to greater labour flexibility and associated lower labour costs. Scally appears to have accepted this viewpoint, given the article’s subtitle: “A decade of labour and welfare reform laid the ground for Berlin’s latest success story”.

Yet the one example from the real world of business cited in the article gives an entirely different reason for Germany’s export growth. Daniel Dreizler, partner in a producer of high-tech gas burners for boilers, attributes the firm’s success to “long-term thinking and consistent investment of 5 per cent of turnover in research and development of high-tech patents and products”. Dreizler goes on: “We aren’t the ones who can offer a standard product cheaper; we will never manage that…We can offer a quality product that is more efficient and offers technical advantages, and argue for the price premium on that basis”.

Scally describes Dreizler as a “classic example” of “all that’s right with the German economy”. Yet the rest of his article highlights labour market and welfare reform as the key to Germany’s renewed economic success, even though Dreizler makes no reference at all to these. Is it too much to expect joined-up thinking in what purports to be Ireland’s leading serious newspaper?

Yet the one example from the real world of business cited in the article gives an entirely different reason for Germany’s export growth. Daniel Dreizler, partner in a producer of high-tech gas burners for boilers, attributes the firm’s success to “long-term thinking and consistent investment of 5 per cent of turnover in research and development of high-tech patents and products”. Dreizler goes on: “We aren’t the ones who can offer a standard product cheaper; we will never manage that…We can offer a quality product that is more efficient and offers technical advantages, and argue for the price premium on that basis”.

Scally describes Dreizler as a “classic example” of “all that’s right with the German economy”. Yet the rest of his article highlights labour market and welfare reform as the key to Germany’s renewed economic success, even though Dreizler makes no reference at all to these. Is it too much to expect joined-up thinking in what purports to be Ireland’s leading serious newspaper?

Sunday, 16 January 2011

Time for Plan B?

The euro area’s bail-out strategy is not working. It is time for insolvent countries to restructure their debts. You can read the rest of The Economist's leader here.

Thursday, 13 January 2011

Krugman's prescription for saving Europe

Tom McDonnell: Following on from Citigroup analysis of the Euro debt crisis earlier this week, here is an excellent analysis by Paul Krugman.

Krugman runs through the four possible scenarios for Ireland. He predicts that Ireland will ultimately have to restructure its debts. The four scenarios are:

1) Toughing it out – the current plan. Very harsh fiscal austerity to achieve internal devaluation and restore competitiveness, with accompanying depression level hits to output and employment.

2) Debt restructuring. Krugman sees debt restructuring, in conjunction with toughing it out, as being the likely scenario for Ireland.

3) Full Argentina – the nearest European equivalent being Iceland. The default and devalue combination.

4) Revived Europeanism – going down the transfer union path. The E-bond proposal would be the first step in this direction.

Krugman sees the internal devaluation strategy as a recipe for years of depression. According to Krugman the European currency union project is doomed to failure unless it also becomes a full transfer union.

Krugman runs through the four possible scenarios for Ireland. He predicts that Ireland will ultimately have to restructure its debts. The four scenarios are:

1) Toughing it out – the current plan. Very harsh fiscal austerity to achieve internal devaluation and restore competitiveness, with accompanying depression level hits to output and employment.

2) Debt restructuring. Krugman sees debt restructuring, in conjunction with toughing it out, as being the likely scenario for Ireland.

3) Full Argentina – the nearest European equivalent being Iceland. The default and devalue combination.

4) Revived Europeanism – going down the transfer union path. The E-bond proposal would be the first step in this direction.

Krugman sees the internal devaluation strategy as a recipe for years of depression. According to Krugman the European currency union project is doomed to failure unless it also becomes a full transfer union.

Wednesday, 12 January 2011

Interesting IMF paper

Here is an interesting paper that formalises an idea that many of us would agree with, that inequality caused the crisis.

Unfortunately the IMF policy prescriptions seem totally separate to their analysis.

Unfortunately the IMF policy prescriptions seem totally separate to their analysis.

Economic Treason

Nat O'Connor: Tags like 'Economic Treason' have been liberally applied since the outset of our economic and political crisis. Green Party backbencher, Trevor Sargent, is attempting to have a definition entered into the constitution.

Article 39 of the Constitution defines treason as follows:

Treason shall consist only in levying war against the State, or assisting any State or person or inciting or conspiring with any person to levy war against the State, or attempting by force of arms or other violent means to overthrow the organs of government established by this Constitution, or taking part or being concerned in or inciting or conspiring with any person to make or to take part or be concerned in any such attempt.

However, on the last sitting day of the Dáil before the holidays, Deputy Sargent introduced a bill seeking to change the constitution. This was not opposed by the Government, but will be debated as a private members bill (which almost never get supported by the Government, although they are rarely advanced by TDs on the Government's side of the house either).

The proposed new text for article 39 is as follows:

Article 39

1. (as above)

2. Economic treason shall consist of actions that result in reputational damage for the country, an unacceptable economic cost, or a loss of economic sovereignty for the State.

3. Nothing in this section shall preclude the drafting of legislation, applying these definitions retrospectively.

In this context, it is noteworthy that while Article 15 (Section 13) gives immunity to TDs and Senators to arrest when going to, returning from or within the precints of either house, this immunity is lifted in the case of treason (as defined by the Constitution).

Hence, TDs heading to the Dáil to vote for the blanket bank guarantee scheme could have (in hindsight) been arrested for attempted economic treason, as this vote doubtless caused reputational damage for the country, came at an unacceptable economic cost, and does imply a degree of lost economic sovereignty for the State. Indeed, the amendment proposes that their actions could be retrospectively be defined as treason; including the actions of the Deputy proposing this amendment! And nothing in the proposed amendment requires that actions taken by TDs need to be wilfull. The damage of their actions alone is enough to constitute treason - according to the proposed definition - and it does not state how much damage, cost or loss is required for an otherwise negligent or ill informed act to become treasonous.

Such a scenario illustrates that one of the problems with this proposal is that, whereas the treasonous nature of levying war or taking up arms against the institutions of the state is fairly obvious, the intent behind ideologically-driven or simply misguided economic decision-making is not so easily shown in court beyond reasonable doubt.

The same applies to the actions of financial institutions. Many bodies seek to make money from the state, whether they sell goods and services to public bodies, or use illegal means such as bribery to gain from public decision-making (for which reason we have planning tribunals). While various forms of wrong-doing may be identified, it would seem necessary to reserve the legal term 'treason' for those who actively seek to destroy this country using financial and economic means.

It is unlikely that merely self-serving greed constitutes treason; successful paracites don't kill their hosts.

Of course, this private members bill is highly unlikely to be passed. It is legally unenforceable, not least because making legal actions retrospectively into illegal ones runs completely against human rights and the foundation of the rule of law; even if those 'legal' actions were (in retospect) morally abhorrent.

Which reinforces the argument that reactive legislation is always too late! What was required was the more painstaking - but absolutely necessary - path of reforming the law in relation to economic activity before massive damage was done to the economy. Although the damage in done, in Ireland's case, we still need to put in place tough regulation for the future. What types of financial dealing are to be illegal or restricted? What uses of subsidiary companies and off-shore banking are to be tolerated? And so on.

The future stability and prosperity of this state requires strong regulation of the economy in the public interest. Valuable parliamentary time would be better spent proposing such regulation rather than putting forward ineffective definitions of treason that fail to address the failure of Ireland's ongoing experiment with laissez-faire economics.

Article 39 of the Constitution defines treason as follows:

Treason shall consist only in levying war against the State, or assisting any State or person or inciting or conspiring with any person to levy war against the State, or attempting by force of arms or other violent means to overthrow the organs of government established by this Constitution, or taking part or being concerned in or inciting or conspiring with any person to make or to take part or be concerned in any such attempt.

However, on the last sitting day of the Dáil before the holidays, Deputy Sargent introduced a bill seeking to change the constitution. This was not opposed by the Government, but will be debated as a private members bill (which almost never get supported by the Government, although they are rarely advanced by TDs on the Government's side of the house either).

The proposed new text for article 39 is as follows:

Article 39

1. (as above)

2. Economic treason shall consist of actions that result in reputational damage for the country, an unacceptable economic cost, or a loss of economic sovereignty for the State.

3. Nothing in this section shall preclude the drafting of legislation, applying these definitions retrospectively.

In this context, it is noteworthy that while Article 15 (Section 13) gives immunity to TDs and Senators to arrest when going to, returning from or within the precints of either house, this immunity is lifted in the case of treason (as defined by the Constitution).

Hence, TDs heading to the Dáil to vote for the blanket bank guarantee scheme could have (in hindsight) been arrested for attempted economic treason, as this vote doubtless caused reputational damage for the country, came at an unacceptable economic cost, and does imply a degree of lost economic sovereignty for the State. Indeed, the amendment proposes that their actions could be retrospectively be defined as treason; including the actions of the Deputy proposing this amendment! And nothing in the proposed amendment requires that actions taken by TDs need to be wilfull. The damage of their actions alone is enough to constitute treason - according to the proposed definition - and it does not state how much damage, cost or loss is required for an otherwise negligent or ill informed act to become treasonous.

Such a scenario illustrates that one of the problems with this proposal is that, whereas the treasonous nature of levying war or taking up arms against the institutions of the state is fairly obvious, the intent behind ideologically-driven or simply misguided economic decision-making is not so easily shown in court beyond reasonable doubt.

The same applies to the actions of financial institutions. Many bodies seek to make money from the state, whether they sell goods and services to public bodies, or use illegal means such as bribery to gain from public decision-making (for which reason we have planning tribunals). While various forms of wrong-doing may be identified, it would seem necessary to reserve the legal term 'treason' for those who actively seek to destroy this country using financial and economic means.

It is unlikely that merely self-serving greed constitutes treason; successful paracites don't kill their hosts.

Of course, this private members bill is highly unlikely to be passed. It is legally unenforceable, not least because making legal actions retrospectively into illegal ones runs completely against human rights and the foundation of the rule of law; even if those 'legal' actions were (in retospect) morally abhorrent.

Which reinforces the argument that reactive legislation is always too late! What was required was the more painstaking - but absolutely necessary - path of reforming the law in relation to economic activity before massive damage was done to the economy. Although the damage in done, in Ireland's case, we still need to put in place tough regulation for the future. What types of financial dealing are to be illegal or restricted? What uses of subsidiary companies and off-shore banking are to be tolerated? And so on.

The future stability and prosperity of this state requires strong regulation of the economy in the public interest. Valuable parliamentary time would be better spent proposing such regulation rather than putting forward ineffective definitions of treason that fail to address the failure of Ireland's ongoing experiment with laissez-faire economics.

Tuesday, 11 January 2011

The Hunt Report, and how to close the deficit

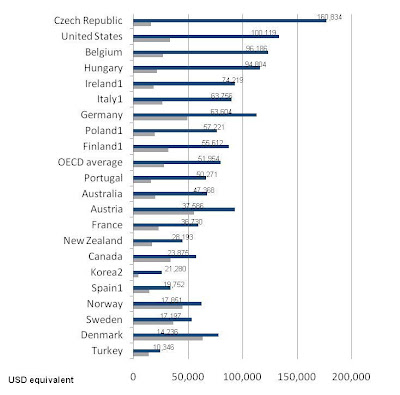

Michael Burke: There are many shortcomings in the Hunt Report ‘National Strategy for Higher Education’ – but one thing that’s very useful.

It's a shame that the authors have published a Report which cites the OECD Education At A Glance 2009 as the latest offering (p. 19). Just one month after the date of this draft report, EAAG 2010 was published in September 2010.

The accompanying press release for the later OECD study highlights the main theme of that report, titled 'Governments should expand tertiary studies to boost jobs and tax revenues'. Put another way: investment, not cuts.

The useful function performed by the Hunt Report is to highlight the relationship of this sector to the overall economy. We are told repeatedly that deficit-reduction is the overwhelming priority of economic policy. This from a government which has seen the public sector balance swing from surplus to over 32% of GDP.