Showing posts with label Michael Taft. Show all posts

Showing posts with label Michael Taft. Show all posts

Wednesday, 16 January 2013

Comparison of EU Bank Bailouts

Michael Taft uses Eurostat data here to compare the 'direct' impacts on General Government Deficits caused by the EU's numerous bank bailouts. In some cases these figures dont even capture the full cost of the bailouts as, for example, in the case of Ireland the €20 billion taken from the National Pension Reserve Fund is not included in the Eurostat figures.

Monday, 30 July 2012

A long ways to go

Michael Taft: It is difficult to come to a judgement on the NTMA bond sale. That we entered the bond market accessing new money is a plus, especially against a backdrop of yet another twist in the Eurozone crisis. That it builds up liquidity assets in anticipation of a large bond redemption in January 2014 is another plus. However, there are downsides and disappointments.

NamaWineLake compares the costs of the new bonds with borrowings from the EU-IMF bailout and finds that it will cost us nearly €1 billion more in interest payments up to 2020. However, this may not be the best comparator as it is the intention to exit the EU-IMF deal late next year. To test the water, so to speak, was always going to prove expensive at first.

There are two better comparisons. First, how do the interest rates compare with the secondary market? On the day of the bond sale, this is how the comparison stood using Bloomberg data.

For the 5-year bond (raising €3.9 billion):

• Bond sale: 6.1 percent

• Secondary market: 5.3

For the 8-year bond: (raising €1.3 billion):

• Bond Sale: 6.1 percent

• Secondary market: 6.2 percent

The majority of funds (from the 5-year bond sale) were borrowed at rates that compare badly with the secondary market. This is a disappointment. The 8-year sale just beat the interest rates on the secondary market.

Another comparison is with the beginning of 2010 – the year we started sliding into the bail-out with interest rates getting out of control. However, at the beginning of the year out interest rates were sustainable, though still high by comparison with most other EU-15 countries.

For the 5-year bond sale:

• Bond Sale: 5.9 percent

• January 2010: 3.3 percent

For the 8-year bond sale:

• Bond Sale: 6.1 percent

• January 2010: 4.5 percent

Again, the 5-year bond compares badly while the 8-year comparison shows a significant gap.

Can we close these gaps on a permanent basis by the end of next year? The only thing we can conclude from last week’s intervention is that we have a long, long way to go.

NamaWineLake compares the costs of the new bonds with borrowings from the EU-IMF bailout and finds that it will cost us nearly €1 billion more in interest payments up to 2020. However, this may not be the best comparator as it is the intention to exit the EU-IMF deal late next year. To test the water, so to speak, was always going to prove expensive at first.

There are two better comparisons. First, how do the interest rates compare with the secondary market? On the day of the bond sale, this is how the comparison stood using Bloomberg data.

For the 5-year bond (raising €3.9 billion):

• Bond sale: 6.1 percent

• Secondary market: 5.3

For the 8-year bond: (raising €1.3 billion):

• Bond Sale: 6.1 percent

• Secondary market: 6.2 percent

The majority of funds (from the 5-year bond sale) were borrowed at rates that compare badly with the secondary market. This is a disappointment. The 8-year sale just beat the interest rates on the secondary market.

Another comparison is with the beginning of 2010 – the year we started sliding into the bail-out with interest rates getting out of control. However, at the beginning of the year out interest rates were sustainable, though still high by comparison with most other EU-15 countries.

For the 5-year bond sale:

• Bond Sale: 5.9 percent

• January 2010: 3.3 percent

For the 8-year bond sale:

• Bond Sale: 6.1 percent

• January 2010: 4.5 percent

Again, the 5-year bond compares badly while the 8-year comparison shows a significant gap.

Can we close these gaps on a permanent basis by the end of next year? The only thing we can conclude from last week’s intervention is that we have a long, long way to go.

Tuesday, 10 July 2012

Bathing the rich

Michael Taft: Okay, so you’re not one of those who believe in soaking the rich. But what about bathing? A good bath is healthy for the body and the mind. And the economy. There are a number of arguments for increasing taxation on high incomes: that low-average income earners can’t afford to pay more; that there’ s a lot money to be gained; that it is less damaging to domestic demand; and that it is part of a general egalitarian and solidarity strategy. All these work – though there is always a debate over degrees.

What is not debatable is that inequality is accelerating in Ireland. In the run-up to Budget 2013 there are political choices to make. Let’s be clear: our rich are richer than the rich in other European countries. And we’re in recession. And we’re in bail-out.

Let’s take a tour through some data on high-income groups, how much they make, how much tax they pay. Let’s see if there is an argument for Budget 2013 to disproportionately impact on the highest earners.

1. Share of Income

How much share of the income pie do high income groups take? And how does it compare to other EU countries? All figures are taken from Eurostat. Statistical note: this refers to ‘equivalised income’. This is an artificial measurement that factors in the number of people in a household. For example: you might have two households with the same amount of income. However, there are more people in the second household which means that individually they have less income. ‘Equivalised income’ takes account of this.

As seen, high income groups in Ireland take a larger share of equivalised income than in other EU countries. The top Irish 1 percent takes over 6 percent of total income here. Throughout Europe, the top 1 percent take less – 4.6 percent; while in more egalitarian Sweden, the elite 1 percent takes only 3.7 percent of total income there.

The story is similar for the top Irish 5 percent and 10 percent. Our high income groups take up more of the national income pie than their counterparts throughout the EU-15.

To put this in perspective, the top 10 percent in Ireland take in almost as much income as the lowest half of the entire population. The lowest half takes in less than 28 percent, while the top 10 percent takes in 26.6 percent.

In short, our high income groups take more from the economy than high income groups of any other EU-15 country.

2. Levels of Income

What does this mean in income terms? Eurostat provides some insight but, again, here are some stat notes. First, it only provides the minimum and maximum income per decile. For instance, in Ireland the middle 5th decile household averages €31,565 in Disposable income. The range of Gross income in this 5th decile goes from €30,361 to €37,467. So an income of €30,361 is the starting income for the 5th decile.

Second, the following figures, again, refer to the artificial equivalised income.

So let’s look at the starting income for high income groups. What is the minimum income you need to get into this exclusive company?

In Ireland, the minimum equivalised income needed to get into the elite 1 percent is €98,000. In other EU-15 countries it is €67,000 while in Sweden, it is nearly half that of Ireland - €50,200. In other words, our elite 1 percent pull receive a lot more money than their elite EU counterparts.

Again, the story is similar for the top 5 percent and top 10 percent. In Ireland, these income groups not only take a larger share of the national income pie, they take in more Euros than similar high-income groups in the EU-15.

Just to remove any confusion – these income figures refer to ‘equivalised income’ and only to the minimum income in each decile. For instance, the the chart above shows that the minimum equivalised income to get into the top 10 percent to be €41,200. However, the actual average income for the top 10 percent is over €123,000. The difference is down to factoring in the number of people in the household.

The main point here is that Irish high-income groups compare very favourably to high income groups in other countries.

3. Implications for Budget 2013

Let’s play a game. Let’s say that the Government wanted to increase taxation on high-income groups but didn’t want to ‘soak’ them. Let’s say that they would only increase taxation to the extent that it reduces the disposable income of high income groups to EU averages. How much revenue could they expect to take in? This is based on the disposable income figures provided by the ESRI in their recent Economic Commentary.

If the Government fashioned a set of tax measures – rates, reduction of tax expenditures, new taxes, etc. – to bring the disposable income of the top 10 percent to EU averages, it would take in between €3 billion and €3.5 billion, enough to reach their Budget 2013 deficit target. If the Government went Nordic, it would be enough for the next two budgets.

Would this be too onerous on high income groups? No. It would mean they would be ‘earning’ the same as their EU counterparts. But let’s not forget: we are in recession, we are in a bail-out. If there is a time to ask people who can afford it to make a sacrifice, now is that time.

None of the above should be taken as an argument that we can tax-the-rich out of this crisis. For that, we need to increase growth, employment and wages. However, increasing tax on high-incomes can supplant cuts in public services, public investment and social protection, and would minimise damage to domestic demand. One does not need to be some wild-eyed, paid up member of the local ‘eat-the-rich’ chapter to see the pragmatic benefits of this approach.

Others have. As Cedar Lounge Revolution points out – in one country a party and presidential candidate actually kept their campaign promise to increase taxation on high income groups; up to 75 percent on the richest in the economy. Vive la France!

So let’s apply a little common sense. Let’s pursue a rational fiscal approach. Let’s bring a little equity into policy.

Let’s turn on the bath water.

Thanks to Dara Turnball for alerting me to this Eurostat database.

What is not debatable is that inequality is accelerating in Ireland. In the run-up to Budget 2013 there are political choices to make. Let’s be clear: our rich are richer than the rich in other European countries. And we’re in recession. And we’re in bail-out.

Let’s take a tour through some data on high-income groups, how much they make, how much tax they pay. Let’s see if there is an argument for Budget 2013 to disproportionately impact on the highest earners.

1. Share of Income

How much share of the income pie do high income groups take? And how does it compare to other EU countries? All figures are taken from Eurostat. Statistical note: this refers to ‘equivalised income’. This is an artificial measurement that factors in the number of people in a household. For example: you might have two households with the same amount of income. However, there are more people in the second household which means that individually they have less income. ‘Equivalised income’ takes account of this.

As seen, high income groups in Ireland take a larger share of equivalised income than in other EU countries. The top Irish 1 percent takes over 6 percent of total income here. Throughout Europe, the top 1 percent take less – 4.6 percent; while in more egalitarian Sweden, the elite 1 percent takes only 3.7 percent of total income there.

The story is similar for the top Irish 5 percent and 10 percent. Our high income groups take up more of the national income pie than their counterparts throughout the EU-15.

To put this in perspective, the top 10 percent in Ireland take in almost as much income as the lowest half of the entire population. The lowest half takes in less than 28 percent, while the top 10 percent takes in 26.6 percent.

In short, our high income groups take more from the economy than high income groups of any other EU-15 country.

2. Levels of Income

What does this mean in income terms? Eurostat provides some insight but, again, here are some stat notes. First, it only provides the minimum and maximum income per decile. For instance, in Ireland the middle 5th decile household averages €31,565 in Disposable income. The range of Gross income in this 5th decile goes from €30,361 to €37,467. So an income of €30,361 is the starting income for the 5th decile.

Second, the following figures, again, refer to the artificial equivalised income.

So let’s look at the starting income for high income groups. What is the minimum income you need to get into this exclusive company?

In Ireland, the minimum equivalised income needed to get into the elite 1 percent is €98,000. In other EU-15 countries it is €67,000 while in Sweden, it is nearly half that of Ireland - €50,200. In other words, our elite 1 percent pull receive a lot more money than their elite EU counterparts.

Again, the story is similar for the top 5 percent and top 10 percent. In Ireland, these income groups not only take a larger share of the national income pie, they take in more Euros than similar high-income groups in the EU-15.

Just to remove any confusion – these income figures refer to ‘equivalised income’ and only to the minimum income in each decile. For instance, the the chart above shows that the minimum equivalised income to get into the top 10 percent to be €41,200. However, the actual average income for the top 10 percent is over €123,000. The difference is down to factoring in the number of people in the household.

The main point here is that Irish high-income groups compare very favourably to high income groups in other countries.

3. Implications for Budget 2013

Let’s play a game. Let’s say that the Government wanted to increase taxation on high-income groups but didn’t want to ‘soak’ them. Let’s say that they would only increase taxation to the extent that it reduces the disposable income of high income groups to EU averages. How much revenue could they expect to take in? This is based on the disposable income figures provided by the ESRI in their recent Economic Commentary.

If the Government fashioned a set of tax measures – rates, reduction of tax expenditures, new taxes, etc. – to bring the disposable income of the top 10 percent to EU averages, it would take in between €3 billion and €3.5 billion, enough to reach their Budget 2013 deficit target. If the Government went Nordic, it would be enough for the next two budgets.

Would this be too onerous on high income groups? No. It would mean they would be ‘earning’ the same as their EU counterparts. But let’s not forget: we are in recession, we are in a bail-out. If there is a time to ask people who can afford it to make a sacrifice, now is that time.

None of the above should be taken as an argument that we can tax-the-rich out of this crisis. For that, we need to increase growth, employment and wages. However, increasing tax on high-incomes can supplant cuts in public services, public investment and social protection, and would minimise damage to domestic demand. One does not need to be some wild-eyed, paid up member of the local ‘eat-the-rich’ chapter to see the pragmatic benefits of this approach.

Others have. As Cedar Lounge Revolution points out – in one country a party and presidential candidate actually kept their campaign promise to increase taxation on high income groups; up to 75 percent on the richest in the economy. Vive la France!

So let’s apply a little common sense. Let’s pursue a rational fiscal approach. Let’s bring a little equity into policy.

Let’s turn on the bath water.

Thanks to Dara Turnball for alerting me to this Eurostat database.

Thursday, 28 June 2012

Splashing the water

Michael Taft: First there was Claiming our Future with its bold but common-sensical proposals to promote growth and equity in the economy. Now we have the Nevin Economic Research Institute (NERI) laying down a new fiscal framework to pursue such an alternative economic strategy. And it poses a real challenge to all progressives.

Some of us have just been working at the edges of the pond. For instance, some of us have argued for a freezing of current public expenditure at current levels up to 2015, substituting tax increases in place of spending cuts, and relying on an investment programme (mostly paid out of own resources) to increase our productive capacity in the medium-term. Of course, this approach accepts real cuts in the overall spending package (after inflation) but the argument is that savings on unemployment costs can be redirected into other areas of current spending. It still represents an expansionary fiscal platform, but a tight one.

NERI, however, runs past us all, jumps into the pond with both feet and starts splashing the water all around – including all over us. They, too, propose an expansionary programme but instead of freezing public spending, they want to increase it – increasing it to EU averages in the long-term. This would be combined with increasing government revenue to similar EU levels.

Let’s look at the differences – comparing Government projections, a ‘freeze-spending’ scenario, and NERI’s proposals. The following looks at overall spending minus interest payments – that is, primary expenditure.

As seen, while freezing spending would provide an additional €4.3 billion for current and capital spending above the Government’s projections, NERI’s proposals would provide an additional €9.8 billion. That’s a mighty sum.

The objections will be loud and voluminous – you’re adding to debt, you’re avoiding tough decisions (no one ever mentions avoiding bad decisions), you’re padding an already wasteful and inefficient public sector, etc. etc. and more etc.

But let’s briefly looks at some of the issues NERI’s proposals raise.

The first is whether you use GDP or GNP (or more properly GNI – which is GNP plus net EU payments) to measure spending. This is one of those bottom-less pit debates where consensus is almost impossible. I don’t intend to re-run the arguments here. However, it is worth noting that while Irish GDP per capita exceeds the EU-15 average, owing to the froth of multi-national accounting, Irish GNI per capita is about average. Average income, average spend – that’s NERI’s approach.

This suggests another approach to looking at expenditure. The following looks at Government spending on public services per capita. This is useful category given that overall spending can be skewered by pension expenditure in EU countries with a much older demographic.

Ireland would have to increase its spending on public services by €7.5 billion just to reach the average EU-levels. There’s doing more with less as the mantra goes; then there’s doing less with a lot less.

Second, NERI’s proposes to increase Government revenue to EU-15 averages. This would be a substantial sum. By 2017 it would mean €13 billion extra. I can hear a big gulp. But the important point here is that this doesn’t mean that this amount must be met by increasing current tax levels. Increasing growth and employment will make up a large part of this gap.

For instance, the Government intends to increase tax by €3 billion over the next three years. However, they project government revenue will increase by €7.5 billion. Growth will increase government revenue by nearly two-thirds; the fiscal adjustments will only account for a third. And that’s in a scenario where the Government is cutting investment and domestic demand. Imagine the increase in government revenue in a scenario where investment and domestic demand is increasing.

Third, the idea that public spending is a drain on public finances has been firmly established in the public debate by the austerity orthodoxy. NERI’s programme challenges this view.

For instance, the ESRI shows that increasing spending on public services by €1 billion (a combination of increased employment and wages) would mean an increase in the borrowing requirement of €580 million in the first year. Increasing income tax by €1 billion would reduce the borrowing requirement by €744 million. In other words, a straight one-for-one increase in income tax and spending on public services would result in a net reduction in the borrowing requirement.

This is not an argument that we can spend our way out of a recession. We can’t, we must invest. But it is an argument for a more sophisticated fiscal approach which uses a number of instruments in a carefully calibrated way. Increasing taxation beyond the economy’s capacity to absorb it (such as happened in the last few years) while increasing public spending without regard to productivity (which happened under Fianna Fail’s failed programme in the late 1970s) is a recipe for a real mess.

However, increased spending combined with similar increases in taxation can be a net boost to the economy and public finances. Imagine if we introduce a wealth tax and took the proceeds to roll-out an early childhood education network – that would be a boost in the short and long-term.

None of the above constitutes a ‘model’. There is still considerable work to be carried out. But there is considerable evidence to show that NERI’s programme would work, that Claiming our Future’s vision is achievable.

NERI has jumped into the pond and is splashing the water all around. I suggest we all follow suit. I have dipped my toe in. And the waters of an expansionary economic strategy are just fine.

Some of us have just been working at the edges of the pond. For instance, some of us have argued for a freezing of current public expenditure at current levels up to 2015, substituting tax increases in place of spending cuts, and relying on an investment programme (mostly paid out of own resources) to increase our productive capacity in the medium-term. Of course, this approach accepts real cuts in the overall spending package (after inflation) but the argument is that savings on unemployment costs can be redirected into other areas of current spending. It still represents an expansionary fiscal platform, but a tight one.

NERI, however, runs past us all, jumps into the pond with both feet and starts splashing the water all around – including all over us. They, too, propose an expansionary programme but instead of freezing public spending, they want to increase it – increasing it to EU averages in the long-term. This would be combined with increasing government revenue to similar EU levels.

Let’s look at the differences – comparing Government projections, a ‘freeze-spending’ scenario, and NERI’s proposals. The following looks at overall spending minus interest payments – that is, primary expenditure.

As seen, while freezing spending would provide an additional €4.3 billion for current and capital spending above the Government’s projections, NERI’s proposals would provide an additional €9.8 billion. That’s a mighty sum.

The objections will be loud and voluminous – you’re adding to debt, you’re avoiding tough decisions (no one ever mentions avoiding bad decisions), you’re padding an already wasteful and inefficient public sector, etc. etc. and more etc.

But let’s briefly looks at some of the issues NERI’s proposals raise.

The first is whether you use GDP or GNP (or more properly GNI – which is GNP plus net EU payments) to measure spending. This is one of those bottom-less pit debates where consensus is almost impossible. I don’t intend to re-run the arguments here. However, it is worth noting that while Irish GDP per capita exceeds the EU-15 average, owing to the froth of multi-national accounting, Irish GNI per capita is about average. Average income, average spend – that’s NERI’s approach.

This suggests another approach to looking at expenditure. The following looks at Government spending on public services per capita. This is useful category given that overall spending can be skewered by pension expenditure in EU countries with a much older demographic.

Ireland would have to increase its spending on public services by €7.5 billion just to reach the average EU-levels. There’s doing more with less as the mantra goes; then there’s doing less with a lot less.

Second, NERI’s proposes to increase Government revenue to EU-15 averages. This would be a substantial sum. By 2017 it would mean €13 billion extra. I can hear a big gulp. But the important point here is that this doesn’t mean that this amount must be met by increasing current tax levels. Increasing growth and employment will make up a large part of this gap.

For instance, the Government intends to increase tax by €3 billion over the next three years. However, they project government revenue will increase by €7.5 billion. Growth will increase government revenue by nearly two-thirds; the fiscal adjustments will only account for a third. And that’s in a scenario where the Government is cutting investment and domestic demand. Imagine the increase in government revenue in a scenario where investment and domestic demand is increasing.

Third, the idea that public spending is a drain on public finances has been firmly established in the public debate by the austerity orthodoxy. NERI’s programme challenges this view.

For instance, the ESRI shows that increasing spending on public services by €1 billion (a combination of increased employment and wages) would mean an increase in the borrowing requirement of €580 million in the first year. Increasing income tax by €1 billion would reduce the borrowing requirement by €744 million. In other words, a straight one-for-one increase in income tax and spending on public services would result in a net reduction in the borrowing requirement.

This is not an argument that we can spend our way out of a recession. We can’t, we must invest. But it is an argument for a more sophisticated fiscal approach which uses a number of instruments in a carefully calibrated way. Increasing taxation beyond the economy’s capacity to absorb it (such as happened in the last few years) while increasing public spending without regard to productivity (which happened under Fianna Fail’s failed programme in the late 1970s) is a recipe for a real mess.

However, increased spending combined with similar increases in taxation can be a net boost to the economy and public finances. Imagine if we introduce a wealth tax and took the proceeds to roll-out an early childhood education network – that would be a boost in the short and long-term.

None of the above constitutes a ‘model’. There is still considerable work to be carried out. But there is considerable evidence to show that NERI’s programme would work, that Claiming our Future’s vision is achievable.

NERI has jumped into the pond and is splashing the water all around. I suggest we all follow suit. I have dipped my toe in. And the waters of an expansionary economic strategy are just fine.

Friday, 11 May 2012

The structural deficit just got worse

Michael Taft: The latest EU Commission projections are out and, if anything, they show an even higher structural deficit than what the Government is projecting. This provides a perspective on what additional austerity might be in store for us under the Fiscal Treaty.

The EU Commission’s Spring Economic forecasts shows Ireland‘s structural budget balance to be far and away the highest in the Eurozone – at 7.9 percent for 2013. The Eurozone average is 1.8. We are much higher than Greece (4.5 percent), Spain (4.8 percent) and Portugal (4.6 percent).

The EU projection compares unfavourably to the Government’s own projection of 6.9 percent for 2013. In nominal terms, the EU is projecting a structural deficit over €1.6 billion higher than the Government for next year.

What is particularly noteworthy is how sluggishly the deficit is falling. Between 2011 and 2013, factoring in €7 billion worth of fiscal adjustments, the structural deficit falls by a mere 0.5 percent. The Government is hoping for a fall of 1 percent.

The EU doesn’t make projections outward to 2015. However, if we were to take 2013 as the starting point and use the Government’s pace of deficit reduction, we’d find a structural deficit of 4.5 percent for 2015. If this holds, the structural deficit has deteriorated and the gap between the EU projection and the Fiscal Treaty target has now widened to €7.2 billion. The Government estimated that it would be €5.4 billion.

To date, the Government has refused to engage with this issue. Instead, it insists that increased investment and micro-economic reforms will raise our productive capacity and that this will be enough to close the structural deficit gap without any further fiscal adjustments. However, whatever about the talk of growth and investment, the Government is doing the exact opposite as discussed here.

This is, of course, all a bit speculative as we don’t have EU projections out to 2015. But, with the new EU projections, we could now be facing into a higher structural deficit than that projected by the Government with a much slower decline. All things remaining the same, this means that the gap between the structural deficit and the Fiscal Treaty target just got larger. And, potentially, the amount of austerity needed just got greater.

The EU Commission’s Spring Economic forecasts shows Ireland‘s structural budget balance to be far and away the highest in the Eurozone – at 7.9 percent for 2013. The Eurozone average is 1.8. We are much higher than Greece (4.5 percent), Spain (4.8 percent) and Portugal (4.6 percent).

The EU projection compares unfavourably to the Government’s own projection of 6.9 percent for 2013. In nominal terms, the EU is projecting a structural deficit over €1.6 billion higher than the Government for next year.

What is particularly noteworthy is how sluggishly the deficit is falling. Between 2011 and 2013, factoring in €7 billion worth of fiscal adjustments, the structural deficit falls by a mere 0.5 percent. The Government is hoping for a fall of 1 percent.

The EU doesn’t make projections outward to 2015. However, if we were to take 2013 as the starting point and use the Government’s pace of deficit reduction, we’d find a structural deficit of 4.5 percent for 2015. If this holds, the structural deficit has deteriorated and the gap between the EU projection and the Fiscal Treaty target has now widened to €7.2 billion. The Government estimated that it would be €5.4 billion.

To date, the Government has refused to engage with this issue. Instead, it insists that increased investment and micro-economic reforms will raise our productive capacity and that this will be enough to close the structural deficit gap without any further fiscal adjustments. However, whatever about the talk of growth and investment, the Government is doing the exact opposite as discussed here.

This is, of course, all a bit speculative as we don’t have EU projections out to 2015. But, with the new EU projections, we could now be facing into a higher structural deficit than that projected by the Government with a much slower decline. All things remaining the same, this means that the gap between the structural deficit and the Fiscal Treaty target just got larger. And, potentially, the amount of austerity needed just got greater.

Tuesday, 8 May 2012

Will the Fiscal Treaty Cost Us?

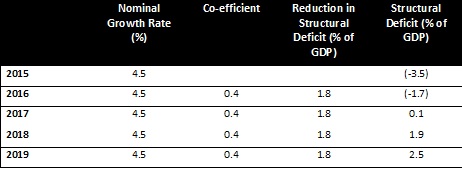

Michael Taft: Will the Fiscal Treaty – in particular, the notorious structural deficit rule – require additional austerity? John McHale of the Fiscal Council says it won’t. He accepts that in 2015 the gap between the Department of Finance’s projected structural deficit (3.5 percent) and the Fiscal Treaty target (0.5 percent) is €5.4 billion. But then he argues that growth can wipe that deficit out:

‘Growth affects both the denominator and the numerator of the structural deficit as a share of GDP. (For simplicity I assume that actual and potential GDP grow at equal rates post 2015.) The denominator effect is straightforward. For the numerator, we could use the standard coefficient used by the European Commission for Ireland that assumes that the reduction in the deficit is 0.4 times the change in nominal GDP. (This coefficient is usually used for doing cyclical adjustments, but it should also be applicable for measuring the impact of changes in nominal potential GDP on structural balance in the absence of discretionary adjustments to tax and expenditure parameters.)’

On this basis John does some calculations – using a more conservative co-efficient of 0.2. He finds the structural deficit is effectively wiped out by 2019 / 2020 without any additional austerity because growth has done all the heavy lifting.

I would suggest that this line of argument is flawed. First, I assume the co-efficient he uses refers to the cyclical sensitivity measurement of 0.4. This measurement is used to deconstruct the deficit into its ‘cyclical’ and ‘structural’ components. Essentially, you measure the gap between the real GDP and potential GDP growth and then apply the 0.4 to see how much of the gap is cyclical.

And herein lies the first problem – the 0.4 is an instrument to define the cyclical component of the output gap. It is not a measurement which defines the relationship between nominal growth rates and deficit reduction – whether it is the general or structural deficit. It is analogous to using a car clamp to change a light bulb. It is the wrong instrument. As the Department of Finance puts it:

‘Indeed, by definition, reducing the structural element of the deficit will require policy action. . . .‘

The whole point of structural deficit measurements is to determine what the deficit will be when the economy returns to full capacity. If the economy is firing on all cylinders and there is still a deficit, then the Government must take policy action to correct this, because growth cannot.

In doing his calculations, John assumes that real and potential GDP grow at the same rate. Never mind that the Government estimates that real GDP is growing at twice the rate of potential GDP in 2015 (yes, I know, this suggest that the economy is ‘over-heating’ – one of the absurdities with the model that the Department of Finance is using). If the output gap is zero, there is no role for applying the 0.4 co-efficient because there is no cyclical component to measure.

Seamus Coffey does his own calculations based on John’s more conservative co-efficient of 0.2 and applies it to GDP growth (though Seamus does say ‘There is no way of knowing what this’ co-efficient is). He comes up with a similar result to John.

But there is a problem here. Why use a conservative 0.2 co-efficient? If you believe that 0.4 tells the story, go with it. And why, use a nominal growth rate of 3.5 percent? The Government claims that in 2015 the nominal growth rate is 4.5 percent. So let’s go with that.

What do we get? We find that the structural deficit turns into a structural surplus without doing anything.

And what a surplus! By 2019 we will have a structural surplus of 2.5 percent. We outdo even the Germans. We get to go to the top of the class.

Is this likely? No. But we don’t have to argue the toss about cyclical sensitivity measurements or coefficients of elasticity. We merely have to go to the IMF’s own projection – which helps because (a) they stretch out to 2017 and (b) they assume, like John, no fiscal adjustment after 2015. What do they find?

In percentage terms, the reduction in the structural deficit is minimal: less than 0.1 percent of GDP each year.

But why should this surprise us? If there is deficit left over after the output gap is closed (after the economy returns to full capacity), what remains is the structural deficit which requires ‘policy action’ to reduce.

Political Implications

But there’s more to all this than duelling statistics. The Government and their austerity supporters have co-opted the language of progressives to avoid answering a fundamental question: what the cost of the Fiscal Treaty will be in terms of future austerity measures. They are now talking about ‘growth’ being the main instrument of deficit-reduction. The Government has even gone so far as to say that investment will grow the productive capacity and, therefore, reduce the deficit. Some of us have been saying that since the start of the crisis – UNITE and the trade union movement, TASC, contributors on Progressive-Economy; all we got was ridicule and scorn.

Here’s how the Department of Finance puts it:

‘Indeed, by definition, reducing the structural element of the deficit will require policy action, though not necessarily taxation and expenditure adjustments. Other options are available . . . . Such measures include labour market reforms - some of which are already in train - together with investment in technology and infrastructure to boost the productive capacity of the economy. To this end, the Government has established NewERA and the Strategic Investment Fund . . .

This ambitious programme of microeconomic reforms, by boosting the productive capacity of the economy, is expected to help reduce the structural element of the deficit by the middle part of the decade. For example, reforms along the lines of those set out in the Action Plan for Jobs 2012 and the Pathways to Work initiative, aimed at addressing some of the skills mis-match in the labour market, should help lower the unemployment rate. This would have a structurally beneficial impact on the public finances, on both the revenue and expenditure sides. In other words, the structural fiscal position is set to improve with these microeconomic reforms.’

And, yet, yet – the Government still refuses to provide a projection for this. If they are convinced that investment and labour market reforms will boost our productivity, they can project this – through the ‘potential GDP’ which measures the contribution of labour, capital and productivity.

This is all a charade. At the same time as the Government is assuring us that growing our potential GDP will reduce the structural deficit, they are actually revising downwards potential GDP.

In the last budget, the Government projected that our productive capacity would grow by 3.4 percent between 2010 and 2015. Only a few months later, the Government is now projecting growth at 2.4 percent. This revision downwards reflects their lower GDP projections.

In other words, we are going forward by going backwards.

This is the ultimate game plan. Stonewall any questions about the cost of the Fiscal Treaty with talk of growing our productive capacity even as you revise downwards our productive capacity. ‘Prove’ that growth will reduce the structural deficit by using variables that have little reference to structural deficit reduction. But don’t ‘prove’ it too much because it will look nonsensical. Ignore what current projections (IMF) have to say about all this. Even ignore the definition of a structural deficit. Above all, abandon your austerity clothes and don the robes of an expansionary programme – even as you promise to cut public investment next year and cut spending on public services and social protection by even more than you did this year.

Do all this. But don’t call it austerity.

‘Growth affects both the denominator and the numerator of the structural deficit as a share of GDP. (For simplicity I assume that actual and potential GDP grow at equal rates post 2015.) The denominator effect is straightforward. For the numerator, we could use the standard coefficient used by the European Commission for Ireland that assumes that the reduction in the deficit is 0.4 times the change in nominal GDP. (This coefficient is usually used for doing cyclical adjustments, but it should also be applicable for measuring the impact of changes in nominal potential GDP on structural balance in the absence of discretionary adjustments to tax and expenditure parameters.)’

On this basis John does some calculations – using a more conservative co-efficient of 0.2. He finds the structural deficit is effectively wiped out by 2019 / 2020 without any additional austerity because growth has done all the heavy lifting.

I would suggest that this line of argument is flawed. First, I assume the co-efficient he uses refers to the cyclical sensitivity measurement of 0.4. This measurement is used to deconstruct the deficit into its ‘cyclical’ and ‘structural’ components. Essentially, you measure the gap between the real GDP and potential GDP growth and then apply the 0.4 to see how much of the gap is cyclical.

And herein lies the first problem – the 0.4 is an instrument to define the cyclical component of the output gap. It is not a measurement which defines the relationship between nominal growth rates and deficit reduction – whether it is the general or structural deficit. It is analogous to using a car clamp to change a light bulb. It is the wrong instrument. As the Department of Finance puts it:

‘Indeed, by definition, reducing the structural element of the deficit will require policy action. . . .‘

The whole point of structural deficit measurements is to determine what the deficit will be when the economy returns to full capacity. If the economy is firing on all cylinders and there is still a deficit, then the Government must take policy action to correct this, because growth cannot.

In doing his calculations, John assumes that real and potential GDP grow at the same rate. Never mind that the Government estimates that real GDP is growing at twice the rate of potential GDP in 2015 (yes, I know, this suggest that the economy is ‘over-heating’ – one of the absurdities with the model that the Department of Finance is using). If the output gap is zero, there is no role for applying the 0.4 co-efficient because there is no cyclical component to measure.

Seamus Coffey does his own calculations based on John’s more conservative co-efficient of 0.2 and applies it to GDP growth (though Seamus does say ‘There is no way of knowing what this’ co-efficient is). He comes up with a similar result to John.

But there is a problem here. Why use a conservative 0.2 co-efficient? If you believe that 0.4 tells the story, go with it. And why, use a nominal growth rate of 3.5 percent? The Government claims that in 2015 the nominal growth rate is 4.5 percent. So let’s go with that.

What do we get? We find that the structural deficit turns into a structural surplus without doing anything.

And what a surplus! By 2019 we will have a structural surplus of 2.5 percent. We outdo even the Germans. We get to go to the top of the class.

Is this likely? No. But we don’t have to argue the toss about cyclical sensitivity measurements or coefficients of elasticity. We merely have to go to the IMF’s own projection – which helps because (a) they stretch out to 2017 and (b) they assume, like John, no fiscal adjustment after 2015. What do they find?

In percentage terms, the reduction in the structural deficit is minimal: less than 0.1 percent of GDP each year.

But why should this surprise us? If there is deficit left over after the output gap is closed (after the economy returns to full capacity), what remains is the structural deficit which requires ‘policy action’ to reduce.

Political Implications

But there’s more to all this than duelling statistics. The Government and their austerity supporters have co-opted the language of progressives to avoid answering a fundamental question: what the cost of the Fiscal Treaty will be in terms of future austerity measures. They are now talking about ‘growth’ being the main instrument of deficit-reduction. The Government has even gone so far as to say that investment will grow the productive capacity and, therefore, reduce the deficit. Some of us have been saying that since the start of the crisis – UNITE and the trade union movement, TASC, contributors on Progressive-Economy; all we got was ridicule and scorn.

Here’s how the Department of Finance puts it:

‘Indeed, by definition, reducing the structural element of the deficit will require policy action, though not necessarily taxation and expenditure adjustments. Other options are available . . . . Such measures include labour market reforms - some of which are already in train - together with investment in technology and infrastructure to boost the productive capacity of the economy. To this end, the Government has established NewERA and the Strategic Investment Fund . . .

This ambitious programme of microeconomic reforms, by boosting the productive capacity of the economy, is expected to help reduce the structural element of the deficit by the middle part of the decade. For example, reforms along the lines of those set out in the Action Plan for Jobs 2012 and the Pathways to Work initiative, aimed at addressing some of the skills mis-match in the labour market, should help lower the unemployment rate. This would have a structurally beneficial impact on the public finances, on both the revenue and expenditure sides. In other words, the structural fiscal position is set to improve with these microeconomic reforms.’

And, yet, yet – the Government still refuses to provide a projection for this. If they are convinced that investment and labour market reforms will boost our productivity, they can project this – through the ‘potential GDP’ which measures the contribution of labour, capital and productivity.

This is all a charade. At the same time as the Government is assuring us that growing our potential GDP will reduce the structural deficit, they are actually revising downwards potential GDP.

In the last budget, the Government projected that our productive capacity would grow by 3.4 percent between 2010 and 2015. Only a few months later, the Government is now projecting growth at 2.4 percent. This revision downwards reflects their lower GDP projections.

In other words, we are going forward by going backwards.

This is the ultimate game plan. Stonewall any questions about the cost of the Fiscal Treaty with talk of growing our productive capacity even as you revise downwards our productive capacity. ‘Prove’ that growth will reduce the structural deficit by using variables that have little reference to structural deficit reduction. But don’t ‘prove’ it too much because it will look nonsensical. Ignore what current projections (IMF) have to say about all this. Even ignore the definition of a structural deficit. Above all, abandon your austerity clothes and don the robes of an expansionary programme – even as you promise to cut public investment next year and cut spending on public services and social protection by even more than you did this year.

Do all this. But don’t call it austerity.

Tuesday, 24 April 2012

Ireland's financing alternatives - the EFSF

Tom McDonnell and Michael Taft: In our first post, we outlined some of Ireland’s financing alternatives; namely through the IMF and the European Stability Mechanism. There is, however, a more compelling source of institutional funding in the eventuality of a No vote: the European Financial Stability Facility (EFSF).

The EFSF is one of four external sources of funding for the current Irish bail-out (along with the IMF, the European Financial Stabilisation Mechanism, and bi-lateral loan agreements with the UK, Sweden and Denmark). The EFSF remains a source of funding for all Eurozone countries until the middle of next year.

The EFSF stands apart from the ESM and the Fiscal Treaty. Ireland, and all countries who are members of the EFSF, has access to this fund as of right, depending on the following conditions:

• They cannot access funding at reasonable rates on the international markets

• They have negotiated a Memorandum of Understanding with the EU and the IMF

A further stipulation is unanimous consent from the Finance Ministers of the Eurozone (Eurogroup), which would follow on from an agreement with the EU/IMF. Applications for this funding can be made up to the end of June 2013. After that the EFSF will only administer funding that has already been agreed.

According to the recent Eurogroup statement (the Finance Ministers of Eurozone countries):

‘For a transitional period until mid-2013, it (the EFSF) may engage in new programmes in order to ensure a full fresh lending capacity of EUR 500 billion (for the ESM).’

This is confirmed by the EFSF itself which states:

‘ . . . following the Eurogroup meeting held on 30 March, it was decided that the EFSF would remain active until July 2013 . . . For a transitional period until 2013, EFSF may engage in new programmes in order to ensure a full fresh lending capacity of €500 billion . . . after June 2013, EFSF [will] not enter into any new programmes.’

Therefore, were Ireland to apply for a second bail-out prior to July 1st 2013, it would be granted if such an application were accompanied by a Memorandum of Understanding negotiated between Ireland, the EU and the IMF – similar to the first bail-out. This funding is not contingent upon the ratification of the Fiscal Treaty.

In all probability, funding for Ireland’s second bail-out – whether it approves the Fiscal Treaty or not – will be routed through the EFSF. The EFSF (the temporary bailout fund in place up to July 2013) and the ESM (permanent bailout mechanism) are different companies. The EFSF has €440 billion (see page 1 of the EFSF document) of which €192 billion already committed to Ireland, Portugal and Greece (see the diagram on page 20 of the EFSF document). The remaining lending capacity of the EFSF for programmes initiated before July 2013 is therefore €248 billion. The EFSF will remain in place to manage its existing programmes (see diagram on page 20 of the EFSF document) and any other new programmes approved prior to July 2013, until such time as all these programmes are all wound down.

The ESM itself has €500 billion and is scheduled to enter force on 1 July 2012. As stated above, the intention would be to ensure the ESM retains its full lending capacity of €500 billion. This no doubt refers to the prospect of larger countries, in particular Spain, needing a bail-out. The ESM would require full capacity to accommodate new countries’ need for a bail-out.

Ireland’s continuing access to institutional funding beyond the current bail-out programme has been guaranteed not once, but twice, by the Heads of States and Government; first, on July 21st of last year when the establishment of the European Stability Mechanism was agreed, and most recently on January 30th of this year – after the Fiscal Treaty was signed:

‘We welcome the latest positive reviews of the Irish and Portuguese programmes which concluded that quantitative performance criteria and structural benchmarks have been met. We will continue to provide support to countries under a programme until they have regained market access, provided they successfully implement their programmes.’

This is an important and helpful guarantee. There is no condition set on continued support until we return to the markets – except that we implement agreed programmes. If continued support were contingent upon acceptance of the Treaty, we should have expected it to be highlighted in this statement.

This helps explain another issue we highlighted in the first post. The drafters of the European Stability Mechanism Treaty inserted clauses that provide manoeuvrability in negotiations with any Eurozone country in need of financing, regardless of the Fiscal Treaty. In particular, they inserted references to ‘new programmes under the European Stability Mechanism’, a clause which would have been unnecessary if all financing under the ESM were strictly conditional on a yes vote. They have seemingly factored in a situation whereby a second bail-out for Ireland (and potentially Portugal and Greece) would constitute ‘rolled-over’ financing, rather than ‘new’ financing. This buttresses the guarantee given by the Heads of States and Governments – namely that Ireland will continue to be supported until we return to the markets.

This is an important debate as there is a high probability that Ireland will require a second bail-out. We are expected to return to the markets in late 2013 and fully by 2014. However, the IMF is cautious:

‘Debt sustainability remains fragile, especially with respect to medium-term growth prospects . . . In this context, the prospects for regaining the substantial access to market funding that is assumed in 2013 remain uncertain.’

Were a second bail-out required, we estimate that it could be as large as €45 billion and possibly more for the years 2014 and 2015, taking into account the Exchequer balance and bond redemptions. This does not include bank payments. While this is less than the current bail-out provision it is clear that Ireland, without access to either market or institutional funding, would not be able to cope with this fiscally. We would be heading into a default – quite possibly on both sovereign and banking debt. This would have negative spillover effects for other Eurozone countries.

We reiterate the point from our first post: there is no reason to resort to counter-posing ‘appalling scenarios’. Some argue that Ireland will be frozen out of both market and institutional funding if we vote No. Clearly, this would be an appalling scenario. Others argue that it would never come to this because of the impact on the Eurozone (defaults, contagion) – another appalling scenario.

This is not a satisfactory way to debate this issue. This will trap us in a ‘race-to-disaster’ debate which will be particularly uninformative. We have attempted to outline concrete alternative funding scenarios for Ireland. Whether these would become available is a subject for legitimate debate. However, those who claim that Ireland would be denied access to EFSF funding – or any other funding sources – should provide concrete evidence to this effect. Evidence one way or the other would be a valuable contribution.

The debate over the Fiscal Treaty should be just that – a debate about the provisions of the Treaty. In this respect, it is helpful to note wider European developments. Spain has, unsurprisingly, officially re-entered recession putting at risk their deficit targets; the prospect of a Socialist Party victory in the French second-round Presidential vote raises the prospect of some renegotiation of the Fiscal Treaty; the fall of the Dutch government over failure to agree budget cuts highlights the problems posed by the Fiscal Compact in a major core country.

As Ireland prepares for the referendum vote, the ground under the Fiscal Treaty may already be shifting. Resort to ‘appalling scenarios’ will only confuse the issue when the debate should be focused on whether the provisions of the Fiscal Treaty are good, or even sustainable, for Ireland and the Eurozone.

The EFSF is one of four external sources of funding for the current Irish bail-out (along with the IMF, the European Financial Stabilisation Mechanism, and bi-lateral loan agreements with the UK, Sweden and Denmark). The EFSF remains a source of funding for all Eurozone countries until the middle of next year.

The EFSF stands apart from the ESM and the Fiscal Treaty. Ireland, and all countries who are members of the EFSF, has access to this fund as of right, depending on the following conditions:

• They cannot access funding at reasonable rates on the international markets

• They have negotiated a Memorandum of Understanding with the EU and the IMF

A further stipulation is unanimous consent from the Finance Ministers of the Eurozone (Eurogroup), which would follow on from an agreement with the EU/IMF. Applications for this funding can be made up to the end of June 2013. After that the EFSF will only administer funding that has already been agreed.

According to the recent Eurogroup statement (the Finance Ministers of Eurozone countries):

‘For a transitional period until mid-2013, it (the EFSF) may engage in new programmes in order to ensure a full fresh lending capacity of EUR 500 billion (for the ESM).’

This is confirmed by the EFSF itself which states:

‘ . . . following the Eurogroup meeting held on 30 March, it was decided that the EFSF would remain active until July 2013 . . . For a transitional period until 2013, EFSF may engage in new programmes in order to ensure a full fresh lending capacity of €500 billion . . . after June 2013, EFSF [will] not enter into any new programmes.’

Therefore, were Ireland to apply for a second bail-out prior to July 1st 2013, it would be granted if such an application were accompanied by a Memorandum of Understanding negotiated between Ireland, the EU and the IMF – similar to the first bail-out. This funding is not contingent upon the ratification of the Fiscal Treaty.

In all probability, funding for Ireland’s second bail-out – whether it approves the Fiscal Treaty or not – will be routed through the EFSF. The EFSF (the temporary bailout fund in place up to July 2013) and the ESM (permanent bailout mechanism) are different companies. The EFSF has €440 billion (see page 1 of the EFSF document) of which €192 billion already committed to Ireland, Portugal and Greece (see the diagram on page 20 of the EFSF document). The remaining lending capacity of the EFSF for programmes initiated before July 2013 is therefore €248 billion. The EFSF will remain in place to manage its existing programmes (see diagram on page 20 of the EFSF document) and any other new programmes approved prior to July 2013, until such time as all these programmes are all wound down.

The ESM itself has €500 billion and is scheduled to enter force on 1 July 2012. As stated above, the intention would be to ensure the ESM retains its full lending capacity of €500 billion. This no doubt refers to the prospect of larger countries, in particular Spain, needing a bail-out. The ESM would require full capacity to accommodate new countries’ need for a bail-out.

Ireland’s continuing access to institutional funding beyond the current bail-out programme has been guaranteed not once, but twice, by the Heads of States and Government; first, on July 21st of last year when the establishment of the European Stability Mechanism was agreed, and most recently on January 30th of this year – after the Fiscal Treaty was signed:

‘We welcome the latest positive reviews of the Irish and Portuguese programmes which concluded that quantitative performance criteria and structural benchmarks have been met. We will continue to provide support to countries under a programme until they have regained market access, provided they successfully implement their programmes.’

This is an important and helpful guarantee. There is no condition set on continued support until we return to the markets – except that we implement agreed programmes. If continued support were contingent upon acceptance of the Treaty, we should have expected it to be highlighted in this statement.

This helps explain another issue we highlighted in the first post. The drafters of the European Stability Mechanism Treaty inserted clauses that provide manoeuvrability in negotiations with any Eurozone country in need of financing, regardless of the Fiscal Treaty. In particular, they inserted references to ‘new programmes under the European Stability Mechanism’, a clause which would have been unnecessary if all financing under the ESM were strictly conditional on a yes vote. They have seemingly factored in a situation whereby a second bail-out for Ireland (and potentially Portugal and Greece) would constitute ‘rolled-over’ financing, rather than ‘new’ financing. This buttresses the guarantee given by the Heads of States and Governments – namely that Ireland will continue to be supported until we return to the markets.

This is an important debate as there is a high probability that Ireland will require a second bail-out. We are expected to return to the markets in late 2013 and fully by 2014. However, the IMF is cautious:

‘Debt sustainability remains fragile, especially with respect to medium-term growth prospects . . . In this context, the prospects for regaining the substantial access to market funding that is assumed in 2013 remain uncertain.’

Were a second bail-out required, we estimate that it could be as large as €45 billion and possibly more for the years 2014 and 2015, taking into account the Exchequer balance and bond redemptions. This does not include bank payments. While this is less than the current bail-out provision it is clear that Ireland, without access to either market or institutional funding, would not be able to cope with this fiscally. We would be heading into a default – quite possibly on both sovereign and banking debt. This would have negative spillover effects for other Eurozone countries.

We reiterate the point from our first post: there is no reason to resort to counter-posing ‘appalling scenarios’. Some argue that Ireland will be frozen out of both market and institutional funding if we vote No. Clearly, this would be an appalling scenario. Others argue that it would never come to this because of the impact on the Eurozone (defaults, contagion) – another appalling scenario.

This is not a satisfactory way to debate this issue. This will trap us in a ‘race-to-disaster’ debate which will be particularly uninformative. We have attempted to outline concrete alternative funding scenarios for Ireland. Whether these would become available is a subject for legitimate debate. However, those who claim that Ireland would be denied access to EFSF funding – or any other funding sources – should provide concrete evidence to this effect. Evidence one way or the other would be a valuable contribution.

The debate over the Fiscal Treaty should be just that – a debate about the provisions of the Treaty. In this respect, it is helpful to note wider European developments. Spain has, unsurprisingly, officially re-entered recession putting at risk their deficit targets; the prospect of a Socialist Party victory in the French second-round Presidential vote raises the prospect of some renegotiation of the Fiscal Treaty; the fall of the Dutch government over failure to agree budget cuts highlights the problems posed by the Fiscal Compact in a major core country.

As Ireland prepares for the referendum vote, the ground under the Fiscal Treaty may already be shifting. Resort to ‘appalling scenarios’ will only confuse the issue when the debate should be focused on whether the provisions of the Fiscal Treaty are good, or even sustainable, for Ireland and the Eurozone.

Thursday, 12 April 2012

Responding to the Minister

Michael Taft: The Minister for Public Expenditure and Reform, Brendan Howlin, has responded to the open letter signed by 39 economists, social scientists and analysts. It is welcomed that a Government Minister is willing to engage constructively as this can only improve the public debate. That the Minister claims there is considerable common ground between the contributors and the Government is further welcomed. But ultimately the Minister doesn’t believe the strategy outlined by the contributors is viable. I’d like to address some of the issues the Minister raised in his article. I speak, of course, only for myself and not for any other signatory of the open letter.

The first problem we confront is a disconnect between what the Minister claims and what is actually happening in the economy. He states:

‘The importance of growth is factored into our budgetary figures. Our own economy has returned to modest growth and indeed, the greatest impediment to future growth is the state of the global economy.’

The problem here is that the economy has actually returned to recession – a double-dip recession. The latest quarterly data we have – from the second half of last year – shows GDP in decline. When we turn to the domestic economy, we find the biggest fall since the dark days of 2009. It is difficult to reconcile the statement ‘our own economy has returned to modest growth’ with the fact that we are back in recession.

The second problem is a denial of what the Government is actually doing.

‘Contrary to the view articulated (by the contributors), the Government is not pursuing an “austerity” strategy. The opposite is the case.’

Again, it is hard to reconcile this with what the current Government is doing. In the last budget, the Government engaged in a fiscal contraction equivalent to €4.3 billion (according to the EU Commission, factoring in the carryover from Budget 2011). This was made up of tax increases – primarily regressive VAT increases – and spending cuts, in particular a significant €750 million capital investment cut.

This will have a profound impact, not only on the social fabric, but on economic growth. The Minister for Finance has estimated that for every €1 billion in cuts/tax increases, the GDP falls by €500 million. On this basis, the Government reduced growth by €2.15 billion or over 1 percent off real GDP.

It is worth noting that the Government is now at pains to distance itself from the word ‘austerity’ – such is the low esteem it is now held among people since it is a by-word for low-growth, job losses and rising debt. However, to maintain that you are not pursuing austerity while at the same time doing just that is slightly disingenuous.

From these highly contestable propositions – that the economy has returned to growth and the Government is not actually pursuing austerity – the Minister takes critical aim. But it is not clear exactly who he is aiming at. First, he claims:

‘It is perplexing then to see a problem of this scale (the deficit) effectively dismissed by the suggestion that there is a better, simpler, pain-free way.’

Clearly, this does not refer to the open letter which sets out a very rational approach to fiscal consolidation – ‘smart’ or ‘growth-friendly’ fiscal consolidation:

‘Such an investment programme must be accompanied by “smart” fiscal consolidation, focusing on the least contractionary forms of fiscal adjustment. This requires progressive and equality-proofed taxation targeting high-income groups, property assets, unproductive activity and passive income, as well as environmental measures.’

I doubt there is any Government minister that would disagree with this formulation. And this certainly doesn’t suggest ‘a simpler, pain-free way’ – though it does suggest a ‘better’ way.

Ultimately, the issue is not whether there should be fiscal consolidation or whether it should be pain-free, but what is the most effective and efficient means. According to the ESRI, spending cuts are the least efficient and effective means of deficit reduction for the reason that they most contractionary forms of adjustment. Again, the Minister would be aware of this research – and the common sense behind it.

It also overlooks the fact that investment itself is an effective means of deficit reduction. Putting people back to work, increasing the productive capacity to grow cuts both the general and the structural deficit. In this regard, the Nevin Economic Research Institute’s (NERI) recent report puts the growth potential of investment in perspective.

Second, the Minister claims:

‘The idea that we would use all of our available resources in an all-or-nothing attempt to kick-start the economy strikes me as more Fianna Fáil circa 1977 than John Maynard Keynes, bearing in mind that the sum mentioned, €15 billion, equates to approximately one year’s exchequer borrowing requirement, money borrowed to pay day-to-day costs.’

There is, of course a difference between Fianna Fail’s economic adventurism and the investment-based approach advanced in the open letter. In the late 1970s Fianna Fail gambled that cutting taxation and boosting Government consumption would lead to increased consumer spending. As a result, the indigenous private sector would expand to meet growth among indigenous firms which they assumed would respond with a surge of expansion. This didn’t happen, of course; all we got was the stagflation of the 1980s.

The open letter strategy, however, is to address the economic and social deficits through investment which will grow the productive capacity - a strategy completely at odds with the badly misjudged Fianna Fail strategy of pump-priming consumer expenditure.

In this context, the ‘all or nothing’ reference is curious: it is hardly ‘all or nothing’ to roll out a next generation broadband, to invest in education from pre-primary to lifelong learning, to modernise our water & waste system. This is not about kick-starting, it is about creating new assets that will generate income and reduce spending in the future.

The phrase ‘silver bullet’ only reinforces the notion that the Minister was debating other positions. Even the reference to the ‘€15 billion’: the open letter didn’t propose a €15 billion programme (though NERI has). It merely outlined the sources where investment could commence – the €5 billion in the pension fund, the €15 billion in cash balances, the use of public enterprises’ commercial potential. Regarding the cash balances, even the Government has admitted that using €6 billion of this amount to write-down debt would still leave the balance ‘relatively healthy’. Why not redirect this amount into building our productive capacity?

While it is welcome that the Minister has publicly engaged with the open letter, it is disappointing that he argued from highly contestable premises while failing to address the real and practical propositions that the letter put forward. We are still left with the need for the Government to actually put forward concrete evidence that spending-based fiscal contraction is economically efficient; that privatisation will enhance our net investment position; that an economy that has returned to recession and suffering from rising joblessness and poverty can somehow, at the same time, repair its public finances.

We are still left with the need for the Government to admit that its austerity strategy is not going as planned and, therefore, that it is willing to canvas alternatives.

The first problem we confront is a disconnect between what the Minister claims and what is actually happening in the economy. He states:

‘The importance of growth is factored into our budgetary figures. Our own economy has returned to modest growth and indeed, the greatest impediment to future growth is the state of the global economy.’

The problem here is that the economy has actually returned to recession – a double-dip recession. The latest quarterly data we have – from the second half of last year – shows GDP in decline. When we turn to the domestic economy, we find the biggest fall since the dark days of 2009. It is difficult to reconcile the statement ‘our own economy has returned to modest growth’ with the fact that we are back in recession.

The second problem is a denial of what the Government is actually doing.

‘Contrary to the view articulated (by the contributors), the Government is not pursuing an “austerity” strategy. The opposite is the case.’

Again, it is hard to reconcile this with what the current Government is doing. In the last budget, the Government engaged in a fiscal contraction equivalent to €4.3 billion (according to the EU Commission, factoring in the carryover from Budget 2011). This was made up of tax increases – primarily regressive VAT increases – and spending cuts, in particular a significant €750 million capital investment cut.

This will have a profound impact, not only on the social fabric, but on economic growth. The Minister for Finance has estimated that for every €1 billion in cuts/tax increases, the GDP falls by €500 million. On this basis, the Government reduced growth by €2.15 billion or over 1 percent off real GDP.

It is worth noting that the Government is now at pains to distance itself from the word ‘austerity’ – such is the low esteem it is now held among people since it is a by-word for low-growth, job losses and rising debt. However, to maintain that you are not pursuing austerity while at the same time doing just that is slightly disingenuous.

From these highly contestable propositions – that the economy has returned to growth and the Government is not actually pursuing austerity – the Minister takes critical aim. But it is not clear exactly who he is aiming at. First, he claims:

‘It is perplexing then to see a problem of this scale (the deficit) effectively dismissed by the suggestion that there is a better, simpler, pain-free way.’

Clearly, this does not refer to the open letter which sets out a very rational approach to fiscal consolidation – ‘smart’ or ‘growth-friendly’ fiscal consolidation:

‘Such an investment programme must be accompanied by “smart” fiscal consolidation, focusing on the least contractionary forms of fiscal adjustment. This requires progressive and equality-proofed taxation targeting high-income groups, property assets, unproductive activity and passive income, as well as environmental measures.’

I doubt there is any Government minister that would disagree with this formulation. And this certainly doesn’t suggest ‘a simpler, pain-free way’ – though it does suggest a ‘better’ way.

Ultimately, the issue is not whether there should be fiscal consolidation or whether it should be pain-free, but what is the most effective and efficient means. According to the ESRI, spending cuts are the least efficient and effective means of deficit reduction for the reason that they most contractionary forms of adjustment. Again, the Minister would be aware of this research – and the common sense behind it.

It also overlooks the fact that investment itself is an effective means of deficit reduction. Putting people back to work, increasing the productive capacity to grow cuts both the general and the structural deficit. In this regard, the Nevin Economic Research Institute’s (NERI) recent report puts the growth potential of investment in perspective.

Second, the Minister claims:

‘The idea that we would use all of our available resources in an all-or-nothing attempt to kick-start the economy strikes me as more Fianna Fáil circa 1977 than John Maynard Keynes, bearing in mind that the sum mentioned, €15 billion, equates to approximately one year’s exchequer borrowing requirement, money borrowed to pay day-to-day costs.’

There is, of course a difference between Fianna Fail’s economic adventurism and the investment-based approach advanced in the open letter. In the late 1970s Fianna Fail gambled that cutting taxation and boosting Government consumption would lead to increased consumer spending. As a result, the indigenous private sector would expand to meet growth among indigenous firms which they assumed would respond with a surge of expansion. This didn’t happen, of course; all we got was the stagflation of the 1980s.

The open letter strategy, however, is to address the economic and social deficits through investment which will grow the productive capacity - a strategy completely at odds with the badly misjudged Fianna Fail strategy of pump-priming consumer expenditure.

In this context, the ‘all or nothing’ reference is curious: it is hardly ‘all or nothing’ to roll out a next generation broadband, to invest in education from pre-primary to lifelong learning, to modernise our water & waste system. This is not about kick-starting, it is about creating new assets that will generate income and reduce spending in the future.

The phrase ‘silver bullet’ only reinforces the notion that the Minister was debating other positions. Even the reference to the ‘€15 billion’: the open letter didn’t propose a €15 billion programme (though NERI has). It merely outlined the sources where investment could commence – the €5 billion in the pension fund, the €15 billion in cash balances, the use of public enterprises’ commercial potential. Regarding the cash balances, even the Government has admitted that using €6 billion of this amount to write-down debt would still leave the balance ‘relatively healthy’. Why not redirect this amount into building our productive capacity?

While it is welcome that the Minister has publicly engaged with the open letter, it is disappointing that he argued from highly contestable premises while failing to address the real and practical propositions that the letter put forward. We are still left with the need for the Government to actually put forward concrete evidence that spending-based fiscal contraction is economically efficient; that privatisation will enhance our net investment position; that an economy that has returned to recession and suffering from rising joblessness and poverty can somehow, at the same time, repair its public finances.

We are still left with the need for the Government to admit that its austerity strategy is not going as planned and, therefore, that it is willing to canvas alternatives.

Wednesday, 28 March 2012

Welcome to the inequality cycle

Michael Taft: We are now starting to get data to assess just who in society is getting hit and who is getting by. Of course, we know about unemployment rates, deprivation rates, and income inequality rates. But the CSO’s 2010 Survey of Income and Living Conditions gives us an insight as to who has lost how much in the first two years of the crisis, namely 2009 and 2010. Let’s take a particular look at three deciles – the lowest, the highest and the middle 6th decile.

First, what levels of income are we discussing within these groups?

• The lowest decile includes households with gross incomes of less than €13,249 or less; or approximately €10,000 per adult in the household.

• The middle decile includes households with gross incomes between €37, 467 and €46,561; or approximately between €18,000 and €21,000 per adult in the household. (Question: is this the squeezed middle that the Irish Times series was recently chronicling?).

• The average for the highest household is a gross income of over €171,000; or approximately €62,000 per adult in the household.