An Saoi: The Department of Finance has issued the February 2012 tax figures, which can be viewed here. The figures are so confusing a detailed explanatory note has been issued to explain the discrepancies.

Let us start with the headline figure. It is 12.53% over profile. However we now have three different explanations as to why the figures are so far over target.

a) Corporation Tax which came in too late for inclusion in 2011. See here for an explanation – discrepancy €261M

b) Corporation Tax refunds not processed - discrepancy €50m?

c) 2011 Income Tax, wrongly accounted for as Social Insurance – discrepancy €350M estimated (see below for explanation)

This gives a total discrepancy of around €661M and reduces the total from €5,891M to €5,230M or close to the expected target €5,237M.

Firstly in looking at the Income Tax figures, let us start with the Social Insurance Fund. The estimated yield for the SIF in 2011 was €7,148M while the outcome was €7,543M, a discrepancy of €395M. Income Tax for 2011 was €327M below target. Income tax began falling behind profile in the latter half of the year and it completely beggars belief that the Collector General and his staff were not aware of the movement in the two, Social Insurance over target and Income Tax below target by a very similar amount. It is unbelievable that they had to wait until the filing of forms P35 to discover the discrepancy. Anyone who has any experience of Revenue computer systems and its Management Information Systems knows that this discrepancy would have been picked up. While as the Department correctly points out that it doesn’t change the overall position, it does improve the tax position for 2012 while weakening the Social Insurance Fund. Effectively a lump of 2011 Income Tax was hidden as Social Insurance in 2011 and that money is now being taken back in 2012.

By taking this action, the position of the Social Insurance Fund has been considerably weakened. The size of the deficit in the SIF will be far greater than originally expected. In a classic neo-liberal tactic, are we about to see the State's financial hole depicted as the fault of Welfare spending, allowing it to be targeted in to bear most of the cuts for 2013?

The complete opposition of Dept of Finance to the Insurance principle and the opposition of Fine Gael to the extension of Social Insurance to other sources of income further weakens the position of the Social Insurance Fund.

Many questions were raised about the Income Tax target at Budget time. We now of course know why the Minister for Finance was so sure that the figure would be reached. Apart from the pensioners, he had this €300M tucked away. He also has a once off bonus of several hundred million Euro coming his way later in the year. Facebook’s Irish staff will be receiving their Restricted Stock Units some six months after the Initial Public Offering and with nearly 10% of their worldwide staff here, there should be lots of additional tax due. The Financial Times recently estimated that the total value of these RSUs will be in the region of $23,000M, with the tax due on vesting.

There should also be a substantial yield from a further investigation relating to those receiving foreign pensions, as described by Niamh Connolly in the Sunday Business Post on 19th February last.

Income Tax looks likely to well exceed its annual target for 2012.

Moving on to Value Added Tax, the target for the month was €220M net. The State received €194M net or just 88.2% of its target, which is only four weeks old. March’s figures which will cover the Jan/Feb period will reflect the cold blast of the retail sales decline and is highly unlikely to get anywhere near target.

Excise figures were €14M off reflecting the problems in the motor trade. It is unclear whether this is a temporary blip or something more permanent. Finance for the purchase of new cars is readily available to the solvent customers, both from the specialist lenders owned by the motor groups and from Credit Unions.

The inability to process CT repayments in a timely manner reflects the loss of staff. Taxpayers are going to have to get used to this as it will become the norm.

The other tax heads show figures on or very close to target.

The real story however is the further evidence of the cynical manipulation of tax figures to ensure that the 2012 figures look good. First, the movement of corporation tax from December to January and now we hear about this problem with income tax. One wonders what else has fallen down behind the sofa cushions?

Showing posts with label exchequer returns. Show all posts

Showing posts with label exchequer returns. Show all posts

Tuesday, 6 March 2012

Friday, 3 February 2012

January 2012 tax - have we reached the bottom?

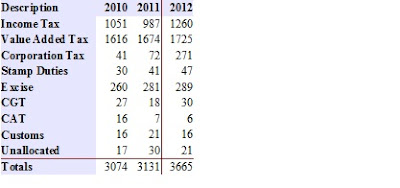

An Saoi: The January tax figures have given the Government a bit of good news, but the question is how much?

The Table below gives the figures for January from 2010 to 2012 and superficially the figures look like a big improvement and certainly some particular tax heads look particularly good.

The Income Tax is well ahead over previous years mainly because the payments relate to 2011 and are influenced by the Brian Lenihan changes and weekly paid staff had an additional payday in December, a Week 53, which added to the tax yield. The income tax figures for the last four months of 2011 were well behind target and perhaps there is a degree of balancing payments being submitted with forms P35. The weakness of Income Tax in 2011 may have been overstated and was perhaps a cashflow issue for employers.

The Corporation Tax figure must be a serious worry to the Government. It includes €261M which they told us really belonged in December 2011 but arrived late. This suggests that the net figure for January was just €10M. It will be May before enough is known to hazard a guess at the final outcome.

Value Added Tax is up €51M on the same period and reflects the better weather in November and December 2011 over the previous year and perhaps a degree of shopping ahead of the increase in the standard rate of VAT which took effect from 1st January. The Retail Sales Figures released by the CSO suggest that the motor trade performed strongly in December. The slight increase in Excise Figures confirms this also.

The other taxes, even together, do not amount to very much and are not really worth a comment for a few more months. It will be March before we can see a definite trend, but on these figures, the Government has a chance of reaching its targets.

The Table below gives the figures for January from 2010 to 2012 and superficially the figures look like a big improvement and certainly some particular tax heads look particularly good.

The Income Tax is well ahead over previous years mainly because the payments relate to 2011 and are influenced by the Brian Lenihan changes and weekly paid staff had an additional payday in December, a Week 53, which added to the tax yield. The income tax figures for the last four months of 2011 were well behind target and perhaps there is a degree of balancing payments being submitted with forms P35. The weakness of Income Tax in 2011 may have been overstated and was perhaps a cashflow issue for employers.

The Corporation Tax figure must be a serious worry to the Government. It includes €261M which they told us really belonged in December 2011 but arrived late. This suggests that the net figure for January was just €10M. It will be May before enough is known to hazard a guess at the final outcome.

Value Added Tax is up €51M on the same period and reflects the better weather in November and December 2011 over the previous year and perhaps a degree of shopping ahead of the increase in the standard rate of VAT which took effect from 1st January. The Retail Sales Figures released by the CSO suggest that the motor trade performed strongly in December. The slight increase in Excise Figures confirms this also.

The other taxes, even together, do not amount to very much and are not really worth a comment for a few more months. It will be March before we can see a definite trend, but on these figures, the Government has a chance of reaching its targets.

Friday, 6 January 2012

End of year Exchequer Returns 2011

An Saoi: You can read the Government's gloss on 2011's awful tax figures here (Slides 5-7). The tax yield has indeed risen but only after

• the reclassification of the Health Levy as a tax within the USC

• substantial cuts in various tax credits

• the introduction of various new levies

After the massive changes introduced the figures still were €873M short of target. We are told that €261M in Corporation Tax arrived “late” and the Dept. of Finance have decided to “adjust” the figures accordingly. Now late payment of tax is regularly occurs, but this is the first time any Government has decided to make such adjustment. I understand the reason for the late payment was a delay in transferring the tax due from a UK account, because of course the multi-national involved does not trust the Irish banking system. While it may account for its sales in Ireland it sure as hell will ensure that its cash is not here!

Let us look at the main figures, starting with Value Added Tax. Yield is down €489M from target or 4.8% & €360M short of the 2010 figure. The VAT yield weakened throughout the year, reflecting insipid consumer activity, which will it is forecast continue into 2012. The number of credit cards and their use continues to plummet, suggesting even those who can afford to spend do are not listening to Michael Noonan's plea that they spend, rather they believe "Ireland is facing 10 years of austerity" , as Dr. Richard Tol so succinctly put it as he flees the island.

The withdrawal of income involved in the Budget changes will lead to a drop in the VAT yield, which the Government has implicitly taken into account in its tax projections for 2012 by accepting that the VAT rate increase will yield far less than would be expected. The actual affects of the Budget changes were not broken down in the Budget documents.

The degree of non payment or late payment is also not detailed though the Revenue Commissioners are promising to specifically target collection as part of its Comprehensive Expenditure Review. However the graph below shows the level of change in VAT in just five years. Click on graphics to enlarge.

Income Tax came in €327M below target for 2011, but is of course not properly comparable with previous years because of the USC. The real challenge is 2012 particularly since the yield from Income Tax actually weakened in December against the Minister's estimate at Budget time, just four weeks ago. Budget papers expected the 2012 yield to increase by €1,202M (8.7%) over the 2011 outturn and looks well nigh impossible. This surely will be clear by the end of March or April, leaving a mini-Budget inevitable.

The position of the two capital taxes, Capital Acquisitions Tax & Capital Gains Tax from 2006 to 2012 is mapped on the chart below (CGT LHS & CAT RHS). Both taxes performed reasonably well in 2011, CGT considerably exceeding its target as many people took advantage of the existing rate, before the Budget increase to 30%. The various changes introduced by the late Brian Lenihan to CAT ensured that the outturn was only marginally below the expected yield. Further changes introduced in the 2012 Budget are expected to increase the yield further. Irish CAT relief, in particular the provisions on agricultural and business transfers are extremely generous. There are huge options to increase the yield from this source without damaging economic activity.

The lack of access to cash to fund purchases whether it is property or business assets leaves the position of CGT particularly problematic.

“Stamp Duties” are now mainly made up of various levies on pensions, insurance policies etc. The historcial sources of property and financial documents are now but a small part of the yield. A breakdown of the various sources up to 2009 is available from the Revenue Commissioners here and in a written answer provided to a well-known cloth cap you can see the 2010 property figures yield. There is little or no logic to many of these ad hoc taxes, other than to fill some financial hole quickly and their efficacy needs to be reviewed urgently. In the meantime they yielded €1,391M in 2011.

Excise Duties also covers a wide range of different fees and flat rate charges and taxes on services and goods, details of which are available from this chapter of the Revenue Commissioners Annual Statistical Report and came in bang on target as the forecasting is not done by the Dept. Of Finance! The yield is the same as in 2010 and the expected increase in 2012 is just €125M, an increase of under 3% and 2012 should come in on target.

Finally Corporation Tax. This is not so much a tax any more as a voluntary contribution from multi-nationals. The yield from this source is still impressive at €3,520M in 2011, if only just over half €6,683M paid in 2006.Unfortunately much of the tax paid in the glory years of 2006 & 2007 has been repaid since as huge losses incurred in the financial service and property industries have been offset against earlier profits. The 2011 figure was €500M short on target. However they claim to have €261M already in the bank, which should help to make reaching the target of €3,770M a little easier.

Conclusion: 2011 was a bad tax year. An economy on short-time with little access to cash was always going to be that way. The issue now is 2012. It is impossible to see the Government reaching the intended target for 2012 without some form of increased economic activity. This may be clear very quickly, as early as March or April.

A further year of economic stagnation lies ahead and Economist Meg of Roubini Global Economics thinks we are in serious trouble and I agree. However we got ourselves into this problem and it is up to ourselves to dig ourselves out of it.

The additional taxes required to bring the figure up to €36,250M as required by the Government would need to be carefully selected if they are not to seriously reduce existing taxes. Blunt tools such as a VAT rate increase, raising duties on tobacco products & alcohol are unlikely to raise additional taxes as they are likely to lead to lower consumption where they cannot be avoided or increased traffic North or smuggling.

Expediting the withdrawal of the property tax breaks which played a major part in getting us into our current difficulties could yield in excess of €1,000M. These would include a “use it or lose it” amendment, ending all of these capital allowance schemes with effect 31st December 2011 and allowing no further carry forward of unused capital allowances or losses created by them after that date. Also the deductibility of interest against all rental income should be ended with effect from 31st December 2011. The withdrawal of tax expenditures would be the most effective way of collecting the money and have the least effect on private consumption.

Enforcement of existing legislation and the collection of taxes as they fall due is also crucial. The Revenue will be particularly badly hit over the next few months by retirements because of the organisation's age structure. Additional Revenue staff not just replacements for those leaving are required to ensure compliance. Sadly this will not be happening. Indeed, one Commissioner is leaving.

A little bit of joined up thinking is required, but it is as seriously lacking in our current Government as in the one that it replaced. God help us.

• the reclassification of the Health Levy as a tax within the USC

• substantial cuts in various tax credits

• the introduction of various new levies

After the massive changes introduced the figures still were €873M short of target. We are told that €261M in Corporation Tax arrived “late” and the Dept. of Finance have decided to “adjust” the figures accordingly. Now late payment of tax is regularly occurs, but this is the first time any Government has decided to make such adjustment. I understand the reason for the late payment was a delay in transferring the tax due from a UK account, because of course the multi-national involved does not trust the Irish banking system. While it may account for its sales in Ireland it sure as hell will ensure that its cash is not here!

Let us look at the main figures, starting with Value Added Tax. Yield is down €489M from target or 4.8% & €360M short of the 2010 figure. The VAT yield weakened throughout the year, reflecting insipid consumer activity, which will it is forecast continue into 2012. The number of credit cards and their use continues to plummet, suggesting even those who can afford to spend do are not listening to Michael Noonan's plea that they spend, rather they believe "Ireland is facing 10 years of austerity" , as Dr. Richard Tol so succinctly put it as he flees the island.

The withdrawal of income involved in the Budget changes will lead to a drop in the VAT yield, which the Government has implicitly taken into account in its tax projections for 2012 by accepting that the VAT rate increase will yield far less than would be expected. The actual affects of the Budget changes were not broken down in the Budget documents.

The degree of non payment or late payment is also not detailed though the Revenue Commissioners are promising to specifically target collection as part of its Comprehensive Expenditure Review. However the graph below shows the level of change in VAT in just five years. Click on graphics to enlarge.

Income Tax came in €327M below target for 2011, but is of course not properly comparable with previous years because of the USC. The real challenge is 2012 particularly since the yield from Income Tax actually weakened in December against the Minister's estimate at Budget time, just four weeks ago. Budget papers expected the 2012 yield to increase by €1,202M (8.7%) over the 2011 outturn and looks well nigh impossible. This surely will be clear by the end of March or April, leaving a mini-Budget inevitable.

The position of the two capital taxes, Capital Acquisitions Tax & Capital Gains Tax from 2006 to 2012 is mapped on the chart below (CGT LHS & CAT RHS). Both taxes performed reasonably well in 2011, CGT considerably exceeding its target as many people took advantage of the existing rate, before the Budget increase to 30%. The various changes introduced by the late Brian Lenihan to CAT ensured that the outturn was only marginally below the expected yield. Further changes introduced in the 2012 Budget are expected to increase the yield further. Irish CAT relief, in particular the provisions on agricultural and business transfers are extremely generous. There are huge options to increase the yield from this source without damaging economic activity.

The lack of access to cash to fund purchases whether it is property or business assets leaves the position of CGT particularly problematic.

“Stamp Duties” are now mainly made up of various levies on pensions, insurance policies etc. The historcial sources of property and financial documents are now but a small part of the yield. A breakdown of the various sources up to 2009 is available from the Revenue Commissioners here and in a written answer provided to a well-known cloth cap you can see the 2010 property figures yield. There is little or no logic to many of these ad hoc taxes, other than to fill some financial hole quickly and their efficacy needs to be reviewed urgently. In the meantime they yielded €1,391M in 2011.

Excise Duties also covers a wide range of different fees and flat rate charges and taxes on services and goods, details of which are available from this chapter of the Revenue Commissioners Annual Statistical Report and came in bang on target as the forecasting is not done by the Dept. Of Finance! The yield is the same as in 2010 and the expected increase in 2012 is just €125M, an increase of under 3% and 2012 should come in on target.

Finally Corporation Tax. This is not so much a tax any more as a voluntary contribution from multi-nationals. The yield from this source is still impressive at €3,520M in 2011, if only just over half €6,683M paid in 2006.Unfortunately much of the tax paid in the glory years of 2006 & 2007 has been repaid since as huge losses incurred in the financial service and property industries have been offset against earlier profits. The 2011 figure was €500M short on target. However they claim to have €261M already in the bank, which should help to make reaching the target of €3,770M a little easier.

Conclusion: 2011 was a bad tax year. An economy on short-time with little access to cash was always going to be that way. The issue now is 2012. It is impossible to see the Government reaching the intended target for 2012 without some form of increased economic activity. This may be clear very quickly, as early as March or April.

A further year of economic stagnation lies ahead and Economist Meg of Roubini Global Economics thinks we are in serious trouble and I agree. However we got ourselves into this problem and it is up to ourselves to dig ourselves out of it.

The additional taxes required to bring the figure up to €36,250M as required by the Government would need to be carefully selected if they are not to seriously reduce existing taxes. Blunt tools such as a VAT rate increase, raising duties on tobacco products & alcohol are unlikely to raise additional taxes as they are likely to lead to lower consumption where they cannot be avoided or increased traffic North or smuggling.

Expediting the withdrawal of the property tax breaks which played a major part in getting us into our current difficulties could yield in excess of €1,000M. These would include a “use it or lose it” amendment, ending all of these capital allowance schemes with effect 31st December 2011 and allowing no further carry forward of unused capital allowances or losses created by them after that date. Also the deductibility of interest against all rental income should be ended with effect from 31st December 2011. The withdrawal of tax expenditures would be the most effective way of collecting the money and have the least effect on private consumption.

Enforcement of existing legislation and the collection of taxes as they fall due is also crucial. The Revenue will be particularly badly hit over the next few months by retirements because of the organisation's age structure. Additional Revenue staff not just replacements for those leaving are required to ensure compliance. Sadly this will not be happening. Indeed, one Commissioner is leaving.

A little bit of joined up thinking is required, but it is as seriously lacking in our current Government as in the one that it replaced. God help us.

Thursday, 3 November 2011

Spinning our tax wheels

Michael Taft: The Exchequer statement out yesterday shows tax revenue falling short of target. The headline rate shows tax revenue at end October falling €184 million, or 0.7 percent, below profile. However, when we dig deeper into the numbers, there is a more depressing message coming through; namely, that we are spinning our wheels in a deflationary ditch despite Government moves to boost revenue.

While tax revenue falls short of targets, when we compare with last year, revenue has increased by nearly €2 billion, or 8 percent. Or has it? The Universal Social Charge, which is counted in the income tax category, includes the Health Levy which it replaced. However, last year the Health Levy was not counted as revenue; rather, it was counted as a Departmental Balance and would have been subsumed under Net Expenditure. So to get a proper read, we have to factor in this accounting change.

According to the Minister for Health, €1,422 million in Health levies was collected up to the end of October last year. When accounting for that we find that:

Tax Revenue is only €552 million ahead of last year (not the €2 billion shown in the Exchequer statement and reproduced in media reports).

This means tax revenue is only 2.2 percent of target, not 8 percent as reported. However, there is more. Since the targets were set, changes were introduced in the Jobs Initiative in May. The main changes that concern us here are the reduction in the VAT rate and the new Pension Levy. The Pension Levy has raised €490 million (under the Stamp Duty heading) which was not envisaged when the targets were set. As well, the reduction in the VAT rate is estimated to cost €120 million in 2011.

For the purposes of the following exercise I have assumed that the VAT rate reduction has cost the Exchequer €80 million to end-October. If these changes weren’t made we might find that tax revenue would have only been €142 million ahead of last year – or about a ½ percent.

When we compare this year’s outturn with the targets, assuming these changes weren’t made (the targets haven’t changed to accommodate these new measures) we find that tax revenue falls €594 million below target – or 2.2 percent below target.

Whichever comparison we use, once we have factored in Health Levy, reduction in the VAT rate and the new Pension Levy, tax revenue is disappointing – barely above last year’s outturn and below targets. But we have to set this in context.

In Budget 2011, the Government introduced new tax measures designed to raise €1,406 million in 2011. The big ticket items were also regressive: cutting personal tax credits and cutting the standard rate tax band (€830 million).

So the Government increased taxation by €1.4 billion and during the year increased taxation again by over €400 million. And, yet, tax revenue is under-performing, barely lifting itself above last year’s level.

This is a sign, not of an economy recovering, but of an economy spinning its wheels in a deflationary ditch.

While tax revenue falls short of targets, when we compare with last year, revenue has increased by nearly €2 billion, or 8 percent. Or has it? The Universal Social Charge, which is counted in the income tax category, includes the Health Levy which it replaced. However, last year the Health Levy was not counted as revenue; rather, it was counted as a Departmental Balance and would have been subsumed under Net Expenditure. So to get a proper read, we have to factor in this accounting change.

According to the Minister for Health, €1,422 million in Health levies was collected up to the end of October last year. When accounting for that we find that:

Tax Revenue is only €552 million ahead of last year (not the €2 billion shown in the Exchequer statement and reproduced in media reports).

This means tax revenue is only 2.2 percent of target, not 8 percent as reported. However, there is more. Since the targets were set, changes were introduced in the Jobs Initiative in May. The main changes that concern us here are the reduction in the VAT rate and the new Pension Levy. The Pension Levy has raised €490 million (under the Stamp Duty heading) which was not envisaged when the targets were set. As well, the reduction in the VAT rate is estimated to cost €120 million in 2011.

For the purposes of the following exercise I have assumed that the VAT rate reduction has cost the Exchequer €80 million to end-October. If these changes weren’t made we might find that tax revenue would have only been €142 million ahead of last year – or about a ½ percent.

When we compare this year’s outturn with the targets, assuming these changes weren’t made (the targets haven’t changed to accommodate these new measures) we find that tax revenue falls €594 million below target – or 2.2 percent below target.

Whichever comparison we use, once we have factored in Health Levy, reduction in the VAT rate and the new Pension Levy, tax revenue is disappointing – barely above last year’s outturn and below targets. But we have to set this in context.

In Budget 2011, the Government introduced new tax measures designed to raise €1,406 million in 2011. The big ticket items were also regressive: cutting personal tax credits and cutting the standard rate tax band (€830 million).

So the Government increased taxation by €1.4 billion and during the year increased taxation again by over €400 million. And, yet, tax revenue is under-performing, barely lifting itself above last year’s level.

This is a sign, not of an economy recovering, but of an economy spinning its wheels in a deflationary ditch.

Monday, 11 July 2011

June tax figures

An Saoi: The half year tax figures came out during the week and there have been various comments published around them. Constantin Gurdgiev’s piece is available here and is full of nice colourful graphs and gives a multi-year view of payments. I want to focus in on just two of the tax heads, Corporation Tax & Income Tax this month. Both suggest trouble ahead.

Corporation Tax paid in June was €824M net against a monthly target or profile of €871M. This follows on the May when €310M net against the profile figure €450M. All companies have now made the first of their two Corporation Tax payments and the Revenue now have all of the information required to figures are extremely worrying.

The figure is also well below the cumulative figure at June 2010 €1,424M against €1,610M. The 2010 figure would surely have been heavily influenced by refunds arising from losses made by companies in their trading years 2008 & 2009. This makes the continued slippage in 2011 even more alarming and suggests that the final CT figure for 2011 will hardly break €3,400M or around €600M below profile. Back in April after the March tax returns, I had expected Corporation Tax figures to come in at €4,800M, well ahead of profile. This projection was based on the level of trading of many International firms with large presences in Ireland. All of these companies have now at least part paid their current liabilities and there is no way the Exchequer will get close to its target.

We know that the level of trading losses within the financial services industry was at least €34,309M arising from a Dail question. The only journalist to pick up the importance of the story was Kathleen Barrington here in the Sunday Business Post. The level of payments being made by the historically large payers outside of the financial services sector must also be falling, suggesting greater internal pressure to reduce the tax cost of doing business in Ireland. Even 12.5% is too high. This is despite increasing profitability and turnover in those companies.

Few Valued Added Tax returns fall due in June and the overall level of payments for the month was small. However the figure €208M was €42M or 16.8% short of profile. However timing of refunds may explain such a large discrepancy.

The May/June VAT returns are due this month (July) and should be reasonably good. June was the last month and as can be seen from these SIMI Stats, it was a good month in the motor trade. However the rest of year will surely be poor as over 40% of car sales were part of the scrappage scheme. Preliminary retail sales figures for May showed non motor trade spending continues to fall. This would suggest that VAT for the year is unlikely to break €10,000M for the year, probably coming in somewhere between €9,600M & €9,800M.

Income Tax incorporating the USC remains on target. While it is nominally ahead of last year, when you take the substantial tax changes in the Finance Act and the replacement of the Health Levy with the USC, it is behind perhaps €300M against the same month last year on a like for like basis. There is an expectation of increased income tax payments for the rest of the year, which seems more of a hope than expectation, but only time will tell. Employment and wage levels continue to fall but perhaps self employed payments will bail the State out later in the year?

Excise Duty remains ahead of target buoyed by the new car sales. The next six months may reflect a different story. Stamp duty remains in the doldrums.

Movements in the other taxes do not materially change the picture as their collective contribution is so small. Customs Duties are collected by the State on behalf of the European Union and while included in the figures are remitted to the EU, minus 40% to cover local costs.

The final outcome suggests that the cumulative tax changes introduced by the outgoing Government have not improved the Exchequer position. Retail activity other than in the car trade continues to fall and with the tax take following suit. The fall in Corporation Tax was not expected, least of all by me and shows just how fickle the multi national sector’s relationship with Ireland is.

June’s figures may also explain Mr. Noonan’s comments about the necessity to find even more than the €3,600M in planned cuts. It would be helpful if he let us all in on the information he has been given by his officials. The final tax yield for 2011 looks as it will fall a good deal short of the €34,900M.

There is an urgent need to expand the Tax base and the Social Insurance base by withdrawing without delay all the various tax breaks, deductibility of interest against property purchase, carry forward of losses, exemptions applied to certain income etc.

The effects of the tax changes introduced this year also make it clear that there is a need to selectively reduce the tax burden but certainly not to increase rates. Proposed changes in the standard rate (21%) VAT rate should not be introduced under any circumstances and a substantial rowing back on the effects of individualisation should also be considered to protect the position of many one income households.

The need to get property related business costs down without delay needs to be tackled with the same alacrity as Richard Bruton has pursued the low paid.

Corporation Tax paid in June was €824M net against a monthly target or profile of €871M. This follows on the May when €310M net against the profile figure €450M. All companies have now made the first of their two Corporation Tax payments and the Revenue now have all of the information required to figures are extremely worrying.

The figure is also well below the cumulative figure at June 2010 €1,424M against €1,610M. The 2010 figure would surely have been heavily influenced by refunds arising from losses made by companies in their trading years 2008 & 2009. This makes the continued slippage in 2011 even more alarming and suggests that the final CT figure for 2011 will hardly break €3,400M or around €600M below profile. Back in April after the March tax returns, I had expected Corporation Tax figures to come in at €4,800M, well ahead of profile. This projection was based on the level of trading of many International firms with large presences in Ireland. All of these companies have now at least part paid their current liabilities and there is no way the Exchequer will get close to its target.

We know that the level of trading losses within the financial services industry was at least €34,309M arising from a Dail question. The only journalist to pick up the importance of the story was Kathleen Barrington here in the Sunday Business Post. The level of payments being made by the historically large payers outside of the financial services sector must also be falling, suggesting greater internal pressure to reduce the tax cost of doing business in Ireland. Even 12.5% is too high. This is despite increasing profitability and turnover in those companies.

Few Valued Added Tax returns fall due in June and the overall level of payments for the month was small. However the figure €208M was €42M or 16.8% short of profile. However timing of refunds may explain such a large discrepancy.

The May/June VAT returns are due this month (July) and should be reasonably good. June was the last month and as can be seen from these SIMI Stats, it was a good month in the motor trade. However the rest of year will surely be poor as over 40% of car sales were part of the scrappage scheme. Preliminary retail sales figures for May showed non motor trade spending continues to fall. This would suggest that VAT for the year is unlikely to break €10,000M for the year, probably coming in somewhere between €9,600M & €9,800M.

Income Tax incorporating the USC remains on target. While it is nominally ahead of last year, when you take the substantial tax changes in the Finance Act and the replacement of the Health Levy with the USC, it is behind perhaps €300M against the same month last year on a like for like basis. There is an expectation of increased income tax payments for the rest of the year, which seems more of a hope than expectation, but only time will tell. Employment and wage levels continue to fall but perhaps self employed payments will bail the State out later in the year?

Excise Duty remains ahead of target buoyed by the new car sales. The next six months may reflect a different story. Stamp duty remains in the doldrums.

Movements in the other taxes do not materially change the picture as their collective contribution is so small. Customs Duties are collected by the State on behalf of the European Union and while included in the figures are remitted to the EU, minus 40% to cover local costs.

The final outcome suggests that the cumulative tax changes introduced by the outgoing Government have not improved the Exchequer position. Retail activity other than in the car trade continues to fall and with the tax take following suit. The fall in Corporation Tax was not expected, least of all by me and shows just how fickle the multi national sector’s relationship with Ireland is.

June’s figures may also explain Mr. Noonan’s comments about the necessity to find even more than the €3,600M in planned cuts. It would be helpful if he let us all in on the information he has been given by his officials. The final tax yield for 2011 looks as it will fall a good deal short of the €34,900M.

There is an urgent need to expand the Tax base and the Social Insurance base by withdrawing without delay all the various tax breaks, deductibility of interest against property purchase, carry forward of losses, exemptions applied to certain income etc.

The effects of the tax changes introduced this year also make it clear that there is a need to selectively reduce the tax burden but certainly not to increase rates. Proposed changes in the standard rate (21%) VAT rate should not be introduced under any circumstances and a substantial rowing back on the effects of individualisation should also be considered to protect the position of many one income households.

The need to get property related business costs down without delay needs to be tackled with the same alacrity as Richard Bruton has pursued the low paid.

Saturday, 4 June 2011

May is a wicked month

An Saoi: The tax figures were released with a range of different views expressed. Read Dan O'Brien as an example of the general tenor of comment.

Thursday, 5 May 2011

April tax figures - not as good as they look

An Saoi: At an initial examination the April figures appear to be very good. However, at closer examination I think that there are a number of specific reasons - administrative and technical - explaining why the underlying figures tell another story.

The Income Tax figure looks excellent at first view. However, the estimate for April appears to have been far below the underlying liability. March involved five pay weeks for those paid weekly, and three pay fortnights. The estimate was just €1,080M - just €100M over the previous month, while €1,271M was actually paid. The profiler clearly did not get out his diary and calculate the full effect of the additional pay weeks.

Bi-monthly VAT returns are not due in April and the net VAT paid for April was €287M well in excess of €205M profiled. This is probably a reflection of delays in VAT repayment claims due to staff shortages, rather than additional taxes paid. The Revenue does not publish any details of repayment claims on hands at the end of the month therefore we can only guess what the actually position is. There have been strong rumours that the Revenue has been staggering large repayments over a longer period because of staffing and cashflow problems. The real test will occur with next month’s figures, which will include the March/April VAT returns. March spending on credit cards published by the Central Bank last week reflected very poor consumer activity in the month, and suggests that the VAT returns will be poor. Add to this the processing of the balance of the repayment claims arising from earlier periods and

Corporation Tax for the month was on target and remains ahead of target. May is a crucial month for Corporation Tax. Companies with account years ending 30th November & 30th June must make payments. In Ireland this includes Microsoft, Pfizer, Oracle & Diageo (Guinness). Last month I commented as follows on Corporation Tax,

“Little or no Corporation Tax is now paid by Irish owned businesses, while a very small proportion of the net yield is accounted for by those multi nationals actually trading in the Irish economy, e.g. Vodafone & O2. The increase in yield from Corporation Tax reflects the activities of multinationals in Ireland, using Ireland as their point of sale for goods and services. The annual target for Corporation Tax of €4,020M is likely to be comfortably exceeded. The net target for March was just €10M compared to €111M actually received. Such a monthly discrepancy needs some explanation, which was not forthcoming from Dept. of Finance.”

Corporation Tax bears no relation to actually Irish economic activity rather it is paid by multi-nationals for Ireland facilitating their activities.

Excise, which includes VRT is slightly below target in April (€406M versus profile €420M), however remains slightly ahead of target. Ongoing car sales are helping to keep figures up. The real test will occur after 30th June and the scrappage scheme ends. The continuing collapse of major garages such as Maxwell Motors would suggest that without this crutch, trade will collapse in the second half of the year.

Customs Duties are collected by the Irish Revenue on behalf of the European Union. The increase in yield is down to large multi-nationals using Ireland as their point of entry on imports from outside of the European Union and is irrelevant to the Irish Exchequer.

I made a technical error last month in relation to CAT which of course was brought into the pay and file system in Finance Act 2010. We will therefore have to wait until later in the year before we can make any real comparison. Stamp Duty & CGT are both running marginally below their very low targets.

However, I would hold with my tentative projection of March, which you can access here. Real cutbacks have not yet been felt, despite what people may think. Substantial losses of jobs will continue in the Public Sector and in Construction. The May figures should enable us to make more confident predictions for the final outcome.

The Income Tax figure looks excellent at first view. However, the estimate for April appears to have been far below the underlying liability. March involved five pay weeks for those paid weekly, and three pay fortnights. The estimate was just €1,080M - just €100M over the previous month, while €1,271M was actually paid. The profiler clearly did not get out his diary and calculate the full effect of the additional pay weeks.

Bi-monthly VAT returns are not due in April and the net VAT paid for April was €287M well in excess of €205M profiled. This is probably a reflection of delays in VAT repayment claims due to staff shortages, rather than additional taxes paid. The Revenue does not publish any details of repayment claims on hands at the end of the month therefore we can only guess what the actually position is. There have been strong rumours that the Revenue has been staggering large repayments over a longer period because of staffing and cashflow problems. The real test will occur with next month’s figures, which will include the March/April VAT returns. March spending on credit cards published by the Central Bank last week reflected very poor consumer activity in the month, and suggests that the VAT returns will be poor. Add to this the processing of the balance of the repayment claims arising from earlier periods and

Corporation Tax for the month was on target and remains ahead of target. May is a crucial month for Corporation Tax. Companies with account years ending 30th November & 30th June must make payments. In Ireland this includes Microsoft, Pfizer, Oracle & Diageo (Guinness). Last month I commented as follows on Corporation Tax,

“Little or no Corporation Tax is now paid by Irish owned businesses, while a very small proportion of the net yield is accounted for by those multi nationals actually trading in the Irish economy, e.g. Vodafone & O2. The increase in yield from Corporation Tax reflects the activities of multinationals in Ireland, using Ireland as their point of sale for goods and services. The annual target for Corporation Tax of €4,020M is likely to be comfortably exceeded. The net target for March was just €10M compared to €111M actually received. Such a monthly discrepancy needs some explanation, which was not forthcoming from Dept. of Finance.”

Corporation Tax bears no relation to actually Irish economic activity rather it is paid by multi-nationals for Ireland facilitating their activities.

Excise, which includes VRT is slightly below target in April (€406M versus profile €420M), however remains slightly ahead of target. Ongoing car sales are helping to keep figures up. The real test will occur after 30th June and the scrappage scheme ends. The continuing collapse of major garages such as Maxwell Motors would suggest that without this crutch, trade will collapse in the second half of the year.

Customs Duties are collected by the Irish Revenue on behalf of the European Union. The increase in yield is down to large multi-nationals using Ireland as their point of entry on imports from outside of the European Union and is irrelevant to the Irish Exchequer.

I made a technical error last month in relation to CAT which of course was brought into the pay and file system in Finance Act 2010. We will therefore have to wait until later in the year before we can make any real comparison. Stamp Duty & CGT are both running marginally below their very low targets.

However, I would hold with my tentative projection of March, which you can access here. Real cutbacks have not yet been felt, despite what people may think. Substantial losses of jobs will continue in the Public Sector and in Construction. The May figures should enable us to make more confident predictions for the final outcome.

Tuesday, 5 April 2011

March tax returns

An Saoi: The tax returns for March give us our first real feel for what is happening in the economy in 2011 through the bi-monthly VAT returns.

VAT paid in March covers the period January/ February and the VAT for November/ December was paid in January. Two of the six VAT returns due in the year have therefore been submitted and below is a comparison of VAT received for the first three months of each of the last nine years.

The figures would seem to suggest that VAT for the year is likely to fall quite a bit short of the projected figure of €10,230M. Figures for the first three months are inflated by the extension of the car incentive scheme which will end shortly. VAT payments in the first quarter normally account for around one third of annual VAT paid (31.84% (2010), 34.65% (2009), 33.71% (2008)). The underlying trend would seem to point towards VAT for the year of close to €9,500M.

The VAT figures should not come as a surprise to anyone and reflect the Retail Sales figures for January & February issued by the CSO on 28th March 2011 or the Central Bank’s Credit Card Statistics (Table A13) issued on 31st March. The real Irish economy remains in recession.

The Income Tax position also appears very problematic. The March figures were over 8.1% off the monthly target. This may be partly down to some technical explanation and if so should be corrected in the April figures. Tax deducted in March will be paid over in April and will include five weeks than the normal four and in the case of Public Sector workers, three pay fortnights rather than the normal two. However if the trend continues then the new Government will be in serious trouble.

Little or no Corporation Tax is now paid by Irish owned businesses, while a very small proportion of the net yield is accounted for by those multi nationals actually trading in the Irish economy, e.g. Vodafone & O2. The increase in yield from Corporation Tax reflects the activities of multinationals in Ireland, using Ireland as their point of sale for goods and services. The annual target for Corporation Tax of €4,020M is likely to be comfortably exceeded. The net target for March was just €10M compared to €111M actually received. Such a monthly discrepancy needs some explanation, which was not forthcoming from Dept. of Finance.

The Excise figure for March is slightly above profile, €367M against €350M. This reflects higher than expected car sales. However once the incentive scheme ends it may be difficult for the expected profile figures later in the year to be reached.

Capital Acquisitions Tax paid is just 45% of the amount paid at the same time last year, though strangely ahead of profile. The reduction in the thresholds should have gone some way to protecting the yield despite the decline in asset values.

The March returns suggest that the new Government will find it very difficult to achieve the tax figures set out just two months ago in February. Looking at the figures I would suggest the following as an early projection.

The continued deep recession in the domestic economy make it unlikely that the tax figures can be reached. If such a discrepancy arises, the Government will be under pressure to apply additional cuts to meet targets, sending the economy into a further spiral of decline.

The continued deep recession in the domestic economy make it unlikely that the tax figures can be reached. If such a discrepancy arises, the Government will be under pressure to apply additional cuts to meet targets, sending the economy into a further spiral of decline.

Pressure on households to reduce debt and the lack of access to any new credit will continue to inhibit consumer spending, even if customers wanted to spend. Income taxes will remain weak as employment numbers continue to fall. Any increases in employment numbers in the multinational sector will be swamped by the tsunami of job losses in the local economy

It is not a pretty picture.

VAT paid in March covers the period January/ February and the VAT for November/ December was paid in January. Two of the six VAT returns due in the year have therefore been submitted and below is a comparison of VAT received for the first three months of each of the last nine years.

The figures would seem to suggest that VAT for the year is likely to fall quite a bit short of the projected figure of €10,230M. Figures for the first three months are inflated by the extension of the car incentive scheme which will end shortly. VAT payments in the first quarter normally account for around one third of annual VAT paid (31.84% (2010), 34.65% (2009), 33.71% (2008)). The underlying trend would seem to point towards VAT for the year of close to €9,500M.

The VAT figures should not come as a surprise to anyone and reflect the Retail Sales figures for January & February issued by the CSO on 28th March 2011 or the Central Bank’s Credit Card Statistics (Table A13) issued on 31st March. The real Irish economy remains in recession.

The Income Tax position also appears very problematic. The March figures were over 8.1% off the monthly target. This may be partly down to some technical explanation and if so should be corrected in the April figures. Tax deducted in March will be paid over in April and will include five weeks than the normal four and in the case of Public Sector workers, three pay fortnights rather than the normal two. However if the trend continues then the new Government will be in serious trouble.

Little or no Corporation Tax is now paid by Irish owned businesses, while a very small proportion of the net yield is accounted for by those multi nationals actually trading in the Irish economy, e.g. Vodafone & O2. The increase in yield from Corporation Tax reflects the activities of multinationals in Ireland, using Ireland as their point of sale for goods and services. The annual target for Corporation Tax of €4,020M is likely to be comfortably exceeded. The net target for March was just €10M compared to €111M actually received. Such a monthly discrepancy needs some explanation, which was not forthcoming from Dept. of Finance.

The Excise figure for March is slightly above profile, €367M against €350M. This reflects higher than expected car sales. However once the incentive scheme ends it may be difficult for the expected profile figures later in the year to be reached.

Capital Acquisitions Tax paid is just 45% of the amount paid at the same time last year, though strangely ahead of profile. The reduction in the thresholds should have gone some way to protecting the yield despite the decline in asset values.

The March returns suggest that the new Government will find it very difficult to achieve the tax figures set out just two months ago in February. Looking at the figures I would suggest the following as an early projection.

Pressure on households to reduce debt and the lack of access to any new credit will continue to inhibit consumer spending, even if customers wanted to spend. Income taxes will remain weak as employment numbers continue to fall. Any increases in employment numbers in the multinational sector will be swamped by the tsunami of job losses in the local economy

It is not a pretty picture.

Thursday, 3 March 2011

The murky world of Exchequer statistics

Michael Taft: I don’t want to pre-empt An Saoi’s more informed analysis of Exchequer returns, but there are some real issues emerging even at this early stage of the year.

The Government is hoping to increase the overall Exchequer tax take by €3.1 billion, or 9.9 percent over last year. This is a key determinant to whether the deficit will fall to below -10 percent of GDP (other determinants are public expenditure and the overall level of GDP). This projected increase is made up of increases in the following sub-categories:

• Income tax (including USC): 25.3%

• VAT: 1.3%

• Corporation: 2.4%

• Customs & Excise: 0.1%

• Capital Taxes: 4.5%

The real driver in the projected increase is income tax revenue which includes receipts from the Universal Social Charge. This category is expected to make up over 90 percent of the entire projected tax increase. Of the projected increase of €3.1 billion, income tax/USC is expected to increase by over €2.8 billion.

Why the increase of 25 percent? It’s not because the economy is growing – more employment, more businesses, more tax revenue. The primary reasons are the income tax changes introduced in the budget (cuts in personal tax credits, standard rate tax band, certain tax reliefs, etc.); and the introduction of the USC.

And here is where it starts to get murky. The USC amalgamates the Income Levy and the Health Levy into new thresholds. While the income levy was included in income tax receipts last year, the health levy wasn’t; it was paid directly into the Department of Health and showed up as a Departmental Balance in the Estimates.

What this means is that comparisons between last year’s tax revenue (for both income tax and overall tax) are somewhat skewered since they are not comparing like with like. So when we get headlines like ‘Tax receipts up over 2 percent’ – we have to treat this carefully since last year’s tax receipts didn’t count the health levy which is now part of this year’s USC.

Of course, the Department of Finance could have made this all easier by putting in a like for like comparison. This would have meant taking last year’s figures and adding last year’s monthly receipts of the health levy. This has not been done and I can’t find these monthly figures for last year.

Last year the health levy was estimated to raise €2,431 million. This relates to full year increase. The comparator for this year would be less as January receipts relate to December payments. Therefore, February is the first month that we have to readjust to see how this year’s income tax receipts relate to last year.

• February 2011 income tax receipts: €980

• February 2010 income tax receipts: €784

This might suggest a substantial rise over last year (25 percent) but we have to include the February health levy receipts for 2010 – a figure not readily available. So here is an extrapolation: €186 million. When we add that to the overall February 2010 figure we find the following:

• February 2011 income tax receipts: €980

• February 2010 income tax receipts: €970 (including extrapolated health levy receipts)

The increase for February, therefore, is not 25 percent as the Finance numbers suggest but, rather, 1 percent – and this is with the additional revenue arising from other Budget 2011 changes.

Therefore, the overall tax receipts do not show a 2.2 percent increase over last year. Rather, it shows a -1.7 percent decline.

We should pause here. It is, as they say, early days and we shouldn’t rush to conclusions. But the early returns are not good. The second biggest category – VAT – is showing sluggish receipts so far. They are -2.4 percent down on last year’s outturn and -5.9 percent on the Government’s targets this year.

Throughout the year the important categories to watch are income tax and VAT (it would help if the Department of Finance produced comparable data). Together, they are projected to make up 70 percent of all tax receipts. These best reflect domestic economic activity; corporate tax receipts can reflect the accounting activities of the multi-national sector; namely, transfer pricing and profit imports.

On present trends, the Government will come in about €1 billion under target. But these are early trends which could improve or worsen as the year goes on. Will the deflationary policies of the last two years –now deeply embedded in the economic base – undo the deficit reduction targets? Watch this space but don’t be surprised if the answer is yes.

The Government is hoping to increase the overall Exchequer tax take by €3.1 billion, or 9.9 percent over last year. This is a key determinant to whether the deficit will fall to below -10 percent of GDP (other determinants are public expenditure and the overall level of GDP). This projected increase is made up of increases in the following sub-categories:

• Income tax (including USC): 25.3%

• VAT: 1.3%

• Corporation: 2.4%

• Customs & Excise: 0.1%

• Capital Taxes: 4.5%

The real driver in the projected increase is income tax revenue which includes receipts from the Universal Social Charge. This category is expected to make up over 90 percent of the entire projected tax increase. Of the projected increase of €3.1 billion, income tax/USC is expected to increase by over €2.8 billion.

Why the increase of 25 percent? It’s not because the economy is growing – more employment, more businesses, more tax revenue. The primary reasons are the income tax changes introduced in the budget (cuts in personal tax credits, standard rate tax band, certain tax reliefs, etc.); and the introduction of the USC.

And here is where it starts to get murky. The USC amalgamates the Income Levy and the Health Levy into new thresholds. While the income levy was included in income tax receipts last year, the health levy wasn’t; it was paid directly into the Department of Health and showed up as a Departmental Balance in the Estimates.

What this means is that comparisons between last year’s tax revenue (for both income tax and overall tax) are somewhat skewered since they are not comparing like with like. So when we get headlines like ‘Tax receipts up over 2 percent’ – we have to treat this carefully since last year’s tax receipts didn’t count the health levy which is now part of this year’s USC.

Of course, the Department of Finance could have made this all easier by putting in a like for like comparison. This would have meant taking last year’s figures and adding last year’s monthly receipts of the health levy. This has not been done and I can’t find these monthly figures for last year.

Last year the health levy was estimated to raise €2,431 million. This relates to full year increase. The comparator for this year would be less as January receipts relate to December payments. Therefore, February is the first month that we have to readjust to see how this year’s income tax receipts relate to last year.

• February 2011 income tax receipts: €980

• February 2010 income tax receipts: €784

This might suggest a substantial rise over last year (25 percent) but we have to include the February health levy receipts for 2010 – a figure not readily available. So here is an extrapolation: €186 million. When we add that to the overall February 2010 figure we find the following:

• February 2011 income tax receipts: €980

• February 2010 income tax receipts: €970 (including extrapolated health levy receipts)

The increase for February, therefore, is not 25 percent as the Finance numbers suggest but, rather, 1 percent – and this is with the additional revenue arising from other Budget 2011 changes.

Therefore, the overall tax receipts do not show a 2.2 percent increase over last year. Rather, it shows a -1.7 percent decline.

We should pause here. It is, as they say, early days and we shouldn’t rush to conclusions. But the early returns are not good. The second biggest category – VAT – is showing sluggish receipts so far. They are -2.4 percent down on last year’s outturn and -5.9 percent on the Government’s targets this year.

Throughout the year the important categories to watch are income tax and VAT (it would help if the Department of Finance produced comparable data). Together, they are projected to make up 70 percent of all tax receipts. These best reflect domestic economic activity; corporate tax receipts can reflect the accounting activities of the multi-national sector; namely, transfer pricing and profit imports.

On present trends, the Government will come in about €1 billion under target. But these are early trends which could improve or worsen as the year goes on. Will the deflationary policies of the last two years –now deeply embedded in the economic base – undo the deficit reduction targets? Watch this space but don’t be surprised if the answer is yes.

Friday, 5 November 2010

October tax figures

An Saoi: Seamus Coffey from UCC has produced an excellent analysis of the October Tax Returns on his site Economic Incentives. There you will find a variety of tables providing a seriously good overview of the tax movements, not just of the year to date, but also of the position at this stage for each of the last four years.

The tax figures are ahead of where I expected them to be, the reasons for which I will discuss later. But in discussing the tax figures, the old adage of lies, damn lies and statistics comes immediately to mind. The majority of media stories have correctly pointed out that the Government is for the first time ahead of its forecast. However it is of course substantially below the position of any recent year. We are now back to 2003 tax levels and are unlikely to move much from those levels for some time.

Corporation Tax is the only reason tax figures are ahead of forecast, though even it is €200M down on 2009 figure. The money laundering fees received for facilitating tax avoidance described in a recent article by the journalist Jesse Drucker published by Bloomberg and available here, make up most if not all of this source of tax. My hunch is that Corporation Tax for 2010 will finish with a flourish and will probably end up around €500M over target, with the additional yield coming from just a handful of international fairy godmothers.

The heading Income Tax covers a myriad of different sources of tax including withholding taxes stopped on State service contracts (PSWT), Construction related withholding taxes (RCT), taxes retained on dividends (DWT), taxes retained on deposit interest (DIRT) as well as “normal” income tax paid over through the PAYE system as Income Tax & Income Levy or remitted directly to the Revenue Commissioners by the self employed. The final figure is also net of certain other payments such as mortgage interest and private medical insurance subsidies (TRS) paid directly to lenders and insurers. Income tax has consistently fallen below forecasts and previous year figures as can be seen from the tables available here (thanks again to Seamus Coffey). The reasons for the consistent weakness in Income tax are all around us unemployment, pay cuts and lack of real economic activity. It is a pity that a more detailed analysis is not publicly provided.

Value Added Tax is running slightly over forecast, but nearly €500M below last year. Indeed the figure is back below the 2004 figure. The VAT yield has benefited from Budget changes introduced in an effort to stem the flow North and also the weakening of the Euro against sterling in the interim.

Certain right wing economists have suggested that there is room to increase VAT rates, particularly in light of the UK’s intention to increase their standard rate from 17.5% to 20%. I would caution strongly against such action and indeed would argue that there is a strong case for targeted reductions in VAT to encourage local demand and even to encourage the traffic to move in the opposite direction. The Euro has strengthened by over 7% against sterling since the end of June and may grow stronger over the next few months. There are already stories appearing in the media commenting on the traffic North. It is likely that many NI retailers have already factored in the UK VAT increase and increasing VAT with a strengthening currency would be tantamount to shooting ourselves in both feet.

Excise Duties include vehicle-based taxes (VRT) & taxes on alcohol & tobacco. They show little movement from 2009 or forecasts. The decline in rates of duty charged has kept up the yield, stemming the flow northwards. However the weakness of sterling and the ongoing smuggling problems in relation to cigarettes is likely to keep the pressure on yield. The Government may have no option but to cut duties on alcohol and tobacco to protect the yield. A modest cut in the taxes on cigarettes with more restrictive sales legislation may cut consumption but increase tax yield. Smuggling is estimated to be providing approx. 30% of tobacco products consumed.

The benefit of the reduction in VRT is far more problematic. It is interesting to note that around 33%of the increase in new car sales was made up by a decline in used imports.

The minor taxes sources all remain weak. Capital Acquisitions Tax surely provides opportunities for targeted tax increases, which would be relatively painless. A further reduction in thresholds and also the trimming of the over generous business/agricultural relief available could yield several hundred million euro. It would also go some way to broadening the tax base.

The tax figures are ahead of where I expected them to be, the reasons for which I will discuss later. But in discussing the tax figures, the old adage of lies, damn lies and statistics comes immediately to mind. The majority of media stories have correctly pointed out that the Government is for the first time ahead of its forecast. However it is of course substantially below the position of any recent year. We are now back to 2003 tax levels and are unlikely to move much from those levels for some time.

Corporation Tax is the only reason tax figures are ahead of forecast, though even it is €200M down on 2009 figure. The money laundering fees received for facilitating tax avoidance described in a recent article by the journalist Jesse Drucker published by Bloomberg and available here, make up most if not all of this source of tax. My hunch is that Corporation Tax for 2010 will finish with a flourish and will probably end up around €500M over target, with the additional yield coming from just a handful of international fairy godmothers.

The heading Income Tax covers a myriad of different sources of tax including withholding taxes stopped on State service contracts (PSWT), Construction related withholding taxes (RCT), taxes retained on dividends (DWT), taxes retained on deposit interest (DIRT) as well as “normal” income tax paid over through the PAYE system as Income Tax & Income Levy or remitted directly to the Revenue Commissioners by the self employed. The final figure is also net of certain other payments such as mortgage interest and private medical insurance subsidies (TRS) paid directly to lenders and insurers. Income tax has consistently fallen below forecasts and previous year figures as can be seen from the tables available here (thanks again to Seamus Coffey). The reasons for the consistent weakness in Income tax are all around us unemployment, pay cuts and lack of real economic activity. It is a pity that a more detailed analysis is not publicly provided.

{kind=link}

Value Added Tax is running slightly over forecast, but nearly €500M below last year. Indeed the figure is back below the 2004 figure. The VAT yield has benefited from Budget changes introduced in an effort to stem the flow North and also the weakening of the Euro against sterling in the interim.

Certain right wing economists have suggested that there is room to increase VAT rates, particularly in light of the UK’s intention to increase their standard rate from 17.5% to 20%. I would caution strongly against such action and indeed would argue that there is a strong case for targeted reductions in VAT to encourage local demand and even to encourage the traffic to move in the opposite direction. The Euro has strengthened by over 7% against sterling since the end of June and may grow stronger over the next few months. There are already stories appearing in the media commenting on the traffic North. It is likely that many NI retailers have already factored in the UK VAT increase and increasing VAT with a strengthening currency would be tantamount to shooting ourselves in both feet.

Excise Duties include vehicle-based taxes (VRT) & taxes on alcohol & tobacco. They show little movement from 2009 or forecasts. The decline in rates of duty charged has kept up the yield, stemming the flow northwards. However the weakness of sterling and the ongoing smuggling problems in relation to cigarettes is likely to keep the pressure on yield. The Government may have no option but to cut duties on alcohol and tobacco to protect the yield. A modest cut in the taxes on cigarettes with more restrictive sales legislation may cut consumption but increase tax yield. Smuggling is estimated to be providing approx. 30% of tobacco products consumed.

The benefit of the reduction in VRT is far more problematic. It is interesting to note that around 33%of the increase in new car sales was made up by a decline in used imports.

The minor taxes sources all remain weak. Capital Acquisitions Tax surely provides opportunities for targeted tax increases, which would be relatively painless. A further reduction in thresholds and also the trimming of the over generous business/agricultural relief available could yield several hundred million euro. It would also go some way to broadening the tax base.

Friday, 6 August 2010

July tax figures

An Saoi: That paragon of objective comment, the Sunday Independent, informed us last Sunday that "Public finances (were) buoyed by July Revenue takings", which sort of gave the game away. The Government had something to hide. The by-line informed us that “Income tax receipts 'better than expected'”, and so they were. Income Tax paid in the month to the Revenue Commissioners was €852M against €837M expected, though still far below the July remittances of previous years. To emphasise this possible little green shoot the Dept. of Finance “Information Note” also informs us that “it is important to note that it came in ahead of its monthly target for July.”

July’s unemployment figure goes some way to explain the discrepancy, available here. No longer are the foreigners being let go (Table 9), no longer are the forms P45 going to shop workers and those in the building trade. Table 6 provides a stark analysis of those recently sent on their way. No: this time, 24.3% were professionals and 31.7% in administrative roles. Accrued holiday pay and ex-gratia termination payments paid as they walk through the door for the last time provided a temporary boost in the tax yield, which will be claimed as refunds over the next few months. 75.6% of those let go this month were female, but 82.1% of the professionals sacked were women and 86.4% of clerical/admin staff let go were women. These were core staff to most of the businesses in which they worked. And they have few immediate job prospects

Income Tax is in fact €289M behind a target set less than six months ago, and a massive €483M behind July 2009. Refunds of tax due to the recently unemployed will no doubt increase that discrepancy.

Next, let us look at Excise & VAT together. Excise yield has held up well despite (because) of the reduction in duties on alcohol and the cut on VRT charged on imported new cars. The substantial differential that has opened up between diesel & petrol prices along the border has also boosted fuel sales in this State. However, VAT remains nearly 7% below last year’s figure. The continued decline in retail prices is clearly one factor; however, the continuing decline in demand for goods and services is the real problem. Spending on credit cards is a very good barometer of consumer sentiment and dropped substantially in June 2010 over June 2009, despite glorious weather for the whole month. Approx. two thirds of the annual VAT liability is paid in the first seven months, suggesting that the final outcome is unlikely to break €9,700M, nearly €1,000M short of last year’s outcome.

Our yield from consumption taxes remain very much at the whim of currency movements and UK tax policy. The UK Government are thankfully playing Russian roulette with the Northern economy, with their VAT increase in January next. There is little we can do about currency movements; however, targeted cuts in VAT would give us some protection in ensuring that prices remain attractive on this side of the border.

Corporation Tax looks like the one possible source of Revenue picking up. Most of the big refunds arising from losses in banking and property should have been washed through at this stage, while many of the US multi-nationals who use Ireland to launder their EMEA sales are announcing bumper profits. I have tried to project forward for the last five months of the year using the preliminary tax paid to date & would expect to see the final CT yield in excess of the target, though still well below 2009 and earlier years, say in the region of €3,400M. This should not be seen as a sign of improvement in local economic conditions, but rather as reflecting the activities of a handful of large multi-nationals using Ireland as their sales base.

The other tax sources remain anaemic, though Capital Acquisitions Tax remains robust. Very simple adjustments could dramatically improve the yield. Capital Gains Tax is low with little activity in the sales of assets. The same applies to Stamp Duties. The tax base remains very worryingly narrow as we approach a further slowdown in activity. Yields from the main four sources may yet dry up to a mere trickle.

It is very hard to see how the current Government can hold to their promises of no pay cuts in the Public Service, when they will be cutting services and Social Welfare payments left, right and centre. A 10% cut looks probable with serious consequences for tax yield.

The outlook for the current year remains poor, with 2011 also beginning to look ominous.

July’s unemployment figure goes some way to explain the discrepancy, available here. No longer are the foreigners being let go (Table 9), no longer are the forms P45 going to shop workers and those in the building trade. Table 6 provides a stark analysis of those recently sent on their way. No: this time, 24.3% were professionals and 31.7% in administrative roles. Accrued holiday pay and ex-gratia termination payments paid as they walk through the door for the last time provided a temporary boost in the tax yield, which will be claimed as refunds over the next few months. 75.6% of those let go this month were female, but 82.1% of the professionals sacked were women and 86.4% of clerical/admin staff let go were women. These were core staff to most of the businesses in which they worked. And they have few immediate job prospects

Income Tax is in fact €289M behind a target set less than six months ago, and a massive €483M behind July 2009. Refunds of tax due to the recently unemployed will no doubt increase that discrepancy.

Next, let us look at Excise & VAT together. Excise yield has held up well despite (because) of the reduction in duties on alcohol and the cut on VRT charged on imported new cars. The substantial differential that has opened up between diesel & petrol prices along the border has also boosted fuel sales in this State. However, VAT remains nearly 7% below last year’s figure. The continued decline in retail prices is clearly one factor; however, the continuing decline in demand for goods and services is the real problem. Spending on credit cards is a very good barometer of consumer sentiment and dropped substantially in June 2010 over June 2009, despite glorious weather for the whole month. Approx. two thirds of the annual VAT liability is paid in the first seven months, suggesting that the final outcome is unlikely to break €9,700M, nearly €1,000M short of last year’s outcome.