Slí Eile: The IIEA held an interesting seminar recently on sovereign debt. Here is the link.

Ann Pettifor quoted Henry Liu: ‘“The young, the working poor and the elderly to pay for the careless profligacy and corruption of governments, the propertied rich, and financiers.” She heavily criticised the deflationary tide across Europe

The other two speakers were Lee Buchheit US legal expert on sovereign debt issues (also chair of the Icelandic government’s negotiating committee in the Icesave dispute …) and Dietmar Hornung of Moody’s .

Ann Pettifor’s presentation is available online here. And you can hear her speak by podcast here.

She drew on ‘Fiscal consolidation: A history from a century of UK macroeconomic statistics’. Victoria Chick and Ann Pettifor June 2010

The key conclusion was that

“The economic policies of ‘synchronised austerity’ will not only increase EU unemployment and social dislocation - they will also increase the public debt….

Sooner or later, governments, financial markets and international authorities will be forced to recognise the validity of Keynes’s analysis, ........just as they were forced to do in the 1930s”

Far from being over, as the Moody's speaker claimed, the debate has hardly begun. Events, events, events as the saying goes.

Sunday, 20 June 2010

Appeasing the crazy

Michael Taft: Joseph Stiglitz, writing in the Sunday Tribune, warns against trying to reason with ‘markets’:

‘Appeasing the markets is like trying to reason with a crazy man: after Spain announced its cutbacks, the ratings agencies downgraded its debt because of lower growth prospects as a result of those cuts! You can't win with markets. Better to follow the right policy: supporting growth through higher spending on public investment and infrastructure, which will help the economy grow faster in the long term.’

David McWilliams, in another infuriatingly common-sensical column, writes in similar vein:

‘If the government increases spending to invest in productive assets, like education or infrastructure, it means that, on one side of the balance sheet is debt, but on the other side is an asset, the productive investment which increases the long run growth of the country. This is beneficial spending, because it increases productivity and thus offers a return on investment.’

Have a read and then forward them on to the relevant Minister.

‘Appeasing the markets is like trying to reason with a crazy man: after Spain announced its cutbacks, the ratings agencies downgraded its debt because of lower growth prospects as a result of those cuts! You can't win with markets. Better to follow the right policy: supporting growth through higher spending on public investment and infrastructure, which will help the economy grow faster in the long term.’

David McWilliams, in another infuriatingly common-sensical column, writes in similar vein:

‘If the government increases spending to invest in productive assets, like education or infrastructure, it means that, on one side of the balance sheet is debt, but on the other side is an asset, the productive investment which increases the long run growth of the country. This is beneficial spending, because it increases productivity and thus offers a return on investment.’

Have a read and then forward them on to the relevant Minister.

Thursday, 17 June 2010

FT voices

Paul Sweeney: Following on from Michael Burke's link to Krugman on Tuesday, yesterday Martin Wolf of the Financial Times was quite unequivocal on the dangers of the dash from economic stimulus posed by the “exit strategies” advocated by many economists.

And Lex, the very conservative investor columnist in the Financial Times, described Ireland’s fiscal policy thus: “The process of fiscal adjustment across the eurozone is so arbitrary, so uncoordinated, and – in countries like Ireland and Greece – so savage that the cure is as likely as is the disease to kill the patient.”

And Lex, the very conservative investor columnist in the Financial Times, described Ireland’s fiscal policy thus: “The process of fiscal adjustment across the eurozone is so arbitrary, so uncoordinated, and – in countries like Ireland and Greece – so savage that the cure is as likely as is the disease to kill the patient.”

Tuesday, 15 June 2010

Krugman & lying eyes

Michael Burke: Paul Krugman, writing in the New York Times, asks whether fiscal austerity measures actually reassure the financial markets. This question is of course extremely pertinent to this economy. Not only has the FF-led government led the way in slash&burn economics in Europe, but this has become a defining totem of its economic policy - that the cuts are necessary to reassure financial markets.

Government policy was recently commended by the Wall Street Journal, and duly got a widespread airing. Krugman's analysis is very different and by implication much more critical of policy. I'm guessing his piece will get much less of an airing on the radio shows and might not be reproduced by the Irish Times. Just a hunch.

But who is right, the WSJ, or the NYT's Nobel-winning economist? The only way to judge is in their treatment of facts. Specifically, both articles refer to the reaction in the bond market to Dublin's economic policy, and the contrast with that of Madrid. Krugman points out that Irish 10yr bond yields are higher than Spanish ones, despite the fact that the latter had to be recently strong-armed into fiscal austerity and there has been a public backlash against the measures. He also points that Irish Credit Default Swap rates are higher than Spanish ones. Although these are less reliable guides than bond yields, because they are smaller, more illiquid markets, they do indicate that more speculators are betting on an Irish default than on a Spanish one. Helpfully, Krugman provides links to Bloomberg charts, so the facts at least cannot be contested. In neither case can it be argued that the fiscal austerity here has provided greater reassurance to the markets.

But what of the Murdoch-owned WSJ? It certainly uses lots of facts to support its argument that policy here is correct, and should be emulated. But how it uses those facts is less than rigorous.

To take the key area of disputed ground, bond yields, this is what the WSJ says in its opening paragraph, "SPANISH TWO-year government bond yields climbed five basis points to 2.47 per cent on Monday morning, after Fitch last week cut Spain’s triple-A credit rating to double-A-plus. Ireland, on the other hand, has been making do with its diminished Fitch rating of double A-minus since November. And yet yesterday morning the yield on its two-year government bond was at 1.77 per cent, down seven basis points from the day before, though its 10-year yields remain elevated." The full piece can be read here.

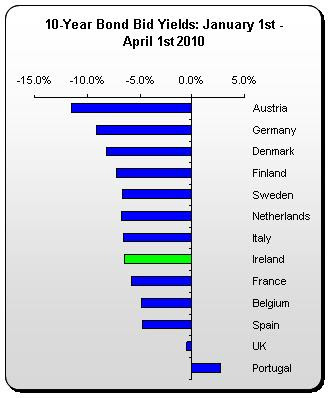

It is perfectly true that Spanish 2-year government yields are higher than Irish ones. But the WSJ article glossed over the fact that Spanish 10-year yields are significantly lower as they have been throughout the crisis. This is shown in the chart below.

Yields

10-year yields are the accepted benchmark for government debt, as prudent government borrowers attempt to lengthen the maturity of its debt precisely to avoid being hurt by wild short-term swings in market sentiment. Less than 20% of government debt is held at short-term maturities like 2 years, the bulk held at much longer maturities. So, while the WSJ treated us to a daily commentary on Irish 2yr yield movements, it passed over a key fact; that Irish long-term yields are higher than Spain's where it counts, which is where most of the borrowing is done. The grudging admission was that Irish 10yr yields 'remain elevated'.

All the crisis-hit countries in Western Europe, Greece, Spain, Portugal and Italy are suffering a fate that has already befallen Eastern Europe. International bodies such as the ECB, European Commission, IMF, etc. insist on austerity policies to reassure financial markets. Sometimes local governments are happy to oblige, others need arm-twisting. But the austerity doesn't reassure financial markets, so more of the same is demanded, and yields rise because bond investors think that the risk of default is rising, as Krugman points out.

Within that general trend, there seem to be favoured countries and not so favoured ones. These are the ones under attack and whose 2year yields are pushed higher as governments find it hard to access short-term funds. But it seems to have little to do with deficits- Italy's deficit is expected to be 5.3% of GDP this year the same as Belgium's, compared to 8% for France and 11.7% for Ireland. And it seems to have precious little to do with debt levels either, with Spain's debt at 64.9% of GDP this year, compared to 77.3% for Ireland, 78.8% for Germany, 83.6% for France, and 99% for Belgium. It does have a lot to do with the scale and foreign assets of each country's banking system, but that's another story http://socialisteconomicbulletin.blogspot.com/2010/06/parasite-threatens-host-impact-of.html .

Irish 10yr yields were the highest in the EU for most of 2009, as austerity was being implemented, in contrast to the rest of the Euro Area, where various types of stimulus measures were attempted. The reassurance that bond investors need is that you can meet interest payments and repay debt as it falls due. For governments that can only come from tax revenues.

Krugman ends with a question, should you believe what everyone knows, or your own lying eyes?

Government policy was recently commended by the Wall Street Journal, and duly got a widespread airing. Krugman's analysis is very different and by implication much more critical of policy. I'm guessing his piece will get much less of an airing on the radio shows and might not be reproduced by the Irish Times. Just a hunch.

But who is right, the WSJ, or the NYT's Nobel-winning economist? The only way to judge is in their treatment of facts. Specifically, both articles refer to the reaction in the bond market to Dublin's economic policy, and the contrast with that of Madrid. Krugman points out that Irish 10yr bond yields are higher than Spanish ones, despite the fact that the latter had to be recently strong-armed into fiscal austerity and there has been a public backlash against the measures. He also points that Irish Credit Default Swap rates are higher than Spanish ones. Although these are less reliable guides than bond yields, because they are smaller, more illiquid markets, they do indicate that more speculators are betting on an Irish default than on a Spanish one. Helpfully, Krugman provides links to Bloomberg charts, so the facts at least cannot be contested. In neither case can it be argued that the fiscal austerity here has provided greater reassurance to the markets.

But what of the Murdoch-owned WSJ? It certainly uses lots of facts to support its argument that policy here is correct, and should be emulated. But how it uses those facts is less than rigorous.

To take the key area of disputed ground, bond yields, this is what the WSJ says in its opening paragraph, "SPANISH TWO-year government bond yields climbed five basis points to 2.47 per cent on Monday morning, after Fitch last week cut Spain’s triple-A credit rating to double-A-plus. Ireland, on the other hand, has been making do with its diminished Fitch rating of double A-minus since November. And yet yesterday morning the yield on its two-year government bond was at 1.77 per cent, down seven basis points from the day before, though its 10-year yields remain elevated." The full piece can be read here.

It is perfectly true that Spanish 2-year government yields are higher than Irish ones. But the WSJ article glossed over the fact that Spanish 10-year yields are significantly lower as they have been throughout the crisis. This is shown in the chart below.

Yields

10-year yields are the accepted benchmark for government debt, as prudent government borrowers attempt to lengthen the maturity of its debt precisely to avoid being hurt by wild short-term swings in market sentiment. Less than 20% of government debt is held at short-term maturities like 2 years, the bulk held at much longer maturities. So, while the WSJ treated us to a daily commentary on Irish 2yr yield movements, it passed over a key fact; that Irish long-term yields are higher than Spain's where it counts, which is where most of the borrowing is done. The grudging admission was that Irish 10yr yields 'remain elevated'.

All the crisis-hit countries in Western Europe, Greece, Spain, Portugal and Italy are suffering a fate that has already befallen Eastern Europe. International bodies such as the ECB, European Commission, IMF, etc. insist on austerity policies to reassure financial markets. Sometimes local governments are happy to oblige, others need arm-twisting. But the austerity doesn't reassure financial markets, so more of the same is demanded, and yields rise because bond investors think that the risk of default is rising, as Krugman points out.

Within that general trend, there seem to be favoured countries and not so favoured ones. These are the ones under attack and whose 2year yields are pushed higher as governments find it hard to access short-term funds. But it seems to have little to do with deficits- Italy's deficit is expected to be 5.3% of GDP this year the same as Belgium's, compared to 8% for France and 11.7% for Ireland. And it seems to have precious little to do with debt levels either, with Spain's debt at 64.9% of GDP this year, compared to 77.3% for Ireland, 78.8% for Germany, 83.6% for France, and 99% for Belgium. It does have a lot to do with the scale and foreign assets of each country's banking system, but that's another story http://socialisteconomicbulletin.blogspot.com/2010/06/parasite-threatens-host-impact-of.html .

Irish 10yr yields were the highest in the EU for most of 2009, as austerity was being implemented, in contrast to the rest of the Euro Area, where various types of stimulus measures were attempted. The reassurance that bond investors need is that you can meet interest payments and repay debt as it falls due. For governments that can only come from tax revenues.

Krugman ends with a question, should you believe what everyone knows, or your own lying eyes?

Sunday, 13 June 2010

Revised rent supports

An Saoi: The Dept. of Social Protection (formerly Dept. of SFA) has finally announced the revised rent supports, effective from now until Secember 2011. It is unfortunate that An tAire Ó Cúiv did not publish the Report on which the revised figures are based. The Report was prepared from, “Information from the Private Residential Property Board databases; the CSO Rental Indices, in addition to the various rental market reports was utilised. Consultation with certain local Superintendent Community Welfare Officers also took place as part of the review.” It certainly would make interesting reading.

It has been suggested in the past (and the Minister made reference to it in interviews) that rent support had become a floor in the private rental market. Our friends in Daft do a comprehensive quarterly report of advertised rent levels, see for example their Quarter 1 2010 Report . Agreed rents may be slightly lower, but this does not devalue the importance of these reports.

I decided to do a comparison between the requested rents and the level of rent supports. In Table 1 the rents quoted are for a two bed unit and the level of rent support is the maximum available for a one child family (one or two parent). The Discrepancy is the percentage difference between requested rent levels and the revised support levels.

Table 1

As can be seen the variation is quite considerable. It would also suggest that outside of urban Cork, Galway & Sligo, all of which have unusually high student populations, the level of rental support may be excessive and indeed acting to prevent rents falling.

In Table 2 the rents quoted are for a three bed unit and the level of rent support is the maximum available for a family with two children (one or two parent). Again, the Discrepancy is the percentage difference between requested rent levels and the revised support levels.

Table 2

The pattern is somewhat similar with the discrepancies in the student dominated markets of Sligo Galway & Cork standing out. In general the discrepancies are less than those in Table 1.

The rents listed above are of course from the first quarter of 2010 and it will be the third quarter before the announced reductions have fed into the system. The reductions in rent supports are to be welcomed but leaving the current levels in place until 2012 seems excessive. A further review of rent support levels in six months could yield substantial further savings to the State.

It has been suggested in the past (and the Minister made reference to it in interviews) that rent support had become a floor in the private rental market. Our friends in Daft do a comprehensive quarterly report of advertised rent levels, see for example their Quarter 1 2010 Report . Agreed rents may be slightly lower, but this does not devalue the importance of these reports.

I decided to do a comparison between the requested rents and the level of rent supports. In Table 1 the rents quoted are for a two bed unit and the level of rent support is the maximum available for a one child family (one or two parent). The Discrepancy is the percentage difference between requested rent levels and the revised support levels.

Table 1

As can be seen the variation is quite considerable. It would also suggest that outside of urban Cork, Galway & Sligo, all of which have unusually high student populations, the level of rental support may be excessive and indeed acting to prevent rents falling.

In Table 2 the rents quoted are for a three bed unit and the level of rent support is the maximum available for a family with two children (one or two parent). Again, the Discrepancy is the percentage difference between requested rent levels and the revised support levels.

Table 2

The pattern is somewhat similar with the discrepancies in the student dominated markets of Sligo Galway & Cork standing out. In general the discrepancies are less than those in Table 1.

The rents listed above are of course from the first quarter of 2010 and it will be the third quarter before the announced reductions have fed into the system. The reductions in rent supports are to be welcomed but leaving the current levels in place until 2012 seems excessive. A further review of rent support levels in six months could yield substantial further savings to the State.

Thursday, 10 June 2010

FEPS / TASC Seminar on 'Stimulating Recovery'

Speakers at a seminar organised by TASC and the Foundation for European Progressive Studies (FEPS) today emphasised the need for an investment strategy to grow the economy, create jobs and counter the current deflationary spiral. The emphasis was on ‘investment towards fiscal consolidation’, and the speakers presented a set of complementary arguments demonstrating that the Government’s fiscal policies have failed, are failing and will continue to fail.

The papers (by Professor Ray Kinsella of UCD, TASC Head of Policy Sinéad Pentony and Michael Burke) can be downloaded from the TASC website (www.tascnet.ie)

The papers (by Professor Ray Kinsella of UCD, TASC Head of Policy Sinéad Pentony and Michael Burke) can be downloaded from the TASC website (www.tascnet.ie)

Wednesday, 9 June 2010

The Reports ...

The Watson/Regling report is available here, and the Honohan report is available here. Comments?

Tuesday, 8 June 2010

Earth goes around the sun - shock

Michael Burke: One of the reasons why economists are often held in low esteem by the general public is that they claim the mantle of science while frequently producing arguments that are unscientific in the extreme.

To take one example, a giant of the natural sciences; Galileo. One of the reasons that Galileo was certain the Earth moves around the Sun was because he approximately calculated some of the distances within the Solar system, and reasoned that such huge bodies could not be hurtling at such great speeds through the Universe. Instead, we now know that the speeds Galileo calculated are actually a tiny fraction of their real speeds, given that the galaxies too and the Universe as whole are also in (extremely fast) motion. But no modern scientist spends any time deriding Galileo for his incorrect assumption, but marvels at his insight, ingenuity and worldliness.

Contrast this with Jeffrey Sachs in today's FT, who has come to bury Keynes, not praise him. Readers are left in no doubt that one of the architects of 'shock therapy' in Eastern Europe is not a fan. Never has been.

But look more closely at what he does argue for. This includes:

- Counter-cyclical spending

- Greening the economy

- Government investment

- Tax rises- big ones for the rich

- Promoting post-secondary education

- Income support for the poor

- Universal access to healthcare and education

- Promotion of exports, clean energy and transport infrastructure

And he argues specifically against:

- Car scrappage schemes

- Tax cuts

- Misplaced cuts in public spending

In fact, the Keynes that Sachs wants to consign to history could have written that policy menu himself (but would no doubt have included lots of measures designed to lower long-term interest rates too). Maybe Sachs' ire is really directed at large budget deficits. But the phrase 'budget deficit' never appears in Keynes' General Theory and they were never advocated by him, so perhaps Prof. Sachs' anger is misdirected. For some reason, Western governments' running large deficits in the 60s and 70s was Keynes' fault. Yet no-one accused Ronald Reagan of Keynesianism when he did it in the 80s.

No matter, no harm done. Two cheers for Jeffrey Sachs, who has discovered for himself that the Earth goes round the Sun.

Now, who's going to break it to Mr Lenihan?

To take one example, a giant of the natural sciences; Galileo. One of the reasons that Galileo was certain the Earth moves around the Sun was because he approximately calculated some of the distances within the Solar system, and reasoned that such huge bodies could not be hurtling at such great speeds through the Universe. Instead, we now know that the speeds Galileo calculated are actually a tiny fraction of their real speeds, given that the galaxies too and the Universe as whole are also in (extremely fast) motion. But no modern scientist spends any time deriding Galileo for his incorrect assumption, but marvels at his insight, ingenuity and worldliness.

Contrast this with Jeffrey Sachs in today's FT, who has come to bury Keynes, not praise him. Readers are left in no doubt that one of the architects of 'shock therapy' in Eastern Europe is not a fan. Never has been.

But look more closely at what he does argue for. This includes:

- Counter-cyclical spending

- Greening the economy

- Government investment

- Tax rises- big ones for the rich

- Promoting post-secondary education

- Income support for the poor

- Universal access to healthcare and education

- Promotion of exports, clean energy and transport infrastructure

And he argues specifically against:

- Car scrappage schemes

- Tax cuts

- Misplaced cuts in public spending

In fact, the Keynes that Sachs wants to consign to history could have written that policy menu himself (but would no doubt have included lots of measures designed to lower long-term interest rates too). Maybe Sachs' ire is really directed at large budget deficits. But the phrase 'budget deficit' never appears in Keynes' General Theory and they were never advocated by him, so perhaps Prof. Sachs' anger is misdirected. For some reason, Western governments' running large deficits in the 60s and 70s was Keynes' fault. Yet no-one accused Ronald Reagan of Keynesianism when he did it in the 80s.

No matter, no harm done. Two cheers for Jeffrey Sachs, who has discovered for himself that the Earth goes round the Sun.

Now, who's going to break it to Mr Lenihan?

Monday, 7 June 2010

Irish debt ... finally, some healthy scepticism

Michael Taft: Just because some people don’t get it – that shouldn’t stop us from getting it. Colm ‘Digger’ McCarthy was at it again, calling upon the nation to dig an even deeper hole. We have engaged in deflationary policies in order to please the markets. This obviously isn’t working. What’s the solution? More deflationary policies.

‘ . . . the government needs to re-state as forcefully as possible its commitment to fiscal consolidation, and to ignore the irresponsible cacophony of demands for additional spending. We will be lucky if we can borrow enough to keep the show on the road.’

Along the way, certain facts have to be ignored and unsubstantiated assertions repeated. For instance, the deflationary interventions last year produced benefit to Irish borrowing costs. It didn’t – as shown here. Borrowing costs increased after each ‘budget’ the Government introduced (February pension levy/spending cuts, April emergency budget, 2010 budget).

Then we got the ‘We’re not Spain, Italy or Portugal’. No, we were worse, despite some commentators’ determination not to read the indices. Of course, they had to say this because admitting things were going south would beg questions about the efficacy of deflationary policies.

Now we’re getting a ‘We were doing the right thing, the markets knew we are doing the right thing but the Euro crisis was outside our control and we unfortunately got swept into the maelstrom.’

Under this narrative, Irish debt was improving up to April – proof that the markets were satisfied. The problem for this narrative is that all EU-15 countries debt was improving (save for Greece and Portugal); but Ireland was improving less than most other nations. And some of those countries whose debt didn’t improve as much in percentage terms as Ireland’s (e.g. Belgium and France) – well, their borrowing costs were much, much lower than ours to start with.

Still, the spin continues. Only this morning we have this gem from the Irish Independent:

‘ASIDE from bond yields that aren't as high as others in the eurozone, the rewards for Ireland's early frugality have been slow to come.’

What index could they possible be referring to? Excluding Greece (who’s not in the market), Irish 10-Year spreads are the worst in the EU-15. According to the Irish Times Saturday index Irish 10-spread came in at 2.53. Next in line is Portugal at 2.51. Every other country is well below.

False narrative, missed facts, bad prescriptions; at least some commentators are starting to express reservations. Peter Bacon said:

‘It is unclear if Europe can sustain fiscal consolidation in the medium term without a growth strategy running in parallel.’

Alan McQuaid said:

‘The 5% interest rate is going too high. My view is that the markets are not buying into the austerity strategy. Telling everybody to get to 3% in two or three years risks knocking the stuffing out of the economy.’

In addition, the Sunday Tribune reports:

‘Ben May, a European economist at Capital Economics in London, warned it would be tough for Ireland to meet the 3% target by 2014 because economic growth rates would unlikely rise back up to historical levels.’

And in the Sunday Business Post, David McWilliams posed the issue this way in arguing for an immediate close down of Anglo Irish:

‘The reason the markets will support closing down Anglo is that markets have no interest in an Ireland that turns itself into a debt-servicing machine to pay for the mistakes of yesterday . . The financial markets are investors who want growth, who want to invest in the real wealth of Ireland and the real wealth of this country . . No investor minds a government spending €20 billion on education and infrastructure because it means the balance sheet will have an asset opposite the debt. But on our national balance sheet opposite the €20 billion is Anglo, with its treasure chest of worthless land and sites. This simple accounting identity scares people.’

At least, in a few quarters, scepticism over deflationary policies is being raised.

We may not be reaching a consensus on a new macro-economic framework – one which emphasises investment, growth, employment, and tax-driven fiscal consolidation. But more and more are starting to ask the difficult questions.

That’s a start.

‘ . . . the government needs to re-state as forcefully as possible its commitment to fiscal consolidation, and to ignore the irresponsible cacophony of demands for additional spending. We will be lucky if we can borrow enough to keep the show on the road.’

Along the way, certain facts have to be ignored and unsubstantiated assertions repeated. For instance, the deflationary interventions last year produced benefit to Irish borrowing costs. It didn’t – as shown here. Borrowing costs increased after each ‘budget’ the Government introduced (February pension levy/spending cuts, April emergency budget, 2010 budget).

Then we got the ‘We’re not Spain, Italy or Portugal’. No, we were worse, despite some commentators’ determination not to read the indices. Of course, they had to say this because admitting things were going south would beg questions about the efficacy of deflationary policies.

Now we’re getting a ‘We were doing the right thing, the markets knew we are doing the right thing but the Euro crisis was outside our control and we unfortunately got swept into the maelstrom.’

Under this narrative, Irish debt was improving up to April – proof that the markets were satisfied. The problem for this narrative is that all EU-15 countries debt was improving (save for Greece and Portugal); but Ireland was improving less than most other nations. And some of those countries whose debt didn’t improve as much in percentage terms as Ireland’s (e.g. Belgium and France) – well, their borrowing costs were much, much lower than ours to start with.

Still, the spin continues. Only this morning we have this gem from the Irish Independent:

‘ASIDE from bond yields that aren't as high as others in the eurozone, the rewards for Ireland's early frugality have been slow to come.’

What index could they possible be referring to? Excluding Greece (who’s not in the market), Irish 10-Year spreads are the worst in the EU-15. According to the Irish Times Saturday index Irish 10-spread came in at 2.53. Next in line is Portugal at 2.51. Every other country is well below.

False narrative, missed facts, bad prescriptions; at least some commentators are starting to express reservations. Peter Bacon said:

‘It is unclear if Europe can sustain fiscal consolidation in the medium term without a growth strategy running in parallel.’

Alan McQuaid said:

‘The 5% interest rate is going too high. My view is that the markets are not buying into the austerity strategy. Telling everybody to get to 3% in two or three years risks knocking the stuffing out of the economy.’

In addition, the Sunday Tribune reports:

‘Ben May, a European economist at Capital Economics in London, warned it would be tough for Ireland to meet the 3% target by 2014 because economic growth rates would unlikely rise back up to historical levels.’

And in the Sunday Business Post, David McWilliams posed the issue this way in arguing for an immediate close down of Anglo Irish:

‘The reason the markets will support closing down Anglo is that markets have no interest in an Ireland that turns itself into a debt-servicing machine to pay for the mistakes of yesterday . . The financial markets are investors who want growth, who want to invest in the real wealth of Ireland and the real wealth of this country . . No investor minds a government spending €20 billion on education and infrastructure because it means the balance sheet will have an asset opposite the debt. But on our national balance sheet opposite the €20 billion is Anglo, with its treasure chest of worthless land and sites. This simple accounting identity scares people.’

At least, in a few quarters, scepticism over deflationary policies is being raised.

We may not be reaching a consensus on a new macro-economic framework – one which emphasises investment, growth, employment, and tax-driven fiscal consolidation. But more and more are starting to ask the difficult questions.

That’s a start.

Sunday, 6 June 2010

Protecting those who have no voice

Slí Eile: The Poor Can't Pay have just issued an important statement about the need for people to make a personal commitment that there will no more cuts in social welfare payments. The statement can be read here. Quite simply, the poor can't pay any more because for many struggling on a meagre income, with little prospect of a job and seeing stealth cuts by a 100 means another cut will be devastating. It may be said that the 'Croke Park' deal, if it passes, will protect the wages and living standards of public sector workers. This is not necessarily the case especially if:

- price inflation resumes in 2010-11 and erodes the real value of wages in the public service

- further taxes on income and property are levied on workers (including those on low income or possibly in 'negative equity'

- there is a serious deterioration in the budgetary situation (the opt-out clause).

While certainty around nominal income going forward may be viewed as better than no loaf and escalation of industrial conflict into full-scale class war, the wider picture needs to be considered including the very real possibility that Government will seek to blame, implicitly or otherwise, the public sector pay lock-in for targetting even more cuts at social welfare recipients and areas of 'non-pay' expenditure (various significant programmes capital and non-capital). All in the interests of appeasing the 'markets' you know. We are living in interesting times whatever the outcome of the Croke Park deal. However, one thing must be assured - let those who care stand together and put the most vulnerable at the top of priorities. It is only fair. And it is good economics because if every shilling taken from the poor leads to further drops in spending and further job losses.

- price inflation resumes in 2010-11 and erodes the real value of wages in the public service

- further taxes on income and property are levied on workers (including those on low income or possibly in 'negative equity'

- there is a serious deterioration in the budgetary situation (the opt-out clause).

While certainty around nominal income going forward may be viewed as better than no loaf and escalation of industrial conflict into full-scale class war, the wider picture needs to be considered including the very real possibility that Government will seek to blame, implicitly or otherwise, the public sector pay lock-in for targetting even more cuts at social welfare recipients and areas of 'non-pay' expenditure (various significant programmes capital and non-capital). All in the interests of appeasing the 'markets' you know. We are living in interesting times whatever the outcome of the Croke Park deal. However, one thing must be assured - let those who care stand together and put the most vulnerable at the top of priorities. It is only fair. And it is good economics because if every shilling taken from the poor leads to further drops in spending and further job losses.

Friday, 4 June 2010

May figures

An Saoi: May’s Tax figures suggest little sign of a pick up, despite the Dept of Finance’s brave effort to suggest that all is still on target. If there was any real improvement happening, then the tax figures should be beginning to show it. They are not. We remain over 10% below last year’s levels. The drop is not uniform, with perhaps small signs that those who have kept their jobs are wandering back into town on paydays.

Income Tax figures are 8.9% behind last year, and a full €219M below their estimates made just four months ago. This is perhaps the most worrying of all the figures. The publication of the most recent unemployment figures on the same day emphasised the point made so many times here – Tax flows from economic activity, not from cutting the economy further.

The Corporation Tax figures continue to show our addict-like dependence on multi-nationals, in particular big pharma & US computer software companies. Most of this month’s money may have come from just a handful of companies. Because companies pay their preliminary tax on fixed dates based on their accounting year end, payers in May would have either a 30th June year end or 30th November. Next month will see the first payments from companies with a 31st December year end, which makes up the majority of Irish companies

Jack Fagan in Thursday’s Irish Times Property supplement suggested that Executor led sales had picked up, however the Stamp Duty figures suggest that there is no bottoming out at all yet. Payments are 17.3% below last year and more alarmingly 14.3% below expectations. Capital Acquisitions Tax is ahead of both last year and profile, which perhaps confirmation of Mr. Fagan’s comments.

Capital Gains Tax is also down 41.4% on 2009, but is up on profile, but is miniscule compared to previous years.

The VAT figures were reasonable, reflecting a slowing in the rate of decline in retail purchases. The Central Bank’s analysis of credit card spending confirms this trend. A drop in the number of people shopping in the North may also have assisted. The suicidal dependency of all of the Irish banks on interbank borrowing to fund their loan books will ensure that providing new loans to Irish business or public will remain a dream.

There is a massive latent VAT bonanza for the State if even a small number of the empty new builds are sold, as effectively one sixth of the price will go to the State in VAT. However, sales are very unlikely for many years.

The forthcoming funding crisis facing not just the Irish banks, but all those banks across Europe who became dependent on the crack cocaine of banking, inter bank loans, will adversely influence the rest of the year. Even the dealer of last resort, the ECB, will not be able to deal with the demand.

There is a major caveat on all these figures – The Revenue provides no summary of outstanding refunds. Corporation Tax & VAT refunds can be huge, particularly VAT refunds for service exporters and the overhang can be substantial and material to the overall totals. There has been constant innuendo that the Revenue have slowed up the issuance of refunds, which maybe partially caused by the lost of experienced staff.

Without a substantial pick up in the economy happening very quickly, I cannot see the Minister getting close to his projection and remain wedded to my previous estimates.

Income Tax figures are 8.9% behind last year, and a full €219M below their estimates made just four months ago. This is perhaps the most worrying of all the figures. The publication of the most recent unemployment figures on the same day emphasised the point made so many times here – Tax flows from economic activity, not from cutting the economy further.

The Corporation Tax figures continue to show our addict-like dependence on multi-nationals, in particular big pharma & US computer software companies. Most of this month’s money may have come from just a handful of companies. Because companies pay their preliminary tax on fixed dates based on their accounting year end, payers in May would have either a 30th June year end or 30th November. Next month will see the first payments from companies with a 31st December year end, which makes up the majority of Irish companies

Jack Fagan in Thursday’s Irish Times Property supplement suggested that Executor led sales had picked up, however the Stamp Duty figures suggest that there is no bottoming out at all yet. Payments are 17.3% below last year and more alarmingly 14.3% below expectations. Capital Acquisitions Tax is ahead of both last year and profile, which perhaps confirmation of Mr. Fagan’s comments.

Capital Gains Tax is also down 41.4% on 2009, but is up on profile, but is miniscule compared to previous years.

The VAT figures were reasonable, reflecting a slowing in the rate of decline in retail purchases. The Central Bank’s analysis of credit card spending confirms this trend. A drop in the number of people shopping in the North may also have assisted. The suicidal dependency of all of the Irish banks on interbank borrowing to fund their loan books will ensure that providing new loans to Irish business or public will remain a dream.

There is a massive latent VAT bonanza for the State if even a small number of the empty new builds are sold, as effectively one sixth of the price will go to the State in VAT. However, sales are very unlikely for many years.

The forthcoming funding crisis facing not just the Irish banks, but all those banks across Europe who became dependent on the crack cocaine of banking, inter bank loans, will adversely influence the rest of the year. Even the dealer of last resort, the ECB, will not be able to deal with the demand.

There is a major caveat on all these figures – The Revenue provides no summary of outstanding refunds. Corporation Tax & VAT refunds can be huge, particularly VAT refunds for service exporters and the overhang can be substantial and material to the overall totals. There has been constant innuendo that the Revenue have slowed up the issuance of refunds, which maybe partially caused by the lost of experienced staff.

Without a substantial pick up in the economy happening very quickly, I cannot see the Minister getting close to his projection and remain wedded to my previous estimates.

Wednesday, 2 June 2010

The inter-relationship of it all

Michael Taft: From Ernst & Young’s Economic Eye Summer 2010 forecast, two projections scream out from the report:

First, employment levels won’t return to their pre-recession level until 2022. Yes, 2022. That’s 15 years of a jobs-recession – a decade and a half. That led the report to refer to a ‘ . . . sluggish and largely ‘jobless’ recovery’. The word ‘largely’ is an understatement.

Second, is their projection on the annual deficit. This is equally depressing but, given their employment projections, not surprising. Ernst & Young project that the Government will not only fail to reach the Maastricht deficit target of -3 percent by 2014 – they won’t reach it until 2018 or 2019.

What’s noteworthy about this deficit projection is that it is done against the background of a reasonably optimistic growth rate of 3.5 percent throughout the next decade. However, the E&Y report poses a number of caveats, especially as this growth rate rests largely on the export sector. They raise the real danger of a two-tier economy, with the domestic economy lagging even further behind. If this occurs, we might find that the deficit might (might) eventually come right statistically, but remain an unsustainably high burden for years and years to come.

Of course, this will no doubt give new impetus to the cuts brigade – those who believe you get out of a hole by digging even more. They should be aware of the following. Just after the April 2009 budget, E&Y projected that Ireland would reach the Maastricht deficit target by 2015. Now, after the December budget, they have pushed that back by three to four years. Another round of cuts could see that target pushed back even further.

The key inter-relationship is employment and the deficit. A jobless recovery will continue to impair the public finances. Responding to public finances by more spending cuts will exacerbate employment. And this, in turn, will continue to impair public finances.

Some Governments get it. This one doesn’t.

First, employment levels won’t return to their pre-recession level until 2022. Yes, 2022. That’s 15 years of a jobs-recession – a decade and a half. That led the report to refer to a ‘ . . . sluggish and largely ‘jobless’ recovery’. The word ‘largely’ is an understatement.

Second, is their projection on the annual deficit. This is equally depressing but, given their employment projections, not surprising. Ernst & Young project that the Government will not only fail to reach the Maastricht deficit target of -3 percent by 2014 – they won’t reach it until 2018 or 2019.

What’s noteworthy about this deficit projection is that it is done against the background of a reasonably optimistic growth rate of 3.5 percent throughout the next decade. However, the E&Y report poses a number of caveats, especially as this growth rate rests largely on the export sector. They raise the real danger of a two-tier economy, with the domestic economy lagging even further behind. If this occurs, we might find that the deficit might (might) eventually come right statistically, but remain an unsustainably high burden for years and years to come.

Of course, this will no doubt give new impetus to the cuts brigade – those who believe you get out of a hole by digging even more. They should be aware of the following. Just after the April 2009 budget, E&Y projected that Ireland would reach the Maastricht deficit target by 2015. Now, after the December budget, they have pushed that back by three to four years. Another round of cuts could see that target pushed back even further.

The key inter-relationship is employment and the deficit. A jobless recovery will continue to impair the public finances. Responding to public finances by more spending cuts will exacerbate employment. And this, in turn, will continue to impair public finances.

Some Governments get it. This one doesn’t.

Tuesday, 1 June 2010

Property taxes and economic growth

Tom McDonnell: Nat O’Connor’ post on this blog on May 18th provided an excellent overview of the debate on property tax. Another important aspect of the debate relates to the effect of a property tax on economic growth.

It is important to stress at this point that I’m restricting my comments here to ‘bricks and mortar’ property. Bricks and mortar property is no more or no less a form of property than a financial asset or a car, but as it is likely that any property tax introduced later this year will effectively be a bricks and mortar tax, I won’t include those other categories of property in this post. Of course, from an equity perspective an all-encompassing property tax is preferable to just a bricks and mortar tax, because most low and middle income earners do not have substantial assets besides the family home.

The parlous state of the public finances seems to be making the prospect of some form of bricks and mortar property tax ever more likely. But fixing the hole in the public finances is not the only reason to introduce such a property tax. From an economic growth perspective, recurrent (e.g., once a year) taxes on immovable property are generally considered to be desirable because they do not penalise productive activity. One rationale is that, in the long term, recurrent taxes on immovable property will shift some investment out of housing into higher return investments and so increase the rate of growth. Taxes on property transactions are considered less desirable than recurrent taxes for a number of reasons, for example because they reduce labour mobility. Recurrent property taxes are also preferable to taxes on property transactions because they are stable over the economic cycle

Recent evidence indicates that the tax structure does appear to impact growth performance. The OECD looked at various taxes from an economic efficiency perspective and found that property taxes may be the least damaging to growth prospects. Heady et al (2009)also find that recurrent taxes on immovable property are the least harmful (or most beneficial) tax instrument in terms of its effect on long-run GDP per capita.

The full tax-and-growth rankings are (from best to worst):

1. recurrent taxes on immovable property

2. consumption taxes (and other property taxes)

3. personal income taxes

4. corporate income taxes

Finally, it should be noted that the better-off are disproportionately likely to hold property, and that it should therefore be possible to construct a progressive property tax. An inequality-proofed and poverty-proofed property tax is long overdue in Ireland.

It is important to stress at this point that I’m restricting my comments here to ‘bricks and mortar’ property. Bricks and mortar property is no more or no less a form of property than a financial asset or a car, but as it is likely that any property tax introduced later this year will effectively be a bricks and mortar tax, I won’t include those other categories of property in this post. Of course, from an equity perspective an all-encompassing property tax is preferable to just a bricks and mortar tax, because most low and middle income earners do not have substantial assets besides the family home.

The parlous state of the public finances seems to be making the prospect of some form of bricks and mortar property tax ever more likely. But fixing the hole in the public finances is not the only reason to introduce such a property tax. From an economic growth perspective, recurrent (e.g., once a year) taxes on immovable property are generally considered to be desirable because they do not penalise productive activity. One rationale is that, in the long term, recurrent taxes on immovable property will shift some investment out of housing into higher return investments and so increase the rate of growth. Taxes on property transactions are considered less desirable than recurrent taxes for a number of reasons, for example because they reduce labour mobility. Recurrent property taxes are also preferable to taxes on property transactions because they are stable over the economic cycle

Recent evidence indicates that the tax structure does appear to impact growth performance. The OECD looked at various taxes from an economic efficiency perspective and found that property taxes may be the least damaging to growth prospects. Heady et al (2009)also find that recurrent taxes on immovable property are the least harmful (or most beneficial) tax instrument in terms of its effect on long-run GDP per capita.

The full tax-and-growth rankings are (from best to worst):

1. recurrent taxes on immovable property

2. consumption taxes (and other property taxes)

3. personal income taxes

4. corporate income taxes

Finally, it should be noted that the better-off are disproportionately likely to hold property, and that it should therefore be possible to construct a progressive property tax. An inequality-proofed and poverty-proofed property tax is long overdue in Ireland.

Monday, 31 May 2010

Mortgage arrears and the case for assistance

Tom O'Connor: The comments last week by the Financial Regulator Matthew Elderfield display a callous indifference to the plight of 77,000 people currently in arrears with their mortgages. Mr Elderfield rejects government help for these people, as it would cost the taxpayer money. This is astonishing when we consider that he is supportive of the €33 billion in recapitalisation of the banks and the overall cost (including NAMA) of €73 billion according to the ESRI. This includes €10.44 billion to Anglo Irish Bank, which has very few ordinary people as customers and is well known as the bank of the property developers.

We are not being told of the extent of arrears. However, there are 77,000 householders in arrears. Even if every single one of these housholders had arrears totalling €20,000, this would still only add up to 1.54 billion. This is just 2% of the €73 billion being given to the banks. Now, even though it is the taxpayer who will be liable for the €73 billion, they are being denied what amounts to 2% of this figure to keep 77,000 people in homes.

The government’s 12 month moratorium on repossessions has ended for many, and will end for all in September. The truth of the matter is that if we are to take Mr.Elderfield's advice, then the government should stand idly by and watch the unfolding of a social catastrophe.

Mr Elderfield's justification is that other mortgage payers have 'gritted their teeth and are meeting their obligations'. So he is essentially blaming the 77,000 for their plight. This is an outlandish comment because: the vast majority of defaulters are victims of poor government policy arising from its cosy relationship with the construction industry which forced them to buy houses at hugely inflated prices; the government gave people no other option, building only 4,000 social and affordable housing units of the 80,000 a year demanded by the population over the period Celtic Tiger; and the mismanagement of the economy and the bursting of the housing bubble has seen unemployment hit 435,000 while the government does nothing to solve the problem. In fact, its taskforce met once last year before being disbanded.

Surely €1.54 billion could be set aside to pay these arrears. This could be given as re-mortages to defaulters by the Irish government. The defaulters could be asked to make minimum payments, covering interst on mortages at most, if possible, until they are in better financial circumstances. A further €460 million fund could cover the difference between the minimum payment and the actual monthly mortgage payment over the next 12 months until people get back on their feet. The situation could be reviewed at that stage. This is only one obvious way to tackle this problem. There are others.

The government would be foolish to listen to Mr.Elderfield. He is a financial regulator, not a policy maker, and has no democratically elected mandate. It is really time for people to demand a payback from the state, given the risk that they as taxpayers are being asked to take to solve the financial mess which they did not create themselves. The minium is to allow people stay in their homes. People need to stand up and not allow themselves be trampled on any further.

We are not being told of the extent of arrears. However, there are 77,000 householders in arrears. Even if every single one of these housholders had arrears totalling €20,000, this would still only add up to 1.54 billion. This is just 2% of the €73 billion being given to the banks. Now, even though it is the taxpayer who will be liable for the €73 billion, they are being denied what amounts to 2% of this figure to keep 77,000 people in homes.

The government’s 12 month moratorium on repossessions has ended for many, and will end for all in September. The truth of the matter is that if we are to take Mr.Elderfield's advice, then the government should stand idly by and watch the unfolding of a social catastrophe.

Mr Elderfield's justification is that other mortgage payers have 'gritted their teeth and are meeting their obligations'. So he is essentially blaming the 77,000 for their plight. This is an outlandish comment because: the vast majority of defaulters are victims of poor government policy arising from its cosy relationship with the construction industry which forced them to buy houses at hugely inflated prices; the government gave people no other option, building only 4,000 social and affordable housing units of the 80,000 a year demanded by the population over the period Celtic Tiger; and the mismanagement of the economy and the bursting of the housing bubble has seen unemployment hit 435,000 while the government does nothing to solve the problem. In fact, its taskforce met once last year before being disbanded.

Surely €1.54 billion could be set aside to pay these arrears. This could be given as re-mortages to defaulters by the Irish government. The defaulters could be asked to make minimum payments, covering interst on mortages at most, if possible, until they are in better financial circumstances. A further €460 million fund could cover the difference between the minimum payment and the actual monthly mortgage payment over the next 12 months until people get back on their feet. The situation could be reviewed at that stage. This is only one obvious way to tackle this problem. There are others.

The government would be foolish to listen to Mr.Elderfield. He is a financial regulator, not a policy maker, and has no democratically elected mandate. It is really time for people to demand a payback from the state, given the risk that they as taxpayers are being asked to take to solve the financial mess which they did not create themselves. The minium is to allow people stay in their homes. People need to stand up and not allow themselves be trampled on any further.

Sunday, 30 May 2010

Get thee to a calculator

Michael Taft: ‘One and one is what I’m telling you / get a pocket computer’

So sang Blondie. Deborah Harry might have been singing to whoever penned the latest Back Room article in the Sunday Business Post. Arguing that economic policy under a Fine Gael / Labour government would not be significantly different, the author goes on to write:

‘According to the Government’s own figures, the exchequer deficit will this year amount to €18.8 billion. Had the Government not already taken harsh budgetary steps, equivalent in total to €15.9 billion, our exchequer deficit would be a staggering €34.7 billion this year, or 27 percent of national income.’

Just when you think you’ve read it all, along comes someone to present us with a statement so devoid of understanding that all you can do is be amazed that this stuff actually gets published. If the government had not taken harsh steps would our deficit have risen to nearly €35 billion? Of course not; but don’t take my word for it – here’s what the Department of Finance had to say about the matter.

In their 2010 Pre-Budget Outlook, Finance projected the annual deficit for 2010 to 2013 in the absence of any fiscal correction from Budget 2010 onwards; in other words, if there were no tax increases and no spending cuts. This is what they came up with, as a percentage of GDP:

2010: - 14 percent (‘around’ as Finance puts it)

2011: - 13.7 percent

2012: - 12.2 percent

2013 - 10.5 percent

Finance was attempting to assess the deficit without €11 billion worth spending cuts and / or tax increases. You might have noticed that the deficit goes down. Indeed, if one extrapolates from the figures to estimate 2014 (Finance didn’t do 2014 because the EU Commission had yet to postpone the Maastricht target date), the deficit would be less than - 9 percent.

Amazing. Doing nothing would actually cut the deficit by nearly 40 percent. Yet our Back Room whiz has our deficit ballooning to 27 percent of GNP. To readjust the above figures, the deficit would fall from – 17.4 percent of GNP in 2010 to – 11.3 percent in 2014.

If anything, Finance under-estimates the decline in the deficit because they took a ‘static’ approach, which means they didn’t assess the impact of withdrawing the cuts and tax increases on the GDP. I discussed some of this here at the time of the publication.

So how did Back Room get a €35 billion figure? She/he merely totted up the amount of fiscal correction to date and added it to the current deficit. Of course, this ignores the deflationary and, at times, self-defeating impact of such correction.

First, tax increases reduce tax revenue in other streams (e.g. if you increase income levies, people have less money to spend and, consequently indirect taxes fall). In addition, tax increases reduce demand which leads to higher spending (unemployment costs) and reduced tax revenue through less business profits and tax on labour which has been cut.

Second, spending cuts act in the same way but as the ESRI has shown, they are even more damaging to the economy – spending cuts reduce tax revenue and increase unemployment costs more than tax increases.

Third, given that the GDP is reduced, the resulting deficit still remains high.

This is not an argument for doing nothing. Indeed, if one were forensic in tax increases (only on high income earners) and spending cuts (in areas that benefit high income earners), there would be less deflationary impact. And if that were combined with stimulus measures to generate employment and growth it would mean a faster falling deficit and overall debt. Faster than what the Government is trying to attempt.

But that these arguments are difficult to get across is evident when one has to read the type of stuff that Back Room churned out. For that is where our debate is at – an absolute inability to read the economy. And if you can’t read the economy, how are you going to fix it?

So sang Blondie. Deborah Harry might have been singing to whoever penned the latest Back Room article in the Sunday Business Post. Arguing that economic policy under a Fine Gael / Labour government would not be significantly different, the author goes on to write:

‘According to the Government’s own figures, the exchequer deficit will this year amount to €18.8 billion. Had the Government not already taken harsh budgetary steps, equivalent in total to €15.9 billion, our exchequer deficit would be a staggering €34.7 billion this year, or 27 percent of national income.’

Just when you think you’ve read it all, along comes someone to present us with a statement so devoid of understanding that all you can do is be amazed that this stuff actually gets published. If the government had not taken harsh steps would our deficit have risen to nearly €35 billion? Of course not; but don’t take my word for it – here’s what the Department of Finance had to say about the matter.

In their 2010 Pre-Budget Outlook, Finance projected the annual deficit for 2010 to 2013 in the absence of any fiscal correction from Budget 2010 onwards; in other words, if there were no tax increases and no spending cuts. This is what they came up with, as a percentage of GDP:

2010: - 14 percent (‘around’ as Finance puts it)

2011: - 13.7 percent

2012: - 12.2 percent

2013 - 10.5 percent

Finance was attempting to assess the deficit without €11 billion worth spending cuts and / or tax increases. You might have noticed that the deficit goes down. Indeed, if one extrapolates from the figures to estimate 2014 (Finance didn’t do 2014 because the EU Commission had yet to postpone the Maastricht target date), the deficit would be less than - 9 percent.

Amazing. Doing nothing would actually cut the deficit by nearly 40 percent. Yet our Back Room whiz has our deficit ballooning to 27 percent of GNP. To readjust the above figures, the deficit would fall from – 17.4 percent of GNP in 2010 to – 11.3 percent in 2014.

If anything, Finance under-estimates the decline in the deficit because they took a ‘static’ approach, which means they didn’t assess the impact of withdrawing the cuts and tax increases on the GDP. I discussed some of this here at the time of the publication.

So how did Back Room get a €35 billion figure? She/he merely totted up the amount of fiscal correction to date and added it to the current deficit. Of course, this ignores the deflationary and, at times, self-defeating impact of such correction.

First, tax increases reduce tax revenue in other streams (e.g. if you increase income levies, people have less money to spend and, consequently indirect taxes fall). In addition, tax increases reduce demand which leads to higher spending (unemployment costs) and reduced tax revenue through less business profits and tax on labour which has been cut.

Second, spending cuts act in the same way but as the ESRI has shown, they are even more damaging to the economy – spending cuts reduce tax revenue and increase unemployment costs more than tax increases.

Third, given that the GDP is reduced, the resulting deficit still remains high.

This is not an argument for doing nothing. Indeed, if one were forensic in tax increases (only on high income earners) and spending cuts (in areas that benefit high income earners), there would be less deflationary impact. And if that were combined with stimulus measures to generate employment and growth it would mean a faster falling deficit and overall debt. Faster than what the Government is trying to attempt.

But that these arguments are difficult to get across is evident when one has to read the type of stuff that Back Room churned out. For that is where our debate is at – an absolute inability to read the economy. And if you can’t read the economy, how are you going to fix it?

Thursday, 27 May 2010

The Honohan and Regling reports

Jim Stewart: There is considerable media coverage and speculation about the contents of the forthcoming Honohan Report on the role of the Central Bank, and the report by the Financial Regulator on the financial and economic crisis (See Simon Carswell, Irish Times 26/5/2010, Emmet Oliver, Irish Independent 25/5/2010, Ian Kehoe, Sunday Business Post 23/5/2010) David Clerkin and Cliff Taylor Sunday Business Post 23/5/2010).

In addition some of the key people involved in financial decision making have also expressed considerable interest in the findings - for example, Michael Somers (interview in the Sunday Independent (23/5/2010). Of the two reports, the Honohan Report is likely to be the more interesting, for example in understanding policy mistakes made by the Central Bank and the Financial Regulator.

It is also of interest that Michael Somers, in giving evidence to the Central Bank Governor (rather than the inquiry team), stated that he was not in any way involved in the decisions to give guarantees to the six covered institutions on 29th September 2008. Michael Somers is quoted as stating :- Patrick Honohan asked me to meet with his team of inquirers and I said I would meet with him, which I duly did. I think his main interest really was what was happening at the time of the guarantee. I said: 'I can't help you because I wasn't here'." (He does not appear to have had a Blackberry!) This statement appears to contradict the view of Eamon Gilmore (Dail Debate April 1) that the terms of reference of the inquiry excluded the government’s decision in respect of the guarantee.

Whether the guarantee is included or excluded from the scope of the inquiry is of great interest, because it is seen by some (for example, Morgan Kelly Irish Times 22/5/2010) as being disastrous for the stability of exchequer finances and any possible recovery. The guarantee helped the survival of all the covered institutions, but the issue is whether two of those institutions should not have been supported with a consequent reduction in the cost to the State. The ending of the guarantee gives an opportunity to revisit this decision. The guarantee also had a cost in terms of increasing the overall borrowing rate estimated at 0.15 -0.3% (Department of Finance Banking Statement Supplementary Documentation), recouped from the covered institutions via charges.

The decision to implement the guarantee may lie in an important Ecofin (Economic and Financial Affairs Council) decision one year earlier, that responsibility for managing any crisis effectively rested with national authorities (Ecofin meeting October 9, 2007). In late September 2008, following the Lehman collapse, a loss in confidence in banks raised the real possibility of bank runs. In response, individual countries competed for deposits via more and more generous insurance schemes. As Fonteyne et al state (available here) “Starting in early October 2008, EU member countries effectively raced one another to extend deposit and other bank guarantees”. Ireland was one of the first countries “out of the trap” to start this race, and this led to considerable criticism at the time (See for example, Charlie Weston, Irish Independent, October 1, 2008).

Fonteyne at al also note that bank failures “have been very rare in the EU and have usually been limited to small banks”. Restructuring via injections of public funds has been common, and exit via arranged mergers. This was attempted in the case of Anglo Irish and Irish Nationwide. The rarity of decisions to allow banks to fail within the EU is also likely to have influenced decision-making in implementing the guarantee.

The ending of the bank guarantee provides* an opportunity to ‘close’ both Anglo Irish and Irish Nationwide by withdrawing State support, which is very likely to cause them to move into liquidation. Alternative options between liquidation and continuing State support are also possible and deserve extensive analysis. In any event the liquidation of both institutions now, would not (unfortunately) remove all liabilities for the Irish State, central bank deposits would have to be repaid, ordinary depositors and perhaps commercial bank depositors (should there be any) are likely to be repaid in full.

Given the international nature of Anglo Irish’s assets and liabilities, allowing this bank to fail in view of the absence of an EU-wide special resolution regime is likely to be resisted by EU bodies such as the ECB.

The forthcoming reports are important. Given the public interest nature of the issues involved, including as much detail as possible would add enormously to their value.

* The guarantee has been extended for certain debt instruments and the main scheme may be extended until December according to Cliff Taylor, Sunday Business post 23/5/2010).

In addition some of the key people involved in financial decision making have also expressed considerable interest in the findings - for example, Michael Somers (interview in the Sunday Independent (23/5/2010). Of the two reports, the Honohan Report is likely to be the more interesting, for example in understanding policy mistakes made by the Central Bank and the Financial Regulator.

It is also of interest that Michael Somers, in giving evidence to the Central Bank Governor (rather than the inquiry team), stated that he was not in any way involved in the decisions to give guarantees to the six covered institutions on 29th September 2008. Michael Somers is quoted as stating :- Patrick Honohan asked me to meet with his team of inquirers and I said I would meet with him, which I duly did. I think his main interest really was what was happening at the time of the guarantee. I said: 'I can't help you because I wasn't here'." (He does not appear to have had a Blackberry!) This statement appears to contradict the view of Eamon Gilmore (Dail Debate April 1) that the terms of reference of the inquiry excluded the government’s decision in respect of the guarantee.

Whether the guarantee is included or excluded from the scope of the inquiry is of great interest, because it is seen by some (for example, Morgan Kelly Irish Times 22/5/2010) as being disastrous for the stability of exchequer finances and any possible recovery. The guarantee helped the survival of all the covered institutions, but the issue is whether two of those institutions should not have been supported with a consequent reduction in the cost to the State. The ending of the guarantee gives an opportunity to revisit this decision. The guarantee also had a cost in terms of increasing the overall borrowing rate estimated at 0.15 -0.3% (Department of Finance Banking Statement Supplementary Documentation), recouped from the covered institutions via charges.

The decision to implement the guarantee may lie in an important Ecofin (Economic and Financial Affairs Council) decision one year earlier, that responsibility for managing any crisis effectively rested with national authorities (Ecofin meeting October 9, 2007). In late September 2008, following the Lehman collapse, a loss in confidence in banks raised the real possibility of bank runs. In response, individual countries competed for deposits via more and more generous insurance schemes. As Fonteyne et al state (available here) “Starting in early October 2008, EU member countries effectively raced one another to extend deposit and other bank guarantees”. Ireland was one of the first countries “out of the trap” to start this race, and this led to considerable criticism at the time (See for example, Charlie Weston, Irish Independent, October 1, 2008).

Fonteyne at al also note that bank failures “have been very rare in the EU and have usually been limited to small banks”. Restructuring via injections of public funds has been common, and exit via arranged mergers. This was attempted in the case of Anglo Irish and Irish Nationwide. The rarity of decisions to allow banks to fail within the EU is also likely to have influenced decision-making in implementing the guarantee.

The ending of the bank guarantee provides* an opportunity to ‘close’ both Anglo Irish and Irish Nationwide by withdrawing State support, which is very likely to cause them to move into liquidation. Alternative options between liquidation and continuing State support are also possible and deserve extensive analysis. In any event the liquidation of both institutions now, would not (unfortunately) remove all liabilities for the Irish State, central bank deposits would have to be repaid, ordinary depositors and perhaps commercial bank depositors (should there be any) are likely to be repaid in full.

Given the international nature of Anglo Irish’s assets and liabilities, allowing this bank to fail in view of the absence of an EU-wide special resolution regime is likely to be resisted by EU bodies such as the ECB.

The forthcoming reports are important. Given the public interest nature of the issues involved, including as much detail as possible would add enormously to their value.

* The guarantee has been extended for certain debt instruments and the main scheme may be extended until December according to Cliff Taylor, Sunday Business post 23/5/2010).

Wednesday, 26 May 2010

Dare we take note?

Michael Taft: Lawrence Summers, Director of President Obama’s National Economic Council, is articulating sound economic common sense(thanks to Michael Burke for the heads up on this):

‘It is not possible to imagine sound budgets in the absence of economic growth and solid economic performance.’

And

‘Appropriate short-run expansionary budget policy can make an important contribution to establishing the confidence necessary for sound growth.’

And

‘(It is) impossible to sensibly address either unemployment or long-run fiscal challenges in isolation.’

Anyone in the Irish Government want to take note?

‘It is not possible to imagine sound budgets in the absence of economic growth and solid economic performance.’

And

‘Appropriate short-run expansionary budget policy can make an important contribution to establishing the confidence necessary for sound growth.’

And

‘(It is) impossible to sensibly address either unemployment or long-run fiscal challenges in isolation.’

Anyone in the Irish Government want to take note?

Monday, 24 May 2010

Did free fees reduce inequality?

Kevin Denny at the Geary Institute has just posted a very important working paper that highlights the failure of the abolition of university fees to accomplish its primary goal of reducing educational inequality.

Kevin’s broad conclusion is that the abolition effectively amounts to a windfall gain for middle class parents who no longer have to pay fees. The result is that the policy is unintentionally highly regressive.

He also points out that, before the abolition of fees, low-income students received a means tested grant covering both tuition costs and a contribution to their living expenses. The effect of abolition was to actually withdraw the one advantage low income students had relative to high income students.

The author concludes by making some key points. First, he highlights the importance of early interventions in life; and second, he points out that for policies to be successful they must actually target the intended beneficiaries.

Kevin’s broad conclusion is that the abolition effectively amounts to a windfall gain for middle class parents who no longer have to pay fees. The result is that the policy is unintentionally highly regressive.

He also points out that, before the abolition of fees, low-income students received a means tested grant covering both tuition costs and a contribution to their living expenses. The effect of abolition was to actually withdraw the one advantage low income students had relative to high income students.

The author concludes by making some key points. First, he highlights the importance of early interventions in life; and second, he points out that for policies to be successful they must actually target the intended beneficiaries.

Sunday, 23 May 2010

Unaffordable commentary

Michael Taft: We will never find the answers to our severe economic problems until we ground our debate in facts. Take the issue of wages and labour costs: Dr. Garret Fitzgerald makes a specific assertion as to what contributed to our economic ills:

‘. . . before the housing bubble and bank collapse, we had allowed unsustainable prosperity to mislead us into paying ourselves unaffordable wages, salaries, and bonuses – sums that ran far beyond the capacity of any European country.’

Unaffordable wages? Beyond the capacity of any European country? How valid is this assertion? Not very. Not very at all. Let’s look at three sectors, courtesy of the EU Klems database which measures labour costs, productivity and capital compensation. All figures relate to the latest year we have data for – 2007.

Manufacturing

Irish labour costs in manufacturing are low in comparison with our EU trading partners – extremely low. We rank 12th with labour costs running at €20.76 compared to an EU-15 average of €25.03. Labour costs in our peer group (excluding the four poorer Mediterranean countries) averaged €28.90. On this basis it can hardly be argued that our costs are in anyway ‘unaffordable’.

There is the argument that wages have grown too fast? This, again, is a misconception. Irish labour costs rose by €5.20 per hour between 2000 and 2007. The average rise in the other EU-15 countries was €5.20. Our labour costs rose at the average level. The average rise among our peer group was even higher – €5.85. So in this category our labour cost rise was lower than average.