Gerry Hughes: In the National Pensions Framework document the Government points out that between 2004 and 2009 it increased the State Pension (Contributory) by almost two and a half times more than the increase in average industrial earnings and by nearly four times more than the increase in the Consumer Price Index. The increase in the real value of the State Pension resulted in a sharp fall in the risk of poverty for older people from 27 per cent to just over 11 per cent and in consistent poverty from 3.9 per cent to 1.4 per cent.

The strong effect on poverty rates of Government support for the public pension system contrasts with the weak effect on coverage rates of Government support for the private pension system by the introduction in 2003 of tax advantages for Personal Retirement Savings Accounts. Overall coverage of private pensions showed only a marginal increase from 52 per cent in Q1 2002 to 54 per cent in Q1 2008, according to the framework document. The National Pensions Policy Initiative target of 70 per cent coverage for those in employment aged 30 to 65, which was set in 1998, has not been attained. Coverage for this group increased from 59 per cent in Q1 2002 to only 61 per cent in Q1 2008.

The success of the policy of preventing poverty for older people by increasing the benefits of the public pension system is recognised in the framework document by a statement that “the Government will seek to sustain the value of the State Pension at 35 per cent of average weekly earnings and will support this through the PRSI contribution system. “ The Government also recognises that the PRSI system minimises administration costs, is relatively simple to understand and ensures security. However, instead of proposing to develop the public system to build on these strengths the Government simply asserts that the solution to Ireland’s pension problems is to introduce a new auto-enrolment, privately managed, supplementary pension scheme for all employees not covered by an appropriate occupational scheme. The contributions, amounting to 8 per cent for each employee (employee 4 per cent, employer 2 per cent, State 2 per cent), would be collected through the PRSI system and handed over in a competitive process to private pension providers.

No reason is given for why the pensions industry, and the Irish pensions industry in particular, should be rewarded in this way. In the financial crisis of 2008 Irish pension funds had the worst performance of national pension funds in 37 OECD and non-OECD countries. The Irish pension funds lost 37 per cent of the nominal value of their assets, or €27 billion, compared with an average loss of 20 per cent in the OECD area. Employees availing of the auto-enrolment scheme could be exposed to similar losses in the future because “the Government will not,…, provide any guarantees on investment returns.”

The framework document also proposes phased increases in the retirement age. Implementing these increases would reduce the expected lifetime value of the State Pension by 5.5 per cent for current workers aged 62 to 65, by 11 per cent for those aged 50 to 55 and by 16.5 per cent for those aged 49 or younger. At a time when people are reeling from shocks to the financial system, when many employers with DB schemes are reneging on their promise to provide a secure income in retirement and there has been a collapse in the value of pension assets in DC schemes, these are significant losses for the State to impose on employees who have fulfilled their part of the implicit intergenerational Pay As You Go contract on public pensions.

The intention of the proposed auto-enrolment scheme is to assist those in the lower to middle income range to make their own arrangements to bridge the gap and bring their post-retirement income up to the Government’s target of 50 per cent of pre-retirement income. The auto-enrolment scheme is unlikely to enable middle income employees to do this because the proposed contribution rate of 8 per cent is too low. An analysis in the Green Paper on Pensions shows that the average contributor to a PRSA is paying 10.5 per cent of salary and that this is not nearly enough to provide a replacement rate of 50 per cent of pay from a combination of a voluntary private and a mandatory flat-rate State pension.

The TCD Pension Policy Research Group has argued in Choosing Your Future, and Tasc has argued in Making Pensions Work for People, that there is an option available to the Government which would build on the success of the social insurance model in preventing pensioner poverty and provide replacement rates of 50 per cent of pre-retirement income for workers on middle incomes. This is the mandatory State earnings-related option analysed in the National Pensions Review published in 2005. It would provide a flat-rate pension of 34 per cent of average industrial earnings and a supplementary earnings-related payment that would provide an overall benefit close to the 50 per cent target for middle income workers. The total additional contribution required for this option would be 5 per cent to be paid by equal contributions by the employee and the employer of 2.5 per cent of earnings.

Regrettably, the framework document ignores most of the evidence in favour of the superiority of the social insurance system in delivering pensions and opts instead to reward the most incompetent private pensions industry in the OECD.

Tuesday, 6 April 2010

Saturday, 3 April 2010

Crucifixion Friday

An Saoi: The Irish title for Good Friday is Aoine an Chéasta or 'Crucifixion Friday'. I gather that the traditional method of crucifixion involved a slow painful death and of course the English word “excruciating” literally “out of crucifixion” describes it perfectly.

As a country we are in an excruciating condition, having been financially crucified by this unholy alliance of Fianna Fáil, the builder/developers and the banks. There is certain appropriateness to the issuance of the first quarter tax figures today.

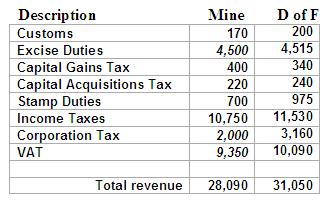

I go through the taxes in more detail below, but I have a firstly set out my revised projections. The Dept. of Finance still seem happy to stand over the figures they issued just eight weeks ago, which are already 3.5 per cent behind profile.

I commented last month that the Corporation Tax figures seemed to be a matter of concern not just to me, but also to the Dept. of Finance. There has been a complete collapse this month, which has forced me to slash my estimate by 33 per cent to just €2,000M. However I will come back to this figure again after seeing the May figures. There are signs that many multi-nationals have decided that they can move from a low tax regime here to a no tax regime also here, using the increasing number of incentives on offer to them.

I have also adjusted upwards the Excise and VAT figures. The adjustments are based on the take up of the car scrappage scheme. What a pity that instead of a scheme sucking in imports, we did not decide to encourage activities with almost 100 per cent local input, such as slashing VAT on restaurants and hotels.

Capital Gains Tax is well ahead of profile but far below the position of last or earlier years. But all of the other taxes show little signs of life in the zombie that is the Irish economy. The additional CGT payments may be the result of a small number of investors crystallising gains previously sheltered in investment holding companies.

The Government are assuming that there will be a pick up later in the year, which will lead to higher taxes, but as retail lending rates increase and households get their personal balance sheets in order, it is very hard to see this happening. Employment numbers continue to fall and it is hard to see where the extra demand will come from.

This month I decided to see what some other commentators have said about the tax forecast. To hell with the realists/pessimists and read what an optimist has to say!

A little while ago, I was sent a copy of Bloxham’s Irish Quarterly Economic Outlook. Alan McQuaid has always been a little bit of an optimist but he surpassed himself here. His tax forecast is extraordinary, see Table below, and is €675M higher than the Dept. of Finance’s total and over €3,500M away from my figures.

He is suggesting that the decline in GDP will be just 0.8 per cent in 2010 and of 3 per cent in GNP. He also is suggesting a much lower borrowing requirement than anyone else.

April is a very quiet tax month and there will be just two figures worth watching, Income Tax to see how the monthly PAYE returns are doing and also the Excise figures for the influence of the car scrappage scheme. May is however a key month with large VAT & Corporation Tax payments due. Any further slippage in the figures will be clear by then and require immediate action. Last month I suggested “Mini-budget and further pay cuts in June? Because there will certainly be no pick up!” Spending is below profile, however it is unclear how much of this was weather-related or for other reasons. Also many planned cutbacks have not yet happened, for example in the Health Service. Many voluntary hospitals and other institutions have only recently received their budgets and are still in discussions with the HSE. I am personally aware of one institution where approx. 10 per cent of frontline staff will be gone by year-end, unless the subvention is increased.

As a country we are in an excruciating condition, having been financially crucified by this unholy alliance of Fianna Fáil, the builder/developers and the banks. There is certain appropriateness to the issuance of the first quarter tax figures today.

I go through the taxes in more detail below, but I have a firstly set out my revised projections. The Dept. of Finance still seem happy to stand over the figures they issued just eight weeks ago, which are already 3.5 per cent behind profile.

I commented last month that the Corporation Tax figures seemed to be a matter of concern not just to me, but also to the Dept. of Finance. There has been a complete collapse this month, which has forced me to slash my estimate by 33 per cent to just €2,000M. However I will come back to this figure again after seeing the May figures. There are signs that many multi-nationals have decided that they can move from a low tax regime here to a no tax regime also here, using the increasing number of incentives on offer to them.

I have also adjusted upwards the Excise and VAT figures. The adjustments are based on the take up of the car scrappage scheme. What a pity that instead of a scheme sucking in imports, we did not decide to encourage activities with almost 100 per cent local input, such as slashing VAT on restaurants and hotels.

Capital Gains Tax is well ahead of profile but far below the position of last or earlier years. But all of the other taxes show little signs of life in the zombie that is the Irish economy. The additional CGT payments may be the result of a small number of investors crystallising gains previously sheltered in investment holding companies.

The Government are assuming that there will be a pick up later in the year, which will lead to higher taxes, but as retail lending rates increase and households get their personal balance sheets in order, it is very hard to see this happening. Employment numbers continue to fall and it is hard to see where the extra demand will come from.

This month I decided to see what some other commentators have said about the tax forecast. To hell with the realists/pessimists and read what an optimist has to say!

A little while ago, I was sent a copy of Bloxham’s Irish Quarterly Economic Outlook. Alan McQuaid has always been a little bit of an optimist but he surpassed himself here. His tax forecast is extraordinary, see Table below, and is €675M higher than the Dept. of Finance’s total and over €3,500M away from my figures.

He is suggesting that the decline in GDP will be just 0.8 per cent in 2010 and of 3 per cent in GNP. He also is suggesting a much lower borrowing requirement than anyone else.

April is a very quiet tax month and there will be just two figures worth watching, Income Tax to see how the monthly PAYE returns are doing and also the Excise figures for the influence of the car scrappage scheme. May is however a key month with large VAT & Corporation Tax payments due. Any further slippage in the figures will be clear by then and require immediate action. Last month I suggested “Mini-budget and further pay cuts in June? Because there will certainly be no pick up!” Spending is below profile, however it is unclear how much of this was weather-related or for other reasons. Also many planned cutbacks have not yet happened, for example in the Health Service. Many voluntary hospitals and other institutions have only recently received their budgets and are still in discussions with the HSE. I am personally aware of one institution where approx. 10 per cent of frontline staff will be gone by year-end, unless the subvention is increased.

Friday, 2 April 2010

Bank shareholders bailed out, welfare recipients to pay

Michael Burke: There is clearly a degree of dissembling that is taking place regarding the bank nationalisation, smokesceens about leaving the Euro, or how bank debt will impair our credit rating (the government has already done that), and perhaps the biggest of all, that the cost of 'oblterating' Anglo-Irish would be huge and would be incurred by the State.

It is therefore important to establish some of the key points of the bail-out:

* the State will add €33bn in debt in order to bail-out bank shareholders and bondholders. This is true whether the debt is issued in the form of promissory notes, IOUs, or sovereign bonds

* the State has removed €10.6bn from the economy in spending cuts and tax increases

gven that nominal GDP was €163.5bn over the course of 2009 and nominal GNP was €131.4, the bank bailout was 20% of GDP and the fiscal contraction was 6.4% of GDP (not including December’s effort)

* for those who insist on using the GNP denominator, the proportions were 25% bank bailout and 8% fiscal contraction (it would be wholly inconsistent to use two different denominators for government finances and the bank bail-out, since both debts must be met from the same income stream, mainly taxes)

* likewise, it is important to use nominal measures, since, unfortuantely the debts cannot be serviced in CSO-2007 euros, but must be met from the actual incomes received, by corporates, households and the government in 2009 euros and beyond. This inconvenient truth is regularly ignored by advocates of competitive deflation; real debts increase as prices and incomes fall

* the €33bn is a fraud in the strictest sense; ie payment of an extremely large sum of money for something that is worthless. Without the government guarantee all the shares in the banks receiving capital would be revalued at zero, likewise the majority of the bonds. The government has increased taxpayers' stake in nothing

* the €33bn is, and I know many scourges of the public sector are fond of these type of comparisons, equivalent to the 3 largest voted departmental spending areas combined, health & children, social & family and education & science, with room to cover arts, sports & tourism as well as the communication, energy and natural resources budgets for 2009 too,

* if issued as four-year debt (assuming a speedy resolution of the banking crisis) the annual cost would be €925mn, for 4 years, or more realistically, if issued at 10yrs, the annual interest bill based on prevailing interest rates would be €1.475bn, slightly more than the Employment, Trade & Enterprise budget

It is hard to imagine which Irish entitities could absorb all the additional State borrowing, implying that foreign ownership of Irish government (or quasi-goernment) debt will increase. While there was a €29.3bn trade surplus in 2009, net factor income from abroad was -€31.9bn. Increased foreign indebtedness will tend to increase the net capital outflow via debt interest payments, pushing a (virtually non-taxed) export-led recovery even further back on the horizon.

Clearly, the project represents a huge transfer of weatlh from the poor to the rich. In the modern era, this usually takes place in some under-developed economy by a Western power and is little reported. It is rarely done so blatantly within a Western economy; so one for the record books.

So what should progressives argue for as an alternative? The key to the situation, and the reason Mr Lenihan's assertion about 'obliteration' is a falsehood, is the bank guarantee. Without it there would be no possible contagion from the banks to government debt. And wthout it there would be no bank shareholders, either.

Their holding would be valued at their true worth, that is zero. It is probably also true that zero would be the share price without the latest lifeline from taxpayers, since any residual value in the shares was premised on the expectation for further slugs of taxpayer money as required.

Therefore, the shareholders would be wiped out and most of the bondholders too by either a withdrawal of the guarantee, or even charging a realistic price for it, or the repatration of the capital injections. Since the taxpayer is now the largest shareholder, emergency legislaion should be prepared to do both those things and at the same time, protect the deposits of the banks' customers by seizing them.

The new entitities would be owned by the State, as now yet rigorously managed, but could then form the basis of a banking sector which did not jeopardise depositors, engaged in prudent balance sheet management, not casino capitalism, and was directed to invest in the most productive areas of the economy, delivering large returns for the shareholder; the taxpayer, and large economic benefits for all.

It is therefore important to establish some of the key points of the bail-out:

* the State will add €33bn in debt in order to bail-out bank shareholders and bondholders. This is true whether the debt is issued in the form of promissory notes, IOUs, or sovereign bonds

* the State has removed €10.6bn from the economy in spending cuts and tax increases

gven that nominal GDP was €163.5bn over the course of 2009 and nominal GNP was €131.4, the bank bailout was 20% of GDP and the fiscal contraction was 6.4% of GDP (not including December’s effort)

* for those who insist on using the GNP denominator, the proportions were 25% bank bailout and 8% fiscal contraction (it would be wholly inconsistent to use two different denominators for government finances and the bank bail-out, since both debts must be met from the same income stream, mainly taxes)

* likewise, it is important to use nominal measures, since, unfortuantely the debts cannot be serviced in CSO-2007 euros, but must be met from the actual incomes received, by corporates, households and the government in 2009 euros and beyond. This inconvenient truth is regularly ignored by advocates of competitive deflation; real debts increase as prices and incomes fall

* the €33bn is a fraud in the strictest sense; ie payment of an extremely large sum of money for something that is worthless. Without the government guarantee all the shares in the banks receiving capital would be revalued at zero, likewise the majority of the bonds. The government has increased taxpayers' stake in nothing

* the €33bn is, and I know many scourges of the public sector are fond of these type of comparisons, equivalent to the 3 largest voted departmental spending areas combined, health & children, social & family and education & science, with room to cover arts, sports & tourism as well as the communication, energy and natural resources budgets for 2009 too,

* if issued as four-year debt (assuming a speedy resolution of the banking crisis) the annual cost would be €925mn, for 4 years, or more realistically, if issued at 10yrs, the annual interest bill based on prevailing interest rates would be €1.475bn, slightly more than the Employment, Trade & Enterprise budget

It is hard to imagine which Irish entitities could absorb all the additional State borrowing, implying that foreign ownership of Irish government (or quasi-goernment) debt will increase. While there was a €29.3bn trade surplus in 2009, net factor income from abroad was -€31.9bn. Increased foreign indebtedness will tend to increase the net capital outflow via debt interest payments, pushing a (virtually non-taxed) export-led recovery even further back on the horizon.

Clearly, the project represents a huge transfer of weatlh from the poor to the rich. In the modern era, this usually takes place in some under-developed economy by a Western power and is little reported. It is rarely done so blatantly within a Western economy; so one for the record books.

So what should progressives argue for as an alternative? The key to the situation, and the reason Mr Lenihan's assertion about 'obliteration' is a falsehood, is the bank guarantee. Without it there would be no possible contagion from the banks to government debt. And wthout it there would be no bank shareholders, either.

Their holding would be valued at their true worth, that is zero. It is probably also true that zero would be the share price without the latest lifeline from taxpayers, since any residual value in the shares was premised on the expectation for further slugs of taxpayer money as required.

Therefore, the shareholders would be wiped out and most of the bondholders too by either a withdrawal of the guarantee, or even charging a realistic price for it, or the repatration of the capital injections. Since the taxpayer is now the largest shareholder, emergency legislaion should be prepared to do both those things and at the same time, protect the deposits of the banks' customers by seizing them.

The new entitities would be owned by the State, as now yet rigorously managed, but could then form the basis of a banking sector which did not jeopardise depositors, engaged in prudent balance sheet management, not casino capitalism, and was directed to invest in the most productive areas of the economy, delivering large returns for the shareholder; the taxpayer, and large economic benefits for all.

Wednesday, 31 March 2010

Banks: elsewhere on the web ....

Over at Ireland after Nama, Declan Curran asks some pertinent questions. On Irish Economy, Karl Whelan takes a look at The Good, the Bad and the Ugly. Meanwhile, Ronan Lyons points out that the first tranche of loans may not be representative, and that subsequent tranches may show significantly larger discounts.

The 'I'm really getting tired of this nonsense' guide to bond yield trends

Michael Taft: There are others who will discuss intelligently the fall-out from Ireland’s financial Black Hole Day (Sli Eile, Stephen Kinsella and Nat O’Connor on this blog for instance). One thing that struck me during the Finance Minister’s robust, if economically-challenged, interview on Prime Time was his contention that things were, like, totally cool. Why? Since he announced the massive give-away, bond yields hadn’t moved. Wow. He made his announcement at 4:30 pm and by 10:00 pm bond yields hadn’t moved. This proved that not only that the international markets were not ‘concerned’ with our financial black hole, they were positively chill (or they just go to bed early).

One could really get tired of this. There’s an eerie anthropomorphic quality to discussions on bond markets. Apparently, these markets can ‘feel’, ‘be happy’, ‘become angry’, ‘contemplate’, etc. and on and on. The trend of commentary usually goes like this: ‘the markets will be concerned if the Government doesn’t get tough on trade unionists, the poor, public spending and businesses in debt’. And when the Government does do tough guy stuff, the bond markets ‘approve’ and so, are at peace.

All this comes from the sound-bite school of deep, thoughtful analysis. Tracking bond yields can tell us many things – and it’s amazing that what it usually tells us is what we want it to tell us: vide the Finance Minister last night. So in that spirit I have constructed my own way of explaining bond yield trends. I have used the gross redemption yields for 10-year plus bonds on the last day of the month, sourced from ISEQ (one of many ways to track borrowing costs). This is what the ‘markets’ are telling me.

APRIL 2008: We are still innocent. The ESRI has yet to discover the recession and predict 3.1 percent growth for 2009. There is talk of property prices but we are assured it will be a soft, gentle landing. AIB is trading at €13.25. In another country baseball season is starting and little boys will be playing well into the bright summer evenings.

Bond Yield: 4.40

SEPTEMBER 2008: The boys of summer are still playing baseball but the financial dogs in the street are muttering something about Irish banks and insolvencies. The Sunday Independent declares that if anything goes wrong, whatever that might be, it will of course be the fault of trade unions. Bank Guarantee announced at the end of the month. Markets don’t have time to react before month’s end because they go to bed early.

Bond Yield: 4.60

OCTOBER 2008: Bankers say everything is fine and they don’t need equity; the markets get worried. AIB trades at €5.00 but no one is fired. Bringing forward the Budget doesn’t help either – especially this budget.

Bond Yield: 4.84

DECEMBER 2009: Markets get less jittery. All that hysterics about the state being exposed to hundred of billions of bank Euros fade away. ISME calls for the suppression of trade unions. Their competitors, the Small Firms Association, call ISME weak on the issue of trade unions.

Bond Yield: 4.47

JANUARY 2009: Everything goes haywire. Markets up in arms. Is it because Anglo-Irish is nationalised or because the Government, only a few days before, was going to pump billions in it because they believed it was still viable? The markets unsure whether the Government was colluding in a tissue of lies and deceit or are just plain idiots. Live Register experiences biggest jump in two decades.

Bond Yield: 5.54

FEBRUARY 2009: The Government goes macho. They kick the unions out of Government buildings in the early morning (and don’t even call them a cab). The Finance Minister announces a pension levy on public sector workers and cuts in the number of special need teachers. Pumped abs and testosterone everywhere. Commentators note that even the weather has improved. The markets, however . . .

Bond Yield: 5.57

MARCH 2009: The Tánaiste declares the Government has public finances under control. No one, not even the omnipotent markets, knows what to make of this.

Bond Yield: 5.45

APRIL 2009: Just to prove the Tánaiste was right, the Government introduces an emergency budget. The markets don’t understand – consumer spending is collapsing, businesses reliant on domestic sales are collapsing; and the Government takes even more money out of people’s pockets. There’s counter-intuitive and there’s counter-intuitive; and then there’s Fianna Fail.

Bond Yield: 5.28

JUNE 2009: The markets reconsider the Government’s emergency budget and their deflationary strategy of cutting €11 billion out of an already debilitated economy over the next four years.

Bond Yield: 5.84

AUGUST 2009: For months the three major credit rating agencies have been downgrading Irish Government debt and are threatening more. Commentators are horrified and claim we’ll never be able to borrow again ever, the Sunday Independent blames trades unions, employers demand the minimum wage be cut (though no one can figure out how this will get cheaper money). The markets, however, prove they have a sense of humour.

Bond Yield: 4.68

THE AUTUMN RUN-UP TO THE BUDGET - NOVEMBER 2009: Everyone is giddy. If the Government keeps their promise to implement a puppy-crunching, Bruce Lee, in-your-face, take-no-prisoners budget, the markets will smile and investors will actually pay us to borrow from them. The Taoiseach promises blood, sweat and bankruptcies, the Tánaiste claims that what ever makes us redundant only makes us stronger; the Minister for Health (sic) goes one better and threatens IMF tanks in every town square in the country if we don’t take the pain.

Bond Yield: 5.16

DECEMBER 2010: The Government introduces a puppy-crunching, Bruce Lee, in-your-face, take-no-prisoners budget.

Bond Yield: 5.18

[For a few weeks everyone’s attention is on Greece and those irrational Greek workers striking and marching in the streets because they don’t want to be the fall-guys and fall-gals for maintaining a strong Euro, Germany’s current account surplus and finance capital’s hopes for a return to Alpha status.]

MARCH 30th 4:30 – 10: 00 pm: The Minister declares markets are totally cool with him shovelling up to €20 billion in Anglo-Irish (proves what shrewd market players the Cabinet are), that the economy has turned the corner, unemployment is stabilising and we’ll return to growth this year. Recession? What recession? The only recession is in your mind, dude.

Bond Yield: Moved not one cent according to the Minister.

* * *

All that – all that courageous action the Government has taken that has so impressed the markets – and bond yields are worse than when we started on this dismal path. Of course, there will be those who will claim that if the Government didn’t take courageous action, borrowing costs would have been worse. If so, then why is it high bond yields got worse every time they did?

That’s one way of looking at all this. For another perspective have a read of Michael Burke’s take on borrowing costs and the Government’s deflationary policies. You might have your own perspective. If so, go on to the Irish Stock Exchange website and build your own story.

But, please, just don’t make the markets ‘nervous’.

One could really get tired of this. There’s an eerie anthropomorphic quality to discussions on bond markets. Apparently, these markets can ‘feel’, ‘be happy’, ‘become angry’, ‘contemplate’, etc. and on and on. The trend of commentary usually goes like this: ‘the markets will be concerned if the Government doesn’t get tough on trade unionists, the poor, public spending and businesses in debt’. And when the Government does do tough guy stuff, the bond markets ‘approve’ and so, are at peace.

All this comes from the sound-bite school of deep, thoughtful analysis. Tracking bond yields can tell us many things – and it’s amazing that what it usually tells us is what we want it to tell us: vide the Finance Minister last night. So in that spirit I have constructed my own way of explaining bond yield trends. I have used the gross redemption yields for 10-year plus bonds on the last day of the month, sourced from ISEQ (one of many ways to track borrowing costs). This is what the ‘markets’ are telling me.

APRIL 2008: We are still innocent. The ESRI has yet to discover the recession and predict 3.1 percent growth for 2009. There is talk of property prices but we are assured it will be a soft, gentle landing. AIB is trading at €13.25. In another country baseball season is starting and little boys will be playing well into the bright summer evenings.

Bond Yield: 4.40

SEPTEMBER 2008: The boys of summer are still playing baseball but the financial dogs in the street are muttering something about Irish banks and insolvencies. The Sunday Independent declares that if anything goes wrong, whatever that might be, it will of course be the fault of trade unions. Bank Guarantee announced at the end of the month. Markets don’t have time to react before month’s end because they go to bed early.

Bond Yield: 4.60

OCTOBER 2008: Bankers say everything is fine and they don’t need equity; the markets get worried. AIB trades at €5.00 but no one is fired. Bringing forward the Budget doesn’t help either – especially this budget.

Bond Yield: 4.84

DECEMBER 2009: Markets get less jittery. All that hysterics about the state being exposed to hundred of billions of bank Euros fade away. ISME calls for the suppression of trade unions. Their competitors, the Small Firms Association, call ISME weak on the issue of trade unions.

Bond Yield: 4.47

JANUARY 2009: Everything goes haywire. Markets up in arms. Is it because Anglo-Irish is nationalised or because the Government, only a few days before, was going to pump billions in it because they believed it was still viable? The markets unsure whether the Government was colluding in a tissue of lies and deceit or are just plain idiots. Live Register experiences biggest jump in two decades.

Bond Yield: 5.54

FEBRUARY 2009: The Government goes macho. They kick the unions out of Government buildings in the early morning (and don’t even call them a cab). The Finance Minister announces a pension levy on public sector workers and cuts in the number of special need teachers. Pumped abs and testosterone everywhere. Commentators note that even the weather has improved. The markets, however . . .

Bond Yield: 5.57

MARCH 2009: The Tánaiste declares the Government has public finances under control. No one, not even the omnipotent markets, knows what to make of this.

Bond Yield: 5.45

APRIL 2009: Just to prove the Tánaiste was right, the Government introduces an emergency budget. The markets don’t understand – consumer spending is collapsing, businesses reliant on domestic sales are collapsing; and the Government takes even more money out of people’s pockets. There’s counter-intuitive and there’s counter-intuitive; and then there’s Fianna Fail.

Bond Yield: 5.28

JUNE 2009: The markets reconsider the Government’s emergency budget and their deflationary strategy of cutting €11 billion out of an already debilitated economy over the next four years.

Bond Yield: 5.84

AUGUST 2009: For months the three major credit rating agencies have been downgrading Irish Government debt and are threatening more. Commentators are horrified and claim we’ll never be able to borrow again ever, the Sunday Independent blames trades unions, employers demand the minimum wage be cut (though no one can figure out how this will get cheaper money). The markets, however, prove they have a sense of humour.

Bond Yield: 4.68

THE AUTUMN RUN-UP TO THE BUDGET - NOVEMBER 2009: Everyone is giddy. If the Government keeps their promise to implement a puppy-crunching, Bruce Lee, in-your-face, take-no-prisoners budget, the markets will smile and investors will actually pay us to borrow from them. The Taoiseach promises blood, sweat and bankruptcies, the Tánaiste claims that what ever makes us redundant only makes us stronger; the Minister for Health (sic) goes one better and threatens IMF tanks in every town square in the country if we don’t take the pain.

Bond Yield: 5.16

DECEMBER 2010: The Government introduces a puppy-crunching, Bruce Lee, in-your-face, take-no-prisoners budget.

Bond Yield: 5.18

[For a few weeks everyone’s attention is on Greece and those irrational Greek workers striking and marching in the streets because they don’t want to be the fall-guys and fall-gals for maintaining a strong Euro, Germany’s current account surplus and finance capital’s hopes for a return to Alpha status.]

MARCH 30th 4:30 – 10: 00 pm: The Minister declares markets are totally cool with him shovelling up to €20 billion in Anglo-Irish (proves what shrewd market players the Cabinet are), that the economy has turned the corner, unemployment is stabilising and we’ll return to growth this year. Recession? What recession? The only recession is in your mind, dude.

Bond Yield: Moved not one cent according to the Minister.

* * *

All that – all that courageous action the Government has taken that has so impressed the markets – and bond yields are worse than when we started on this dismal path. Of course, there will be those who will claim that if the Government didn’t take courageous action, borrowing costs would have been worse. If so, then why is it high bond yields got worse every time they did?

That’s one way of looking at all this. For another perspective have a read of Michael Burke’s take on borrowing costs and the Government’s deflationary policies. You might have your own perspective. If so, go on to the Irish Stock Exchange website and build your own story.

But, please, just don’t make the markets ‘nervous’.

How much are the bank bailouts going to cost us?

Nat O'Connor: There is a lack of clarity about just how much the bank bailout will cost ordinary people. But based on recent news, the estimated costs are huge.

The Irish Independent states that "Every man, woman and child in the State will have to pay an average of €2,000 every year just to service interest payments on borrowings to pay for the bank bailout, estimated to cost €40bn."

In fairness, it's not clear that we have enough information to know that yet. If the banks raise their own capital we won't need to borrow as much. Also, if we part-recapitalise the banks out of the National Pension Reserve Fund (which is what we did before) we will borrow less again. But let's tease out the scale of what borrowing €40 billion would mean.

Unfortunately, not every man, woman and child in Ireland has an income. So will paying the bill fall on the shoulders of Ireland's 1.6 million households, rather than its 4.5 million people? The costs then comes out at roughly €5,600 per year per household. But with state pensioners and other people living on social welfare on incomes of around €12,000, are we talking about halving their incomes and plunging hundreds of thousands of people into destitution?

Alternatively, we could look at the 1.9 million people in employment, who would have to take on an average of €4,600 each (with couples, where both partners are employed, taking on €9,200).

Average earnings for someone in employment in Ireland in 2009 were around €36,300 per year (CSO). So, for example, a single person on this income, already on c. €29,500 after tax, will see their final income fall to around €24,900. (Of course those on lower incomes might pay less, and those on higher incomes might pay more... this is just the average cost applied to the average income).

The cost to those in employment is likely to be lessened by further cuts in public expenditure (social welfare cuts, cuts to pensions, cuts to public capital expenditure, cuts to public services of all kinds, etc). Except that these cuts will also reduce quality of life, health, education, and increase households' costs to fill the gap created by the absence of public services.

And this is just to pay the interest on the loans to bail out the banks.

All the above assumes that NAMA will work and we will only have to pay the interest on the loans for a period of years. If NAMA makes a loss, or further bank bailouts are required, the burden of paying for all this will increase.

If that wasn't bad enough, some people will be further affected by mortgage interest increases. The Belfast Telegraph suggests that AIB "will respond to its latest bailout by raising mortgage rates by a further 1.5% this year." That's on top of this week's 0.5 per cent increase. Assuming the other banks follow suit, that will increase pressure on tens of thousands of households.

Not every household is affected by this double squeeze, but it is hard to see how households will be able to afford to pay another couple of thousand extra per year on their mortgage repayments, alongside bearing the tax increases to pay the interest on the loans to bail out the banks.

It is possible that we could see a major wave of mortgage default and repossession, which would trigger a further crisis in the banks, and a need for further recapitalisation. Those who don't default are likely to be paying way more than they can comfortably afford to keep their homes; all to avoid the nightmare of selling their homes at a low price, while still owing the bank the balance of their original (massive) mortgage loans.

In a year or so, the State could own all or most of the banks, but the citizens who own the State will be paying increased charges to the banks as customers at the same time as paying taxes for the loans to own them. The burden of paying the interest on the loans will all but rule out any productive investment in better infrastructure, better education, etc. Most of our potential for investment will be tied up for years in paying for the mistakes made by past governments.

There is a need for much more accurate information to be made available on exactly how the Government plans on paying for the banks and at what point it would be cheaper to let some of them go bust. We need to know exactly how much households will have to pay and what will be the opportunity cost in cuts to public services and the loss of a generation's ability to invest in a better future. At present we can only speculate. But based on the figures currently in the news, it's a perverse and gloomy situation and we haven't gotten to the bottom of it yet.

The Irish Independent states that "Every man, woman and child in the State will have to pay an average of €2,000 every year just to service interest payments on borrowings to pay for the bank bailout, estimated to cost €40bn."

In fairness, it's not clear that we have enough information to know that yet. If the banks raise their own capital we won't need to borrow as much. Also, if we part-recapitalise the banks out of the National Pension Reserve Fund (which is what we did before) we will borrow less again. But let's tease out the scale of what borrowing €40 billion would mean.

Unfortunately, not every man, woman and child in Ireland has an income. So will paying the bill fall on the shoulders of Ireland's 1.6 million households, rather than its 4.5 million people? The costs then comes out at roughly €5,600 per year per household. But with state pensioners and other people living on social welfare on incomes of around €12,000, are we talking about halving their incomes and plunging hundreds of thousands of people into destitution?

Alternatively, we could look at the 1.9 million people in employment, who would have to take on an average of €4,600 each (with couples, where both partners are employed, taking on €9,200).

Average earnings for someone in employment in Ireland in 2009 were around €36,300 per year (CSO). So, for example, a single person on this income, already on c. €29,500 after tax, will see their final income fall to around €24,900. (Of course those on lower incomes might pay less, and those on higher incomes might pay more... this is just the average cost applied to the average income).

The cost to those in employment is likely to be lessened by further cuts in public expenditure (social welfare cuts, cuts to pensions, cuts to public capital expenditure, cuts to public services of all kinds, etc). Except that these cuts will also reduce quality of life, health, education, and increase households' costs to fill the gap created by the absence of public services.

And this is just to pay the interest on the loans to bail out the banks.

All the above assumes that NAMA will work and we will only have to pay the interest on the loans for a period of years. If NAMA makes a loss, or further bank bailouts are required, the burden of paying for all this will increase.

If that wasn't bad enough, some people will be further affected by mortgage interest increases. The Belfast Telegraph suggests that AIB "will respond to its latest bailout by raising mortgage rates by a further 1.5% this year." That's on top of this week's 0.5 per cent increase. Assuming the other banks follow suit, that will increase pressure on tens of thousands of households.

Not every household is affected by this double squeeze, but it is hard to see how households will be able to afford to pay another couple of thousand extra per year on their mortgage repayments, alongside bearing the tax increases to pay the interest on the loans to bail out the banks.

It is possible that we could see a major wave of mortgage default and repossession, which would trigger a further crisis in the banks, and a need for further recapitalisation. Those who don't default are likely to be paying way more than they can comfortably afford to keep their homes; all to avoid the nightmare of selling their homes at a low price, while still owing the bank the balance of their original (massive) mortgage loans.

In a year or so, the State could own all or most of the banks, but the citizens who own the State will be paying increased charges to the banks as customers at the same time as paying taxes for the loans to own them. The burden of paying the interest on the loans will all but rule out any productive investment in better infrastructure, better education, etc. Most of our potential for investment will be tied up for years in paying for the mistakes made by past governments.

There is a need for much more accurate information to be made available on exactly how the Government plans on paying for the banks and at what point it would be cheaper to let some of them go bust. We need to know exactly how much households will have to pay and what will be the opportunity cost in cuts to public services and the loss of a generation's ability to invest in a better future. At present we can only speculate. But based on the figures currently in the news, it's a perverse and gloomy situation and we haven't gotten to the bottom of it yet.

Tuesday, 30 March 2010

Groundhog Day

Stephen Kinsella: Super Tuesday has been and gone. Even those of us who study Irish public policy and the Irish economy on a daily basis were taken aback by the scale of the wealth transfers from state to private banks. What does it all mean? I’m a professional economist folks–don’t try this at home.

As I mentioned on Drivetime this evening, the injection of capital, combined with the government guarantee and NAMA, is supposed to heal banks’ balance sheets enough to get them into a position where they can borrow cheaply from abroad, and so resume lending again.

Finally, notice the precise imprecision: promissory notes are being issued for several billions, but spread out over ‘10 or 15 years’. Surely we can do better? Not to worry though, we’ll have another crack at it, when groundhog day rolls around again.

As I mentioned on Drivetime this evening, the injection of capital, combined with the government guarantee and NAMA, is supposed to heal banks’ balance sheets enough to get them into a position where they can borrow cheaply from abroad, and so resume lending again.

My opinion is that this increase in lending won’t happen, because canny investors know that residential loan defaults are on the way. We’ll have a groundhog day. This is not the one big moment to sort out our banking sector. This is a stage in a process, and nothing more. We’ll see the outright nationalisation of AIB by the end of 2010.

NAMA is getting going with its big 10 debtors, transferring 16 billion euros worth of loans in the next few weeks, representing perhaps 20% of the overall loans to be transferred by the end of the year. In particular, Anglo transfers €10bn at 50% discount, AIB transfers €3.29bn (43%), BoI transfers €1.93bn (35%), Nationwide transfers €670m (58%), and EBS transfers €140m (37%). Overall, the haircut is 47%. We need to be careful with that 47% discount number (or ‘haircut’) everyone is talking about. As usual, the bigger haircut, the greater the hole to fill in balance sheets to be filled by taxpayer’s money. While it might be the weighted average of the discounts being applied to each bank as the Minister says, we can’t back out the prices NAMA is going to pay for the loans in, say, AIB or Anglo. Update: Karl Whelan has more on this issue.

Notice also the rhetorical shift. We knew after guaranteeing the liabilities of the banks that a bad bank or asset management vehicle like NAMA was necessary, but also a further injection of capital and perhaps even full scale nationalisation. We were told NAMA was the only game in town, and all other options were not to be considered. Those who argued for nationalisation were derided or ignored. Now it looks highly likely that at least AIB, Anglo, INM, and EBS will be nationalised by the end of 2010, with the state taking a large piece of BoI as well.

Finally, notice the precise imprecision: promissory notes are being issued for several billions, but spread out over ‘10 or 15 years’. Surely we can do better? Not to worry though, we’ll have another crack at it, when groundhog day rolls around again.

Moral overload?

Slí Eile: No sooner was the ink dry on the Public Service Agreement (2010-2014) than the next news story broke on - NAMA. It just never dies down. We have now moved from dealing in billions to tens of billions. In Weimar Republic style numbers inflation we are moving into funny money territory. Except it is not funny for anyone. It is staggering. The figures dwarf any possible savings in public sector pay bill by a large multiple that the financial implications of the new deal on the public service (if is passed by union members) pale into insignificance. The negotiators deserve credit for their efforts. But, there is one snag - its paragraph 28 on page 9 - the very last sentence in the main document. It reads:

Worryingly, the Labour Party have pointed out (Strategic Investment Bank) that:

The implementation of this Agreement is subject to no currently unforeseen budgetary deterioration.O dear. I think we might have just had an unforeseen budgetary deterioration over the six o clock news this evening. Even Minister Lenihan admits that this has serious implications for taxpayers (contrary to the McCarthyite dictum that NAMA and the fiscal crisis have nothing to do with each other). NAMA has everything to do with the crisis because it is going to magnify the mountain of debt, contraction and cost-cutting imposed by a general slump. With GNP falling at an annual rate of over 12%, tax receipts under-shooting for most months there is every prospect of an early budget or an early election or an early bank collapse or all three. Either we keep on feeding the junkie called Anglo or we allow the junkie to die. Pretty stark. But, the problem right now for Government is whether it can deliver on all of its promises to:

- not cut public sector pay before 2014

- reduce the General Government Deficit to 3% of GDP by 2014

- keep the Anglo junkie fed with €10bn every few months (does anyone believe that another shot will not be demanded - we are in free fall)

- and keep the economy from contracting by another 10-12% this year (the forecast for a decline of 3% but that remains to be seen).

Worryingly, the Labour Party have pointed out (Strategic Investment Bank) that:

At the same time, Ireland’s fiscal position and the restrictions imposed by theWhere does that leave us if people are saying that we are under siege on all sides and to such an extent that we cannot invest our way out of this crisis along with other policy measures?

Stability and Growth Pact (SGP) represent a major constraint. There is little prospect that the level of investment necessary to improve our infrastructure can take place in the next decade given the current state of the public finances. And even without the fiscal crisis, the SGP, which includes public capital investment as part of its limit for the budget deficit, would restrict the State from making the necessary investments.

Monday, 29 March 2010

Guest Post by Gerry O'Hanlon S.J.: Asking the Right Question

Gerry O’Hanlon: We are understandably concerned about economic recovery in Ireland these days. But given that ‘recovery’ might be taken to imply a return to a previously desirable state, perhaps we need to reframe the question that we ask. If we ask ‘how do we recover’, we are in danger, in our public discourse, of letting conventional indicators like a pick-up in retail sales, an increase in property values, a rise in consumer sentiment, even – the Holy Grail! – growth in GDP and GNP, become the sole normative criteria for what might too easily become a return to ‘business as usual’. That would be a pity. Given what we have learned about the serious flaws in our ‘business as usual’ model, it might be better to ask a different sort of question that might push us in a more radical direction – so, for example, ‘how do we create a new economic model that is sustainable’?

The predominantly neo-liberal, infinite-growth model of the recent past has let us down. It was shot through with an economism which meant that an obsession with economic growth trumped so many other human values. It was riddled with inequalities both within and between nations, in ways which made solidarity unsustainable. And its focus on consumption did serious damage to our planet, as well as failing to make us happier.

In this context the reflections of the former Chief Rabbi of Ireland, David Rosen, are apt. Rosen quotes an old Jewish commentary on those who, according to chapter 11 of the Book of Genesis, showed hubris in attempting to build The Tower of Babel up to the heavens – ‘if in the course of building, a human being fell and was even killed, no one batted an eyelid: but if a brick fell and shattered, they all sat down and cried’. In other words, in this story of an ancient industrial collapse, work and growth were more important than human beings, and the enterprise went to the heads of its developers, showing ‘a profoundly distorted sense of values in which human life and dignity are subordinated to material achievements’.

Of course ‘material achievements’ are important: we want a future where people can work, where basic needs are satisfied, where human dignity is respected. But can that perhaps be done within a vision of the future articulated in terms of ‘prosperity without growth’ (Professor Tim Jackson), a ‘steady-state economy’ (Hermann Daly), ‘the richness of sufficiency’ (Bangkok letter of ecumenical group of Asian Churches in 1999)? And within that vision perhaps we need to create a culture which values society as well as the individual, a culture of the common good that respects solidarity and fairness and that commits itself to responsibility for inter-generational care of the earth?

That kind of new vision, those kinds of values, would have concrete implications. Banks would need to recognise that they have obligations to all stake-holders, not just to share-holders, that they have a social function in serving the ‘real economy’. Financial traders would need to be regulated in such a way that short-termism is eschewed – the introduction of a Tobin or Robin Hood tax on international currency and financial transactions might be a relatively simple and effective first step in this respect. Our economic priority should be to favour labour rather than capital, to put work and jobs as a prime target, and to consider salary caps or more progressive redistributive tax policies in order to bring about greater equality. It is estimated that CEOs in the USA were paid 344 times the average worker’s wage in 2007, as against 42 times in 1989. Why shouldn't we take up the suggestion of Paula Clancy of TASC and consider what it would be like if a policy objective was inserted in the Constitution that limited the top 20 per cent in Ireland to an income of 10 times, or even 5 times, that of the bottom 20 per cent?

The New Economics Foundation (The Great Transition, 2009) has tried to spell out concretely what such an economic model, with those kinds of values, might mean for Britain. They speak in terms of a fall of GDP by a third (to 2001 levels); of a four-day working week, to allow for full employment with less economic activity and to give a better work-life balance; market prices reflecting social and environmental costs; a redistribution of income to Danish levels of equality; capital markets functioning in such a way that company profitability would be linked to social and environmental value, so that share prices for listed companies would reflect this – and so on. All this would be premised on a democratic national determination of what the UK as a society deemed to be of social and environmental value, with government retaining the right to make determinations between competing interests. The net result, they estimate, would be a growth in ‘real value’, despite a reduction in consumption and economic growth.

Are we doing enough to raise these kinds of questions and research these kinds of solutions in Ireland? What is involved is a change of culture; a political class which is capable of the kind of leadership given at the height of the Northern Ireland crisis when a more radical approach was taken; a religious input that transcends the evil evidenced in Murphy and Ryan, not to mention the mediocrity of the kind of social conservatism so common in post-independence Ireland but which – as Habermas, Putnam, Rawls and Sandal all acknowledge – can draw on inspirational sources of self-transcendence which encourage believers to engage in a critique of the status quo and to join with fellow-citizens in the search for a better way forward.

Gerry O’Hanlon, S.J., Jesuit Centre for Faith and Justice, author of recently published Theology in the Irish Public Square, Dublin: Columba Press, 2010.

The predominantly neo-liberal, infinite-growth model of the recent past has let us down. It was shot through with an economism which meant that an obsession with economic growth trumped so many other human values. It was riddled with inequalities both within and between nations, in ways which made solidarity unsustainable. And its focus on consumption did serious damage to our planet, as well as failing to make us happier.

In this context the reflections of the former Chief Rabbi of Ireland, David Rosen, are apt. Rosen quotes an old Jewish commentary on those who, according to chapter 11 of the Book of Genesis, showed hubris in attempting to build The Tower of Babel up to the heavens – ‘if in the course of building, a human being fell and was even killed, no one batted an eyelid: but if a brick fell and shattered, they all sat down and cried’. In other words, in this story of an ancient industrial collapse, work and growth were more important than human beings, and the enterprise went to the heads of its developers, showing ‘a profoundly distorted sense of values in which human life and dignity are subordinated to material achievements’.

Of course ‘material achievements’ are important: we want a future where people can work, where basic needs are satisfied, where human dignity is respected. But can that perhaps be done within a vision of the future articulated in terms of ‘prosperity without growth’ (Professor Tim Jackson), a ‘steady-state economy’ (Hermann Daly), ‘the richness of sufficiency’ (Bangkok letter of ecumenical group of Asian Churches in 1999)? And within that vision perhaps we need to create a culture which values society as well as the individual, a culture of the common good that respects solidarity and fairness and that commits itself to responsibility for inter-generational care of the earth?

That kind of new vision, those kinds of values, would have concrete implications. Banks would need to recognise that they have obligations to all stake-holders, not just to share-holders, that they have a social function in serving the ‘real economy’. Financial traders would need to be regulated in such a way that short-termism is eschewed – the introduction of a Tobin or Robin Hood tax on international currency and financial transactions might be a relatively simple and effective first step in this respect. Our economic priority should be to favour labour rather than capital, to put work and jobs as a prime target, and to consider salary caps or more progressive redistributive tax policies in order to bring about greater equality. It is estimated that CEOs in the USA were paid 344 times the average worker’s wage in 2007, as against 42 times in 1989. Why shouldn't we take up the suggestion of Paula Clancy of TASC and consider what it would be like if a policy objective was inserted in the Constitution that limited the top 20 per cent in Ireland to an income of 10 times, or even 5 times, that of the bottom 20 per cent?

The New Economics Foundation (The Great Transition, 2009) has tried to spell out concretely what such an economic model, with those kinds of values, might mean for Britain. They speak in terms of a fall of GDP by a third (to 2001 levels); of a four-day working week, to allow for full employment with less economic activity and to give a better work-life balance; market prices reflecting social and environmental costs; a redistribution of income to Danish levels of equality; capital markets functioning in such a way that company profitability would be linked to social and environmental value, so that share prices for listed companies would reflect this – and so on. All this would be premised on a democratic national determination of what the UK as a society deemed to be of social and environmental value, with government retaining the right to make determinations between competing interests. The net result, they estimate, would be a growth in ‘real value’, despite a reduction in consumption and economic growth.

Are we doing enough to raise these kinds of questions and research these kinds of solutions in Ireland? What is involved is a change of culture; a political class which is capable of the kind of leadership given at the height of the Northern Ireland crisis when a more radical approach was taken; a religious input that transcends the evil evidenced in Murphy and Ryan, not to mention the mediocrity of the kind of social conservatism so common in post-independence Ireland but which – as Habermas, Putnam, Rawls and Sandal all acknowledge – can draw on inspirational sources of self-transcendence which encourage believers to engage in a critique of the status quo and to join with fellow-citizens in the search for a better way forward.

Gerry O’Hanlon, S.J., Jesuit Centre for Faith and Justice, author of recently published Theology in the Irish Public Square, Dublin: Columba Press, 2010.

Lies, Damn Lies & Irish Economic Statistics - A Basic Lesson in Corporate Tax Planning

An Saoi: I have had enough of all of those stockbroker economists & politicians who lecture us incessantly that exports are the key to getting us out of their economic mess. I decided to put together this note on “Irish” exports, or more correctly Ireland’s role in worldwide tax planning. You will doubtless have heard that “Irish” exports have fallen very little through this depression. This post tries to explain why.

Please make the effort to read it all; I have tried my best to keep it as simple as possible.

The diagrams below show a basic simple structure used by many multi-nationals to avoid paying tax. Sales are booked through an Irish trading company for perhaps the whole of Europe, and the profits are quickly hoovered into another “Irish” company, but this one is actually in a tax haven. It is sometimes referred to as a “double Irish”.

Let us say a US multi-national wants to set up an Irish trading subsidiary or as they are normally described by the IDA a “European Headquarters”. Instead of setting up one company however it sets up two, a trading sub, which will carry out the activity and a holding company, which will move its centre of management and control to a tax haven, let us say the Bahamas, directly after formation. This company is Irish Registered and Non-Resident or an IRNR.

The IRNR will own the license or intellectual property required by the trading company and issues a sub-license to a Dutch BV.

The Dutch BV passes on a sub-license to the Irish trading company. This avoids the IRNR being deemed to be resident in Ireland and thus taxable in this State. It is the reason you interpose a Dutch BV, which acts as a conduit to get the profits tax free up to the IRNR.

The Irish trading company “sells” the license, goods or whatever the company makes or does throughout Europe, paying local subsidiaries a small commission to do the marketing. It passes most of the profit upwards in the form of a royalty payment. Instead of paying a tax rate of 12.5%, it actually has a tax rate of about 3% or even less.

The US accepts that companies are resident in the country where the company is resident, but Ireland looks at its so-called “centre of management and control”. The haven company therefore is Irish as far as the Yanks are concerned, but is not consider Irish by the Revenue Commissioners.

Fig. 1

Fig. 2

Kathleen Barrington of the Sunday Business Post described here how NCR washed most of its profits through Ireland and Simon Bowers writing in the Guardian showed how Google books all its sales through Google Ireland Ltd here.

Tax avoidance is a serious issue, which as an Oxfam publication issued in March 2009 showed costs lives. Ireland is a prime player in world tax avoidance because we happily co-operate with many of the largest multi-nationals, by not just allowing these types of structures, but actually marketing the country as the place to locate.

The accounts of the Irish trading entity would look something like this. This is not an extreme example, but should give a flavour of the type of “exports” we really produce.

(*I have assumed that Depreciation = Capital Allowances)

Please make the effort to read it all; I have tried my best to keep it as simple as possible.

The diagrams below show a basic simple structure used by many multi-nationals to avoid paying tax. Sales are booked through an Irish trading company for perhaps the whole of Europe, and the profits are quickly hoovered into another “Irish” company, but this one is actually in a tax haven. It is sometimes referred to as a “double Irish”.

Let us say a US multi-national wants to set up an Irish trading subsidiary or as they are normally described by the IDA a “European Headquarters”. Instead of setting up one company however it sets up two, a trading sub, which will carry out the activity and a holding company, which will move its centre of management and control to a tax haven, let us say the Bahamas, directly after formation. This company is Irish Registered and Non-Resident or an IRNR.

The IRNR will own the license or intellectual property required by the trading company and issues a sub-license to a Dutch BV.

The Dutch BV passes on a sub-license to the Irish trading company. This avoids the IRNR being deemed to be resident in Ireland and thus taxable in this State. It is the reason you interpose a Dutch BV, which acts as a conduit to get the profits tax free up to the IRNR.

The Irish trading company “sells” the license, goods or whatever the company makes or does throughout Europe, paying local subsidiaries a small commission to do the marketing. It passes most of the profit upwards in the form of a royalty payment. Instead of paying a tax rate of 12.5%, it actually has a tax rate of about 3% or even less.

The US accepts that companies are resident in the country where the company is resident, but Ireland looks at its so-called “centre of management and control”. The haven company therefore is Irish as far as the Yanks are concerned, but is not consider Irish by the Revenue Commissioners.

Fig. 1

Fig. 2

Kathleen Barrington of the Sunday Business Post described here how NCR washed most of its profits through Ireland and Simon Bowers writing in the Guardian showed how Google books all its sales through Google Ireland Ltd here.

Tax avoidance is a serious issue, which as an Oxfam publication issued in March 2009 showed costs lives. Ireland is a prime player in world tax avoidance because we happily co-operate with many of the largest multi-nationals, by not just allowing these types of structures, but actually marketing the country as the place to locate.

The accounts of the Irish trading entity would look something like this. This is not an extreme example, but should give a flavour of the type of “exports” we really produce.

(*I have assumed that Depreciation = Capital Allowances)

Friday, 26 March 2010

DDDA Reports

Wednesday, 24 March 2010

The day after the IMF's tomorrow

Michael Taft: The IMF has suggested that the Irish Government’s growth projections are too optimistic and should be scaled back. So has the EU Commission. This has grave implications for the Government’s current strategy; if growth doesn’t come right, fiscal targets will be missed, debt will pile up, unemployment will remain high and living standards low. The Government may well end up sinking further into deflationary quicksand.

The IMF has projected growth for Ireland up to 2014. While these projections were initially produced in the middle of last year, the IMF reconfirmed them in their recent World Economic Outlook. What would be that impact on the deficit given these growth projections? The following examines only the tax revenue side of the equation.

First, we find IMF growth projections much lower than the Government’s. Between 2010 and 2014, the Government expects the economy to grow by 17.4 percent in real terms; the IMF, 8.8 percent. This will have considerable implications for public finances, as tax revenue is a function of GDP – low economic growth equals low tax revenue growth.

If the Government’s ‘tax burden’ or ‘tax ratio’ holds, under the IMF scenario we would find that not only will we fail to meet the Maastricht guidelines by 2014, we will pile up considerably higher debt in the process. Under the IMF scenario, the annual deficit is unsurprisingly higher each year; by 2014 it still remains above Maastricht guideline levels by 2014.

More alarmingly, is the growth in overall debt levels. The Government expects gross debt to be at 80.8 percent of GDP. However, if the IMF projections hold, overall debt will soar to over 93 percent – a result of higher annual deficits, and lower nominal GDP. This is what the TASC letter referred to as the ‘low-growth, high debt’ future.

There are two major caveats: first, this doesn’t include higher unemployment costs. We should expect unemployment, under the IMF’s lower growth scenario, to remain higher than the Government’s forecasts. If so, spending will rise above current projected levels. Second, higher borrowing levels will incur higher debt service costs. Factor these in, and the deficit and overall debt levels will be higher still.

This is all of a piece. In a previous post, Michael Burke and I showed how the Government’s current strategy will depress future growth. That is because the Government, rather than reducing the deficit, is embedding the deficit into the economic base.

So which scenario is more likely? The IMF projections are clearly pessimistic. The Government will take some comfort from recent projections. For 2011, Bloxham is projecting 3 percent growth; Friends First 3.1 percent. IBEC, however, is slightly more cautious, with a projection of 2.1 percent while PwC projects growth at 1.8 percent.

Some comfort, yes; but even the Department of Finance warns that GDP growth may not be tax-rich. This is because growth may be driven by exports from the multi-national sector.

So do all these numbers matter? Yes, very much so. NCB’s growth projections come up only slightly less than the Government by 2014, but even this has the potential to knock the Government’s fiscal targets off course. They, too, accept that the Government will miss its 2014 target, while piling up more debt than the Government expects.

In short, the Government’s fiscal strategy is built on quicksand. Its growth projections are optimistic and it has failed to factor in the deflationary effects of its current spending cuts policies. If they resort to further fiscal tightening to make up for this, all that will happen is that they will sink even further.

And the rest of us along with them.

The IMF has projected growth for Ireland up to 2014. While these projections were initially produced in the middle of last year, the IMF reconfirmed them in their recent World Economic Outlook. What would be that impact on the deficit given these growth projections? The following examines only the tax revenue side of the equation.

First, we find IMF growth projections much lower than the Government’s. Between 2010 and 2014, the Government expects the economy to grow by 17.4 percent in real terms; the IMF, 8.8 percent. This will have considerable implications for public finances, as tax revenue is a function of GDP – low economic growth equals low tax revenue growth.

If the Government’s ‘tax burden’ or ‘tax ratio’ holds, under the IMF scenario we would find that not only will we fail to meet the Maastricht guidelines by 2014, we will pile up considerably higher debt in the process. Under the IMF scenario, the annual deficit is unsurprisingly higher each year; by 2014 it still remains above Maastricht guideline levels by 2014.

More alarmingly, is the growth in overall debt levels. The Government expects gross debt to be at 80.8 percent of GDP. However, if the IMF projections hold, overall debt will soar to over 93 percent – a result of higher annual deficits, and lower nominal GDP. This is what the TASC letter referred to as the ‘low-growth, high debt’ future.

There are two major caveats: first, this doesn’t include higher unemployment costs. We should expect unemployment, under the IMF’s lower growth scenario, to remain higher than the Government’s forecasts. If so, spending will rise above current projected levels. Second, higher borrowing levels will incur higher debt service costs. Factor these in, and the deficit and overall debt levels will be higher still.

This is all of a piece. In a previous post, Michael Burke and I showed how the Government’s current strategy will depress future growth. That is because the Government, rather than reducing the deficit, is embedding the deficit into the economic base.

So which scenario is more likely? The IMF projections are clearly pessimistic. The Government will take some comfort from recent projections. For 2011, Bloxham is projecting 3 percent growth; Friends First 3.1 percent. IBEC, however, is slightly more cautious, with a projection of 2.1 percent while PwC projects growth at 1.8 percent.

Some comfort, yes; but even the Department of Finance warns that GDP growth may not be tax-rich. This is because growth may be driven by exports from the multi-national sector.

So do all these numbers matter? Yes, very much so. NCB’s growth projections come up only slightly less than the Government by 2014, but even this has the potential to knock the Government’s fiscal targets off course. They, too, accept that the Government will miss its 2014 target, while piling up more debt than the Government expects.

In short, the Government’s fiscal strategy is built on quicksand. Its growth projections are optimistic and it has failed to factor in the deflationary effects of its current spending cuts policies. If they resort to further fiscal tightening to make up for this, all that will happen is that they will sink even further.

And the rest of us along with them.

Tuesday, 23 March 2010

IMF et al on Fiscal Stimulus

Michael Burke: Philip Lane has posted a link to a very useful IMF working paper here. The paper draws on a wide variety of leading macroeconomic models (IMF, EU, Fed, Bank of Canada, etc.) to examine the effectiveness of fiscal stimulus.

Some interesting features of the paper’s conclusion: “There are four broad conclusions flowing from our analysis.

First, there is no such thing as a simple fiscal multiplier. The response of the economy to temporary discretionary fiscal stimulus depends on a number of factors, including most importantly the type of fiscal instrument used and the extent of monetary accommodation of the higher inflation generated by the stimulus.

Second, temporary expansionary fiscal actions can be highly effective, particularly when the fiscal instrument is spending or well-targeted transfers, and when in addition monetary policy is accommodative.

Third, permanent stimulus, that is a permanent increase in deficits, is much more problematic than temporary stimulus. It leads to a long-run contraction in output, but in addition the perception that deficits will become permanent also substantially reduces short-run fiscal multipliers.

Fourth, the G20 stimulus should have significant effects on global GDP in 2009 and 2010.”

So, it seems that the rest of the world has good reason to believe in the ‘tooth-fairy’ of fiscal stimulus. No such naïveté to be found in the ranks of Irish policymaking, unfortunately.

In discriminating as to types of stimulus, the verdict is also rather clear,

“A number of results are consistent across all models.

First, the multipliers from government investment and consumption expenditures, which are roughly similar in size, are clearly larger than the multipliers from transfers, labor income taxes, consumption taxes and corporate taxes.

Second, multipliers are small for general transfers, labor income taxes and corporate taxes, and somewhat larger (but still small relative to government expenditures) for consumption

taxes.

Third, only targeted transfers come close to having multipliers similar to those of government expenditures……[Yet....]

…it is of interest to note that in none of the regions [of the world adopting fiscal stimulus] do increases in government consumption play a predominant role.”

Figs. 22 and 31 show the very large multiplier effects of government investment and (slightly lower) effects of targeted transfers to the low paid in the US economy and Figs. 64 and 73 show the same for the EU.